Crocs ($CROX) 2025 Deep Dive

Crocs continued growth, Hey Dude turnaround and the beginnings of a share cannibal at a valuation of 6.5X FCF

Welcome to this deep dive into Crocs Inc ($CROX).

Crocs is famous for its recognisable classic clog design that has driven the success of the brand since its founding in 2002. Despite being called a fad every year in the company’s 23-year operating history, the company continues to sell more shoes every year, driven by its product-led innovation and social marketing strategy.

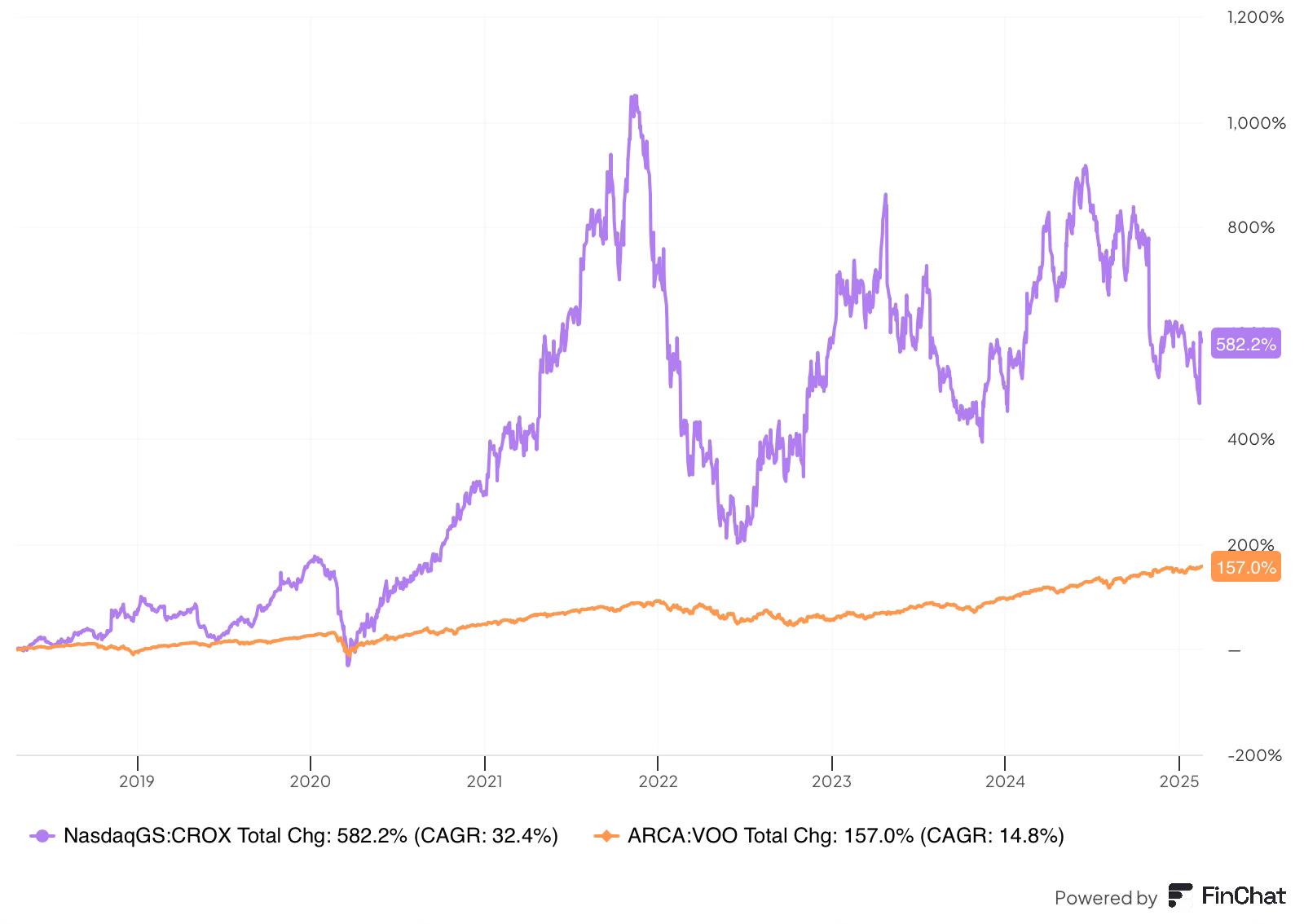

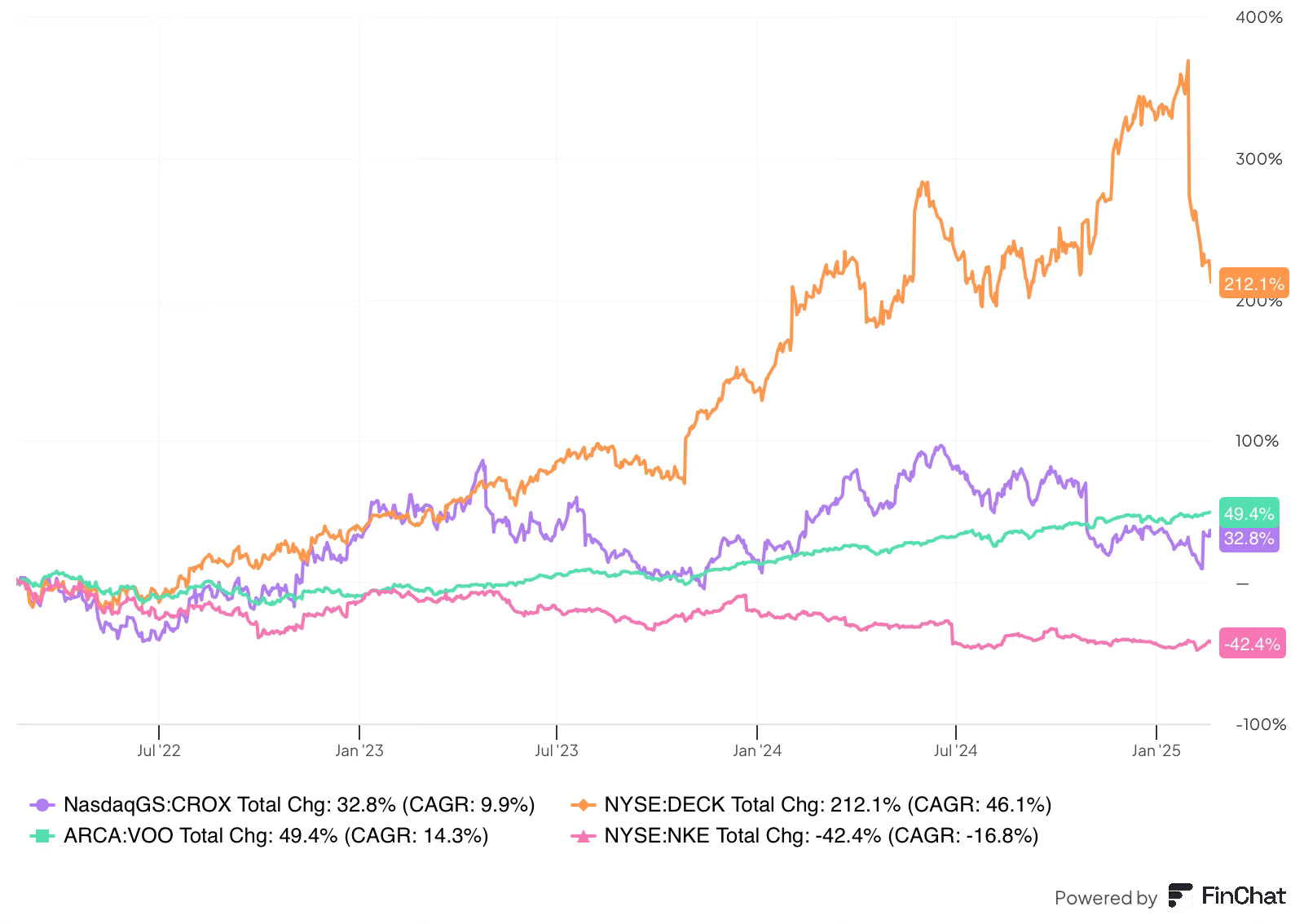

In this deep dive, I will cover the most important aspect of the business to help long-term investors get up to speed with the investment case for Crocs. The stock, which has outperformed the S&P 500 by a considerable margin, currently trades at 6.5X FCF, presenting a compelling opportunity for long-term investors.

In this deep dive, I will cover:

Business Overview

Business pressure

The investment case

Quality Characteristics

Management

Crocs

Sandals

International

Hey Dude

Brand Awareness

International

Buybacks

Valuation

Risks

Overview

Crocs Inc. is a global leader in the $160B casual footwear market, known for its controversial classic clog design and innovative marketing. The company owns two brands, Crocs and Hey Dude, after acquiring the latter in February 2022. Following the acquisition, Crocs remains 80% of revenue, while Hey Dude makes up the remaining 20%.

The company strives to be the world leader in innovative casual footwear, combining comfort and style at a value consumers want.

The company designs, develops, markets and distributes footwear. The only thing they don’t do is manufacture, which is done through third-party manufacturers using a proprietary moulded footwear technology. This technology uses proprietary materials such as Croslite.

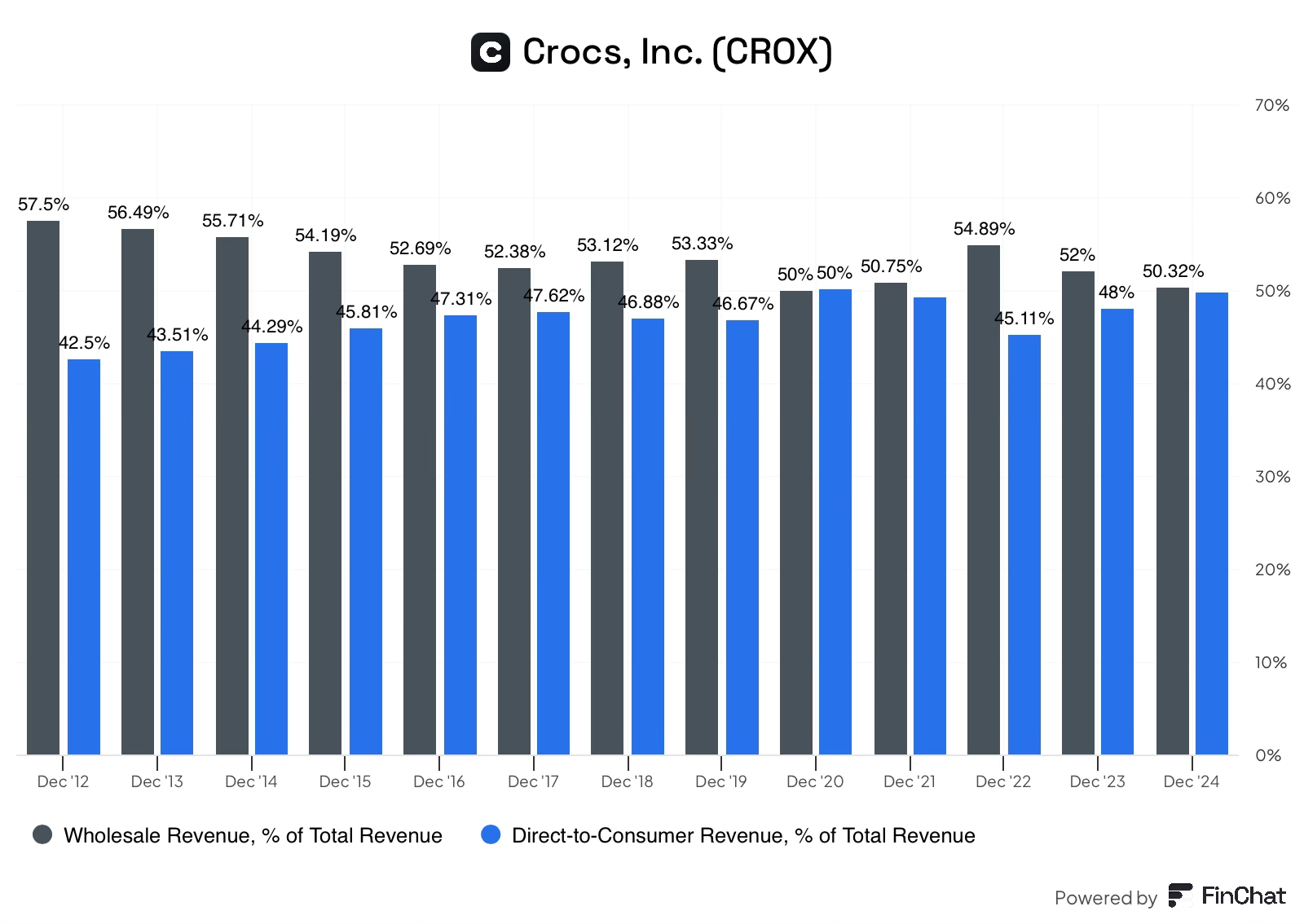

Distribution is split 50/50 between direct-to-consumer and wholesale, this has remained stable over the past few years.

Wholesale includes domestic and International multi-brand retailers, mono-branded partner stores, e-tailers and distributors.

Direct-to-consumer includes company-operated retail stores, the company e-commerce store, and third-party marketplaces (Amazon and TikTok shop)

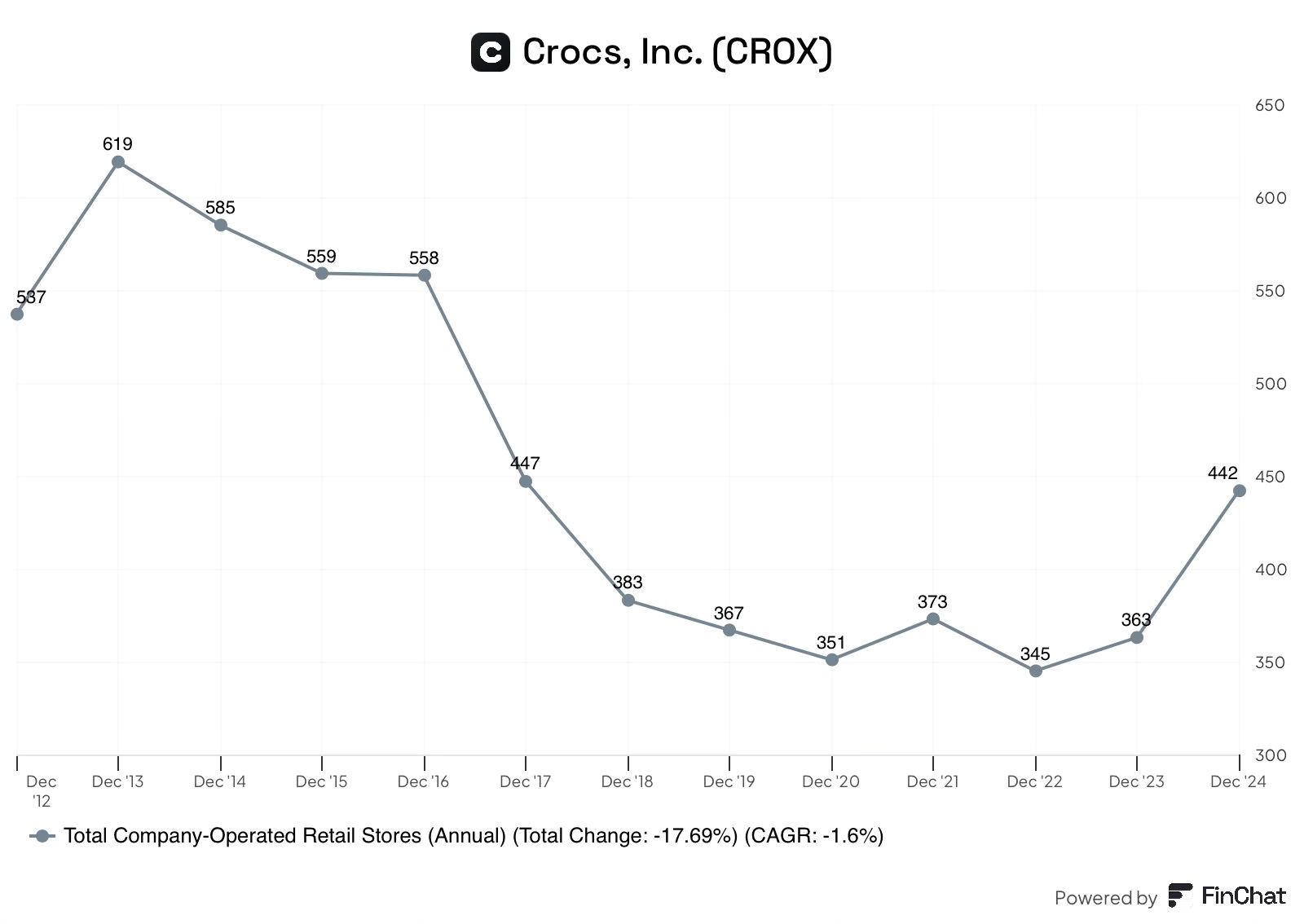

The company operates 442 outlet stores, predominantly in North America, over time management has been closing poor-performing Crocs outlets. The recent increase is attributable to the rollout of Hey Dude outlet stores across North America.

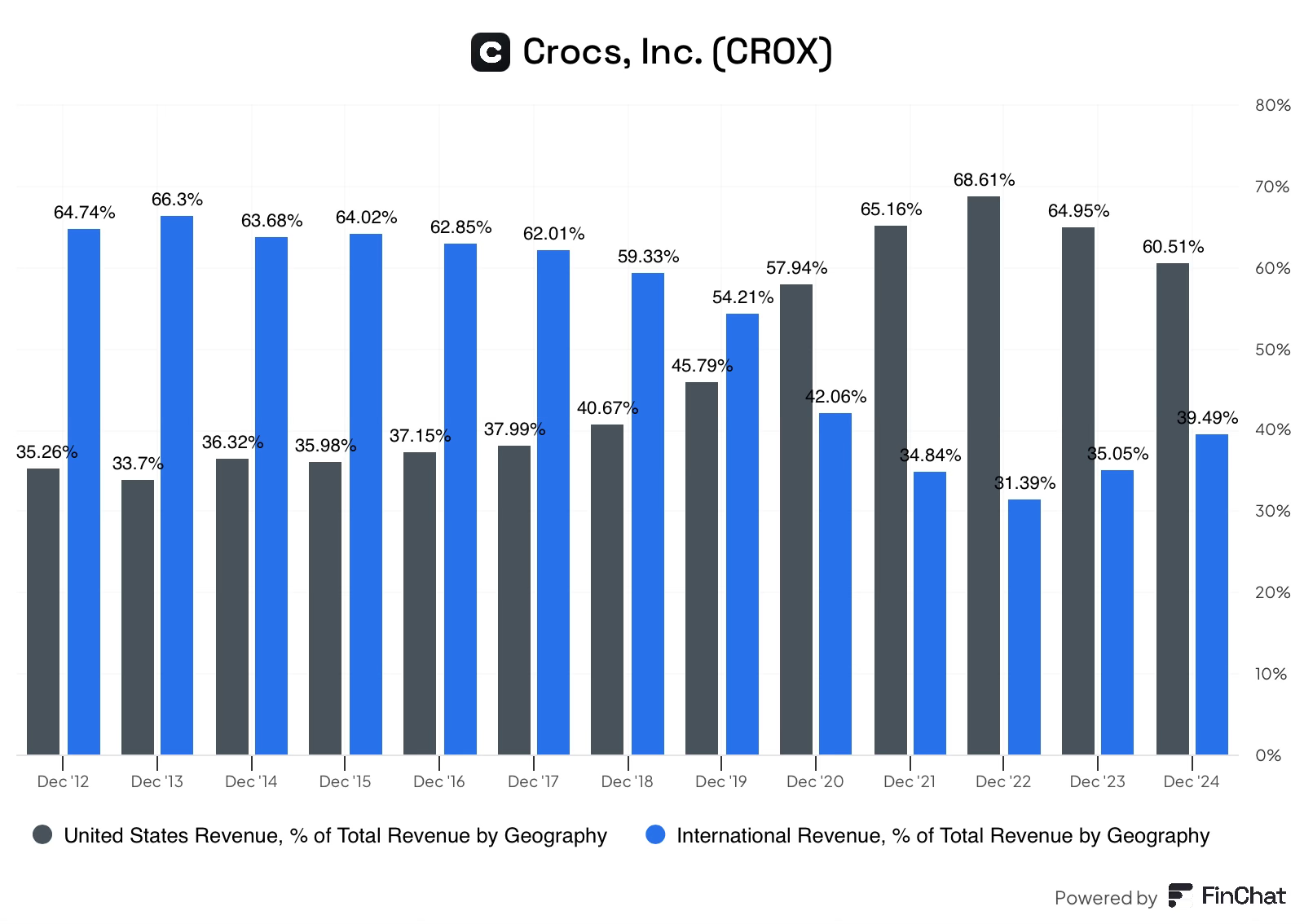

The company makes 60% of its revenue from North America; the rest comes from a diversified International base of more than 80 countries worldwide. The company considers China, India, Japan, South Korea, the US and Western Europe as key markets (Tier-1).

Why do consumers choose Crocs?

The company’s offering revolves around several key consumer trends, casualisation, comfort and personalisation, along with value. Both Crocs and Hey Dudes provide innovative designs that are designed to be comfortable and lightweight, often easy to slip off and on, making them convenient for everyday use.

The company’s product-led innovation has led to the expansion of product lines. The company offers variations of colour, materials, styles and increasingly products beyond the core clog for Crocs and Wally and Wendy for Hey Dude. These expanded product portfolios provide an offering to suit all consumer trends and wearing occasions. Jibbitz and Hey Makerz further allow consumers additional personalisation opportunities. This product innovation is common across both brands and is key to the company’s success.

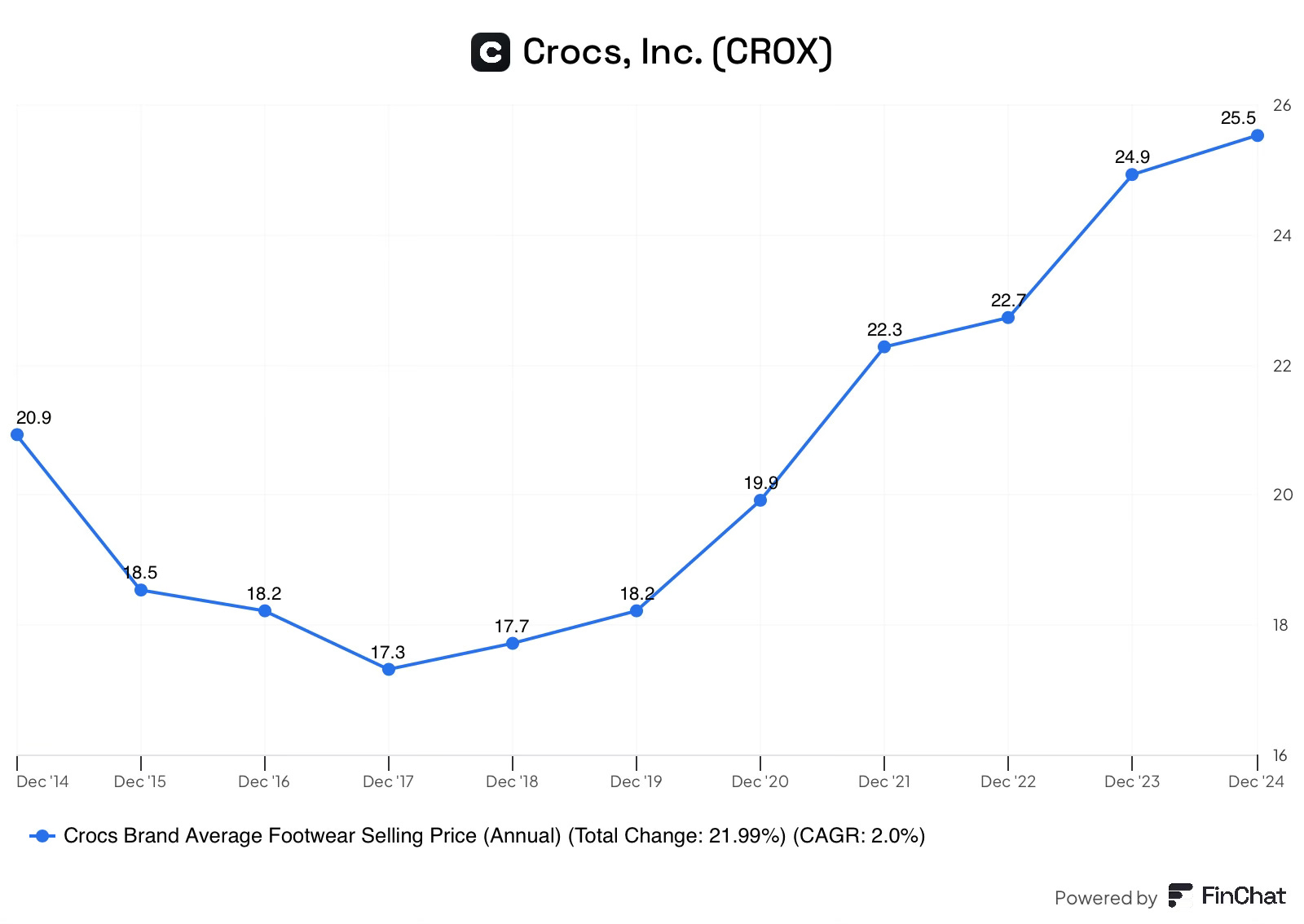

Value is also a key consideration in the consumer purchase decision. The company offers both brands at attractive price points. The company aims to keep the entire range of products below $100, the average selling price for Crocs is $25.52, and $30.54 for Hey Dude. These price points are considerably lower than other casual footwear providers and potentially allow the company to increase ASPs over time with minimal friction.

During the current management tenure, the company has increased the average selling price of Crocs by 6% annually (since 2017). However, management has signalled that there will likely be fewer increases over the near term meaning investors should not rely on pricing power in the short-term.

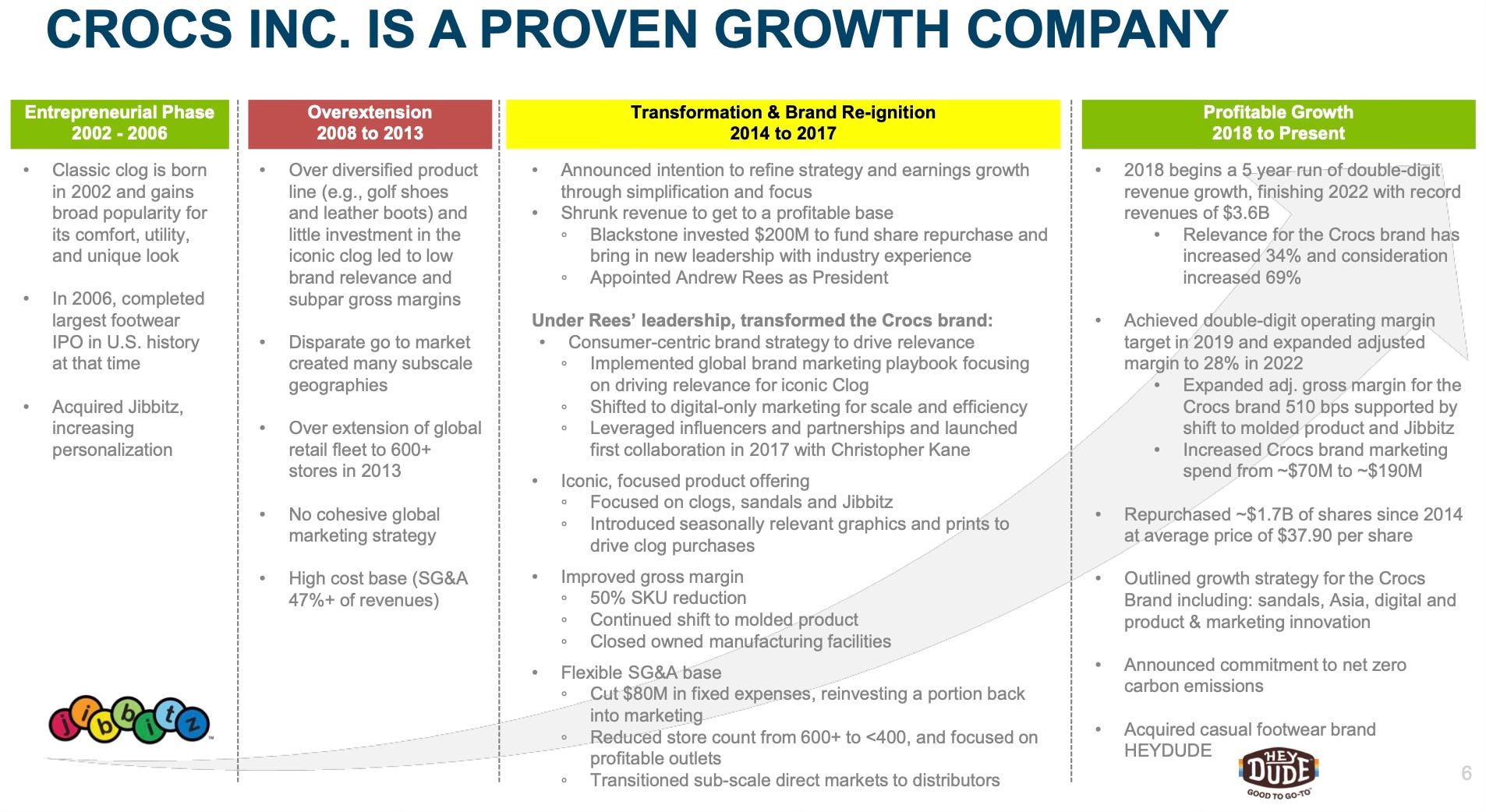

History - Turning the brand around

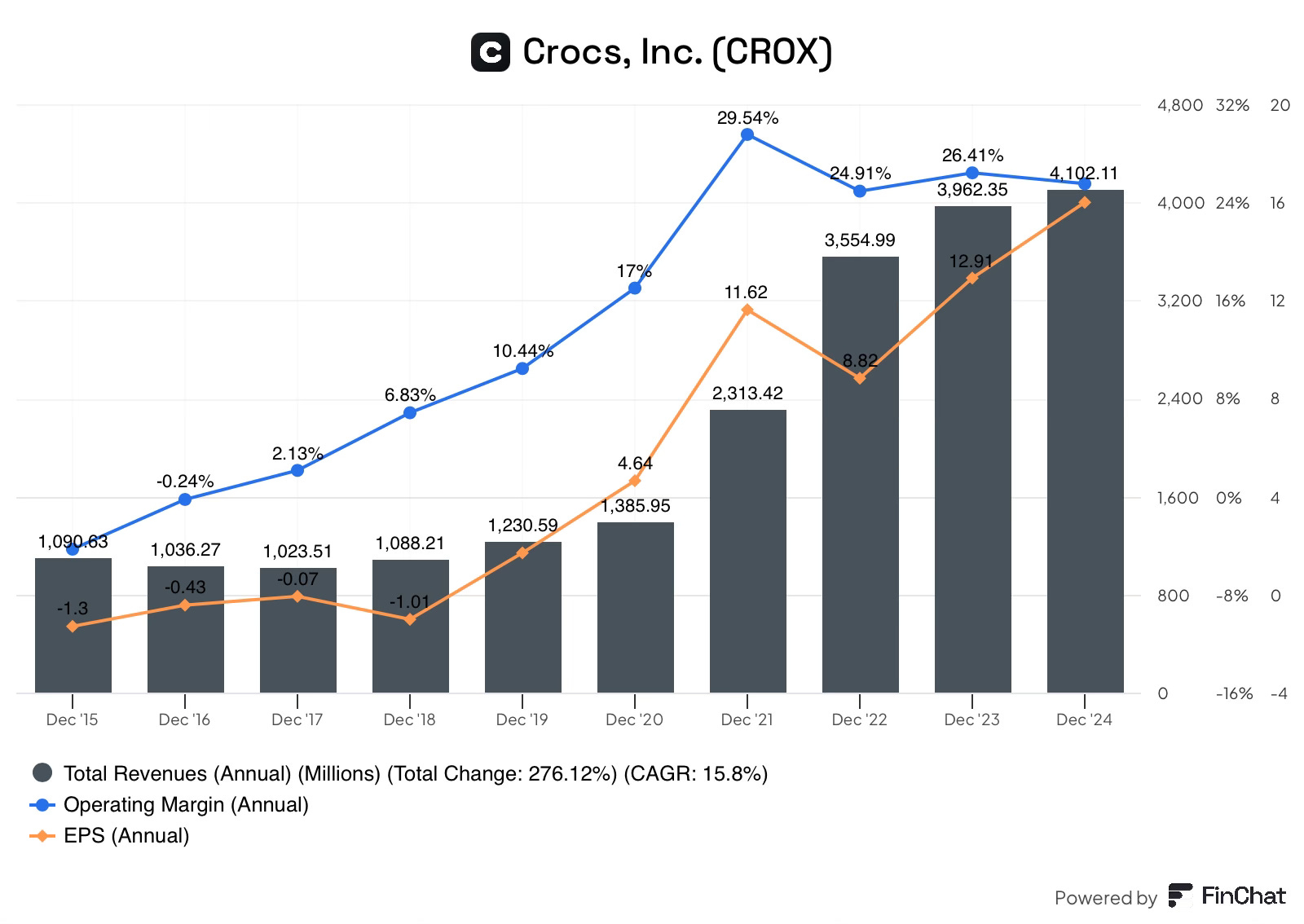

Croc’s history can be divided into 2, first, the initial rise to fame, followed by a turnaround of the struggling business in the mid-2010s. Since the company began its turnaround in 2014, revenue has compounded at 16%.

Crocs was founded in 2002 and experienced rapid growth in the years following, allowing it to go public in 2006, just four years after its launch. During this rapid growth period, the company expanded in an undisciplined manner, overextending the brand, over-distributing geographically, and opening far too many unprofitable stores, leading to losses, a bloated cost base and a confused brand image. This expansion, faster than the business could handle, led to the 2010s being a stagnant period for the company.

In 2014, Blackstone made a major $200m investment and changed the entire management team. This led to the hiring of Andrew Rees, first as president until 2017, then CEO, which he remains today. To turn the brand around, the company refocused on the classic clog, driving innovation through the core and shedding low-quality revenue, pivoted its marketing strategy into a “socially digitally led” approach, and cut SG&A spending, re-engineering the cost base. During the turnaround, the company repurchased shares, demonstrating confidence in the brand’s trajectory, this benefitted shareholders who stuck around tremendously.

In 2018, the company began to see the benefits of these actions; growth inflected positive, brand relevance improved, and profits began to rise.

The pandemic in 2020 turbo-charged this newly found growth; as consumers worked from home, they demanded footwear that was comfortable and casual, causing revenue to double in two years. Between 2020 and 2022, revenue increased from $1.4B to $2.7B. This significant growth created the narrative that the company was experiencing a pandemic-fueled bubble that would eventually pop, sending revenue back to pre-pandemic levels. During this time period, Crocs also acquired Hey Dude, a small brand that had seen a stratospheric rise in popularity in the years leading up to that point.

Over the following years, the Crocs brand remained robust despite investor doubts, growing in the high single digits. Management continued to employ the same product-led innovation and marketing playbook to the Crocs brand while integrating the Hey Dude brand.

What’s happening now?

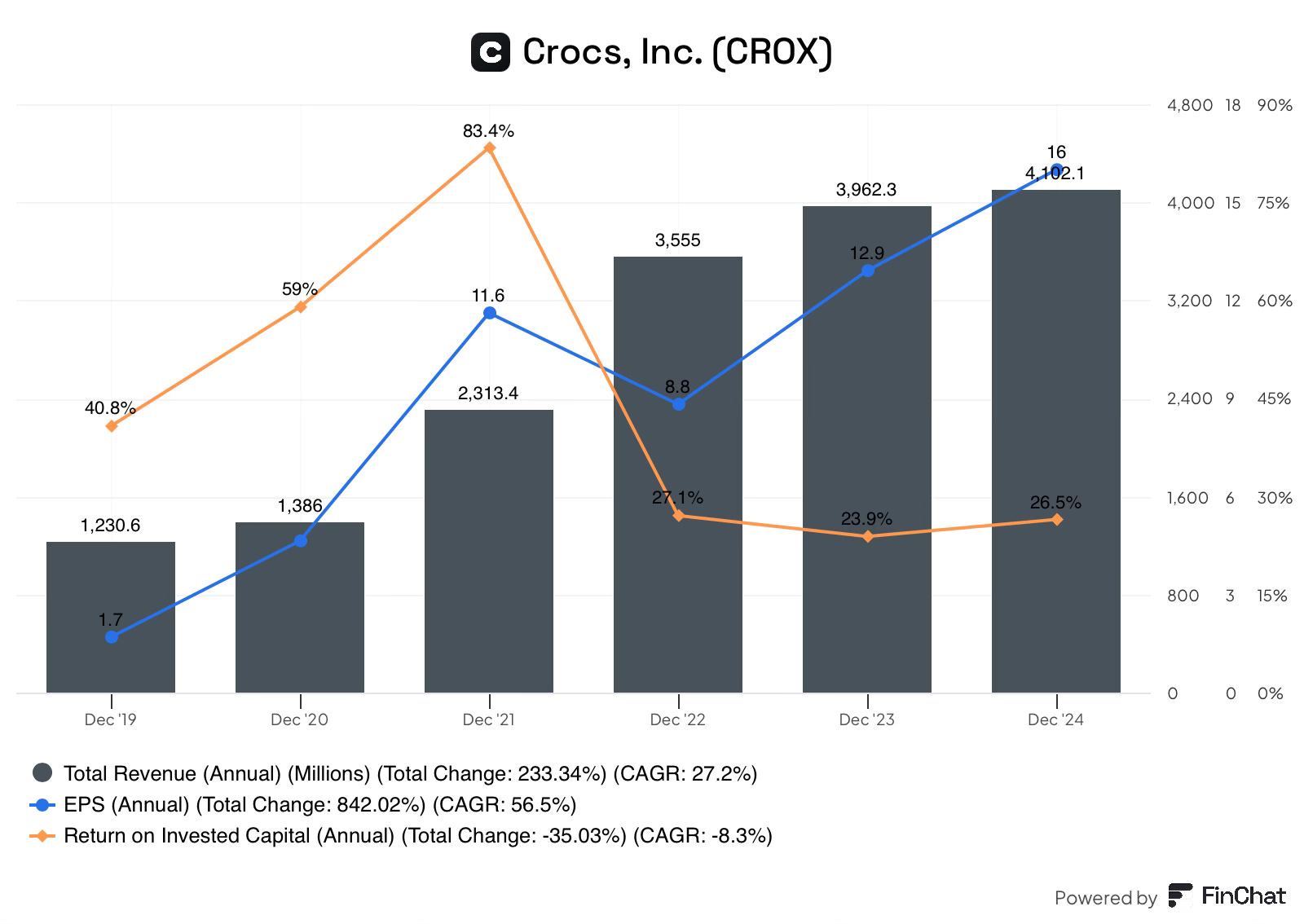

Since Andrew Rees took over, revenue has increased by 22% annually while expanding operating margins from -4% to 25%+. This has resulted in an EPS CAGR of 56% since 2019!

Despite the impressive financial track record led by the turnaround of the Crocs brand and the subsequent pandemic-fueled demand surge. The stock has underperformed the S&P 500 over the last one and three-year time frames.

The main reason for this underperformance is investor concerns surrounding the acquisition of Hey Dude. This acquisition has suppressed the growth of the Crocs brand, pressured margins while the company invests to turn the business around and impacted returns on invested capital.

The Crocs brand has also experienced slowing growth due to a weaker consumer environment in North America (56% of revenue) and China (6% of revenue), leading to a more promotional environment.

What went wrong at Hey Dude

Following the pandemic, the company made a bold move by acquiring Hey Dude for $2.5B, 15X EBITDA. At the time, the business had a run rate of roughly $570m, this had grown from $20m just 4 years ago!

The company saw initial success after the acquisition, the business almost doubled in a year from $570m to $950m in revenue.

This initial success soon faded. The company hit several hurdles, some of which were self-inflicted. The primary issues surrounded wholesale management. Heydude’s original distribution strategy (pre-acquisition) involved a large network of small regional accounts; at the peak, the company had 1,300 distributors. The goal of this was to penetrate markets quickly. However, it was likely a short-sighted solution due to the lack of scalability over the long term.

Following the acquisition, management looked to quickly capture shelf space, retailers were frequently running out of stock and requesting more, in response, Crocs increased shipments. However, the brand overestimated demand and the company quickly ran into two problems;

The company had shipped too many products, flooding channels with inventory.

The company had too many distributors with little segmentation, resulting in key customers competing against each other, undermining customer accounts.

To remedy this situation, management began rationalising accounts, closing over 600 small accounts. While this likely improved segmentation, it created an immediate grey market issue for the company. E-commerce sites such as Amazon were flooded with cheap Hey Dudes, undercutting the full selling prices of official accounts and wholesale partnerships. The source of this grey market was cut-off legacy distributors, of which the company did not have a full view of the inventory levels these old accounts held, trying to get rid of inventory they no longer needed.

While the company initially tried to compete with these lower prices, it quickly pivoted, which meant giving up short-term revenue to preserve brand health.

Beyond the inventory issues, the company also faced issues integrating the business. When Crocs acquired the brand, the backend was unsophisticated, despite achieving $570m in revenue. A few examples of this, The business still used Quickbooks for accounting. Despite going from $20m in revenue to $570 in 4 years, the business did not have a marketing department, instead relying on word of mouth, while extremely impressive, marketing would be required to take the business to the next level. Additionally, the brand came with very little infrastructure, leaving it with subpar distribution capabilities.

To position the brand for the future, the business has invested heavily in improving Hey Dude’s capabilities, these investments include;

Replacing Quickbooks with a stable ERP system

Expanding the Hey Dude distribution centre in Las Vegas, which opened in 2023.

Improving inventory management, the business can now achieve 4 turns per year.

Moving headquarters from Hong Kong to Boston and hiring 150 people.

Implementing a marketing strategy.

Both the inventory and implementation issues have created significant headwinds to the top and bottom lines of the consolidated financial results.

Crocs slowdown

Beyond the HeyDude-specific issues, the company has experienced a softening of consumer trends. Elevated interest rates and inflation have led to an environment of cautious consumer spending, which has reverted to pre-pandemic patterns where consumers typically only spend around retail holidays. These macro trends have disproportionately affected the North American business due to its high penetration of the market.

The business has also faced headwinds internationally from, distributor issues, which resulted in a significant distributor serving Africa being terminated. FX headwinds, supply chain disruptions and the same cautious consumer trends are all also impacting the segment’s growth.

Margin compression

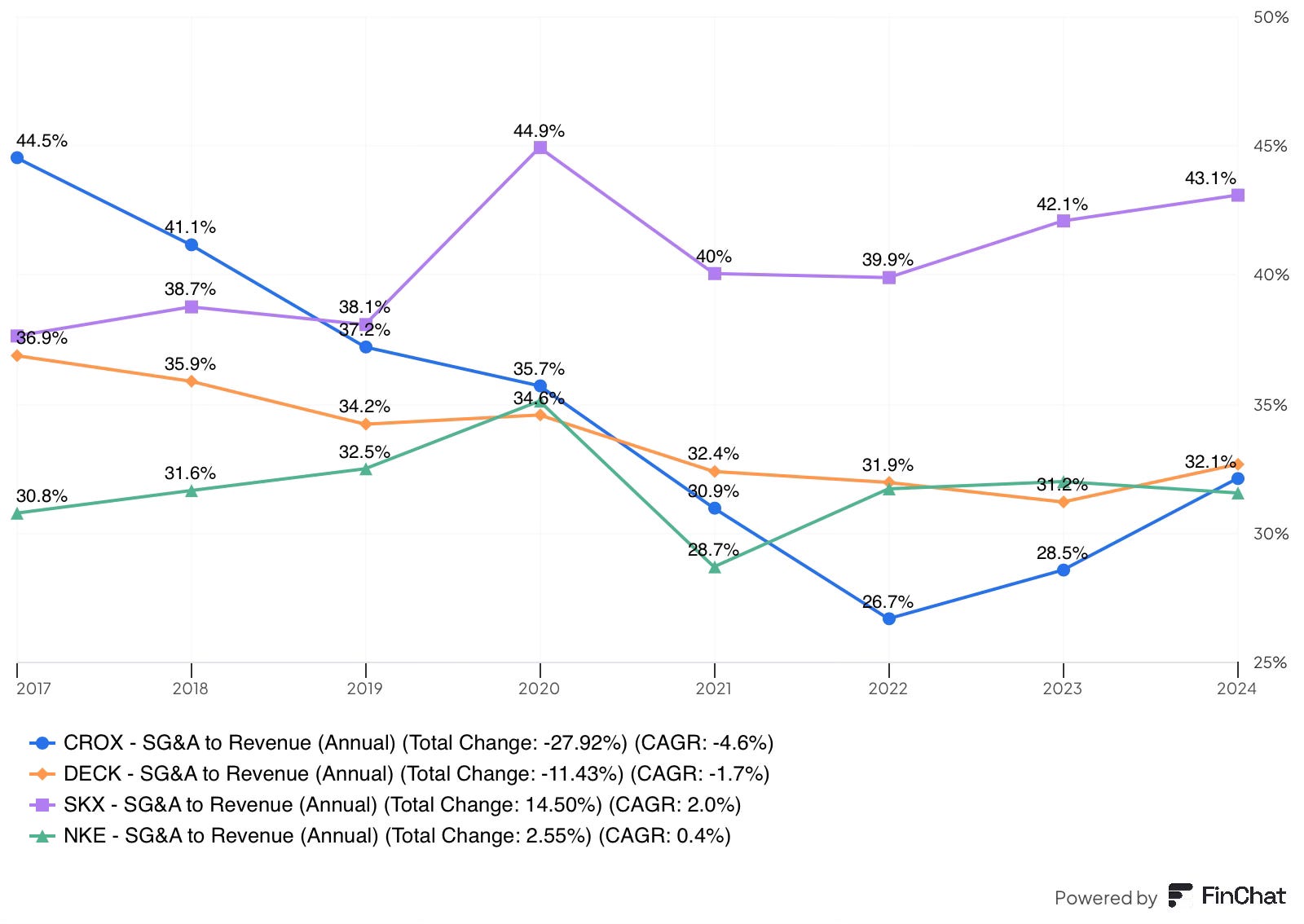

The business is highly profitable thanks to its capital-light model and management’s focus on keeping SG&A costs low, allowing the business to earn operating margins of over 20%.

In Q4 2024, Crocs lowered the long-term operating margin floor from 26% to 24%. While the business has seen some deleveraging in the past two years, this can be explained by the company’s decision to increase investments for the long-term health of the brands, These investments include:

Hey Dude brand integration: The company has been stepping up investments in marketing, talent, facilities, and opening new stores.

DTC investments: Croc’s has been leaning into expanding its online presence to platforms such as Amazon and TikTok shop, these typically come with higher variable expenses.

Crocs marketing: The company has increased the marketing budget from 7-8% of sales to 10%.

While these investments have led to some short-term pressure, the company remains one of the most profitable in the industry, while also positioning the business for future margin expansion.

Financial Performance

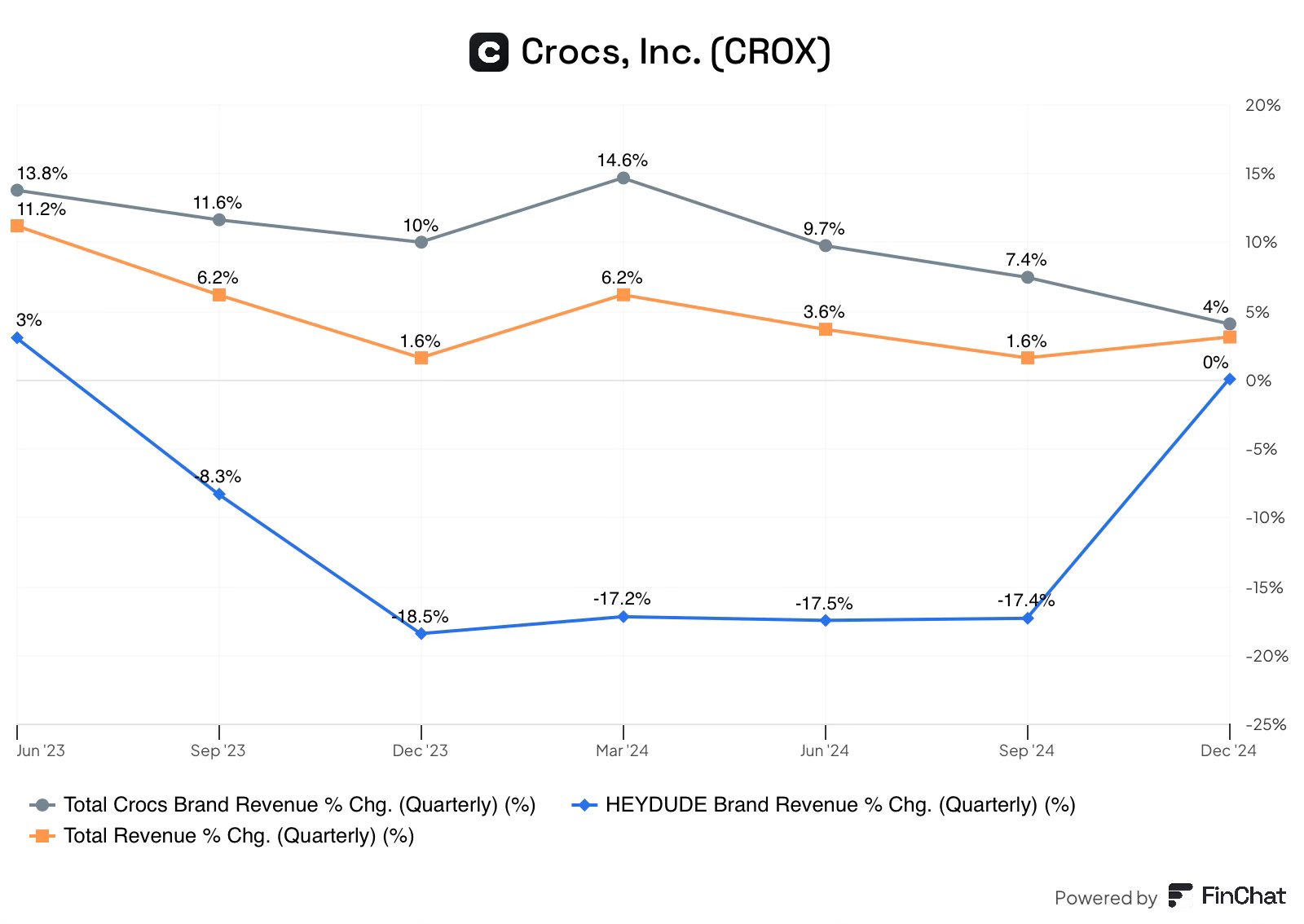

These above-mentioned headwinds have led to slower growth throughout 2023 & 2024.

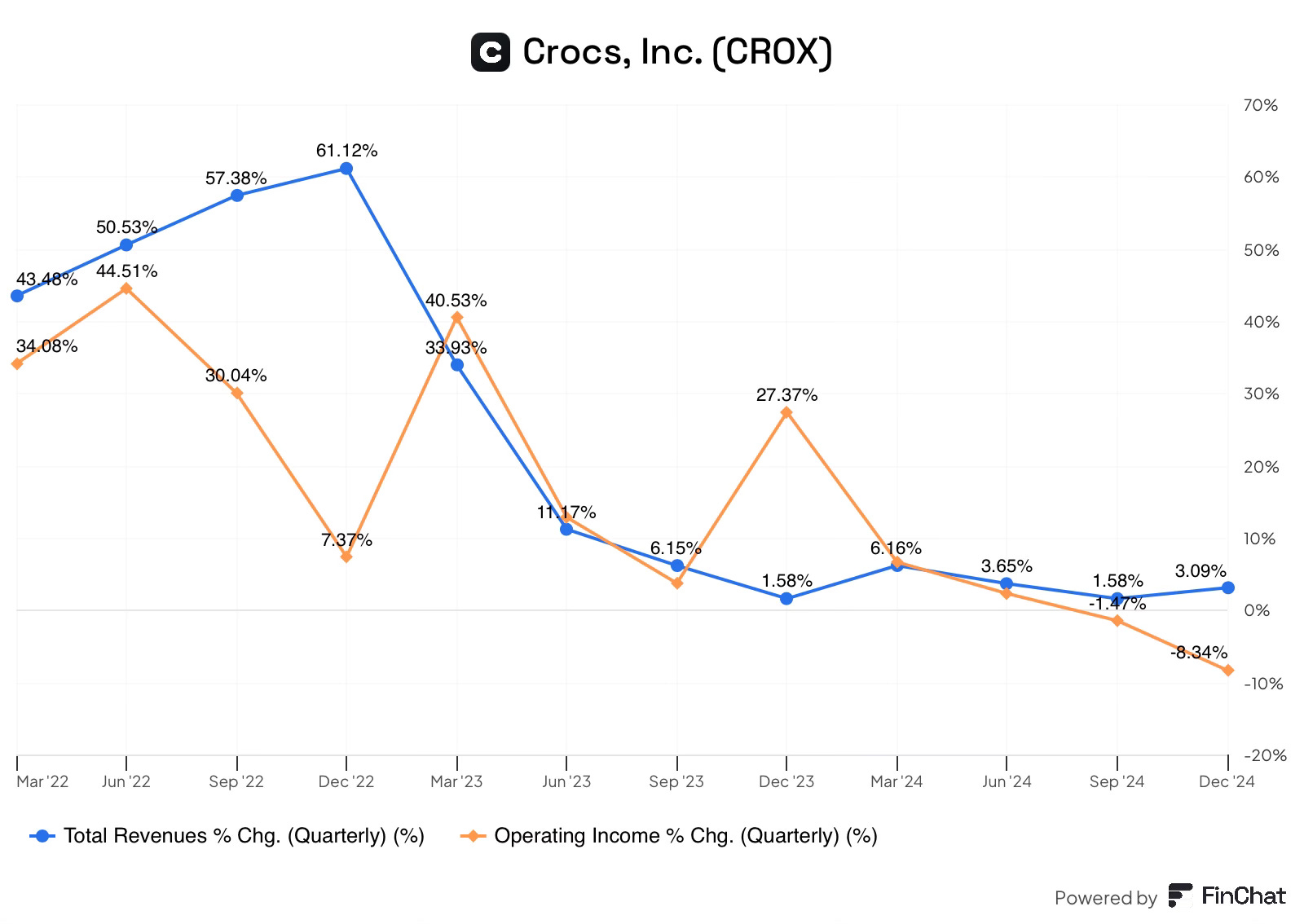

In Q4 2024, the business reported revenue of $990 million, a 3.1% increase (3.8% constant currency) YoY, a slight acceleration from Q3. For the full year revenue grew 3.5% (4.3% constant currency).

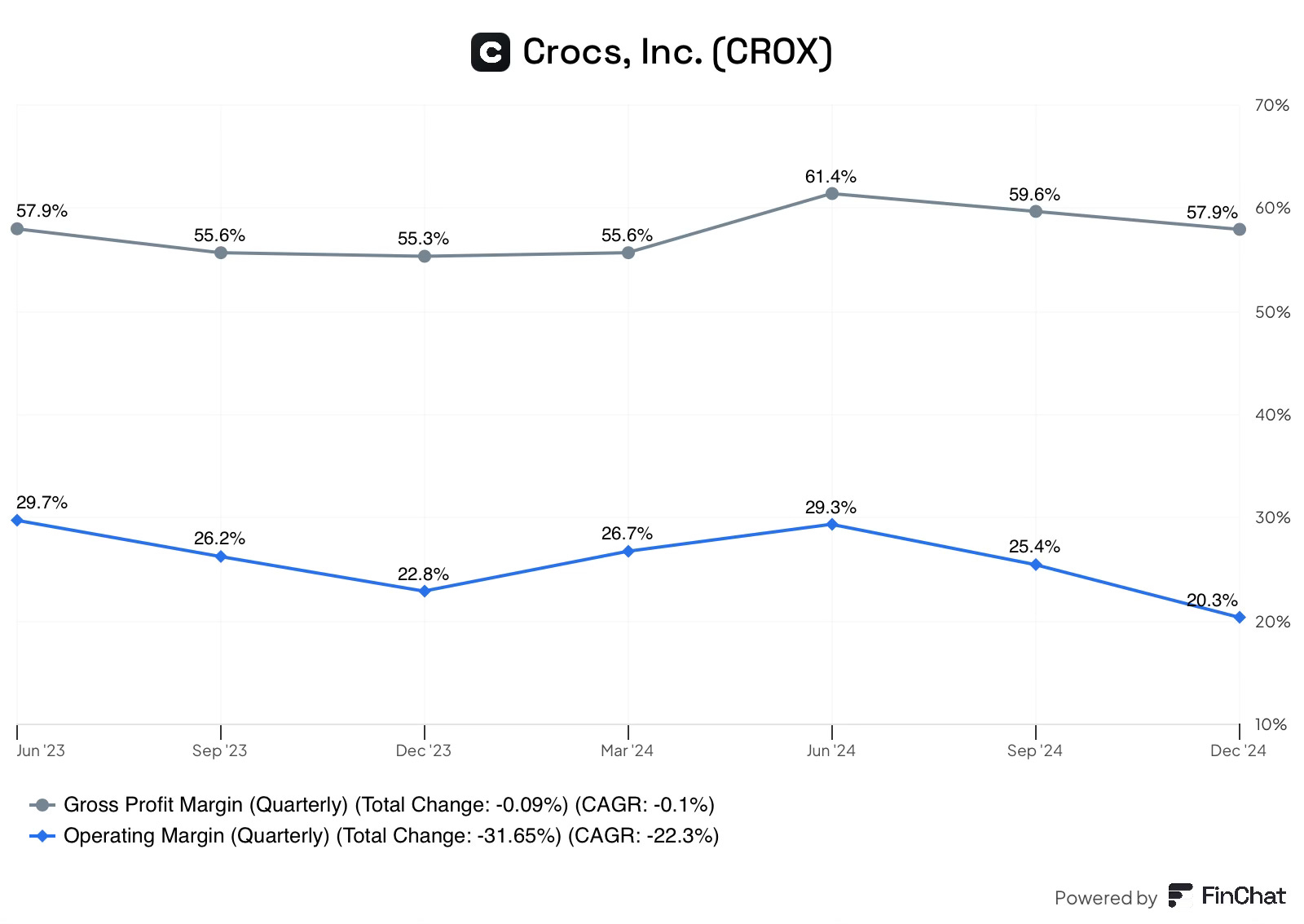

In Q4, Operating income decreased by 4.6%, driven by higher SG&A costs. For the full year, operating income decreased by 1% with full-year operating margins of 24.9%, a decline from 26.2% in the previous year. These higher costs were associated with increased investments across Hey Dude.

Brand performance

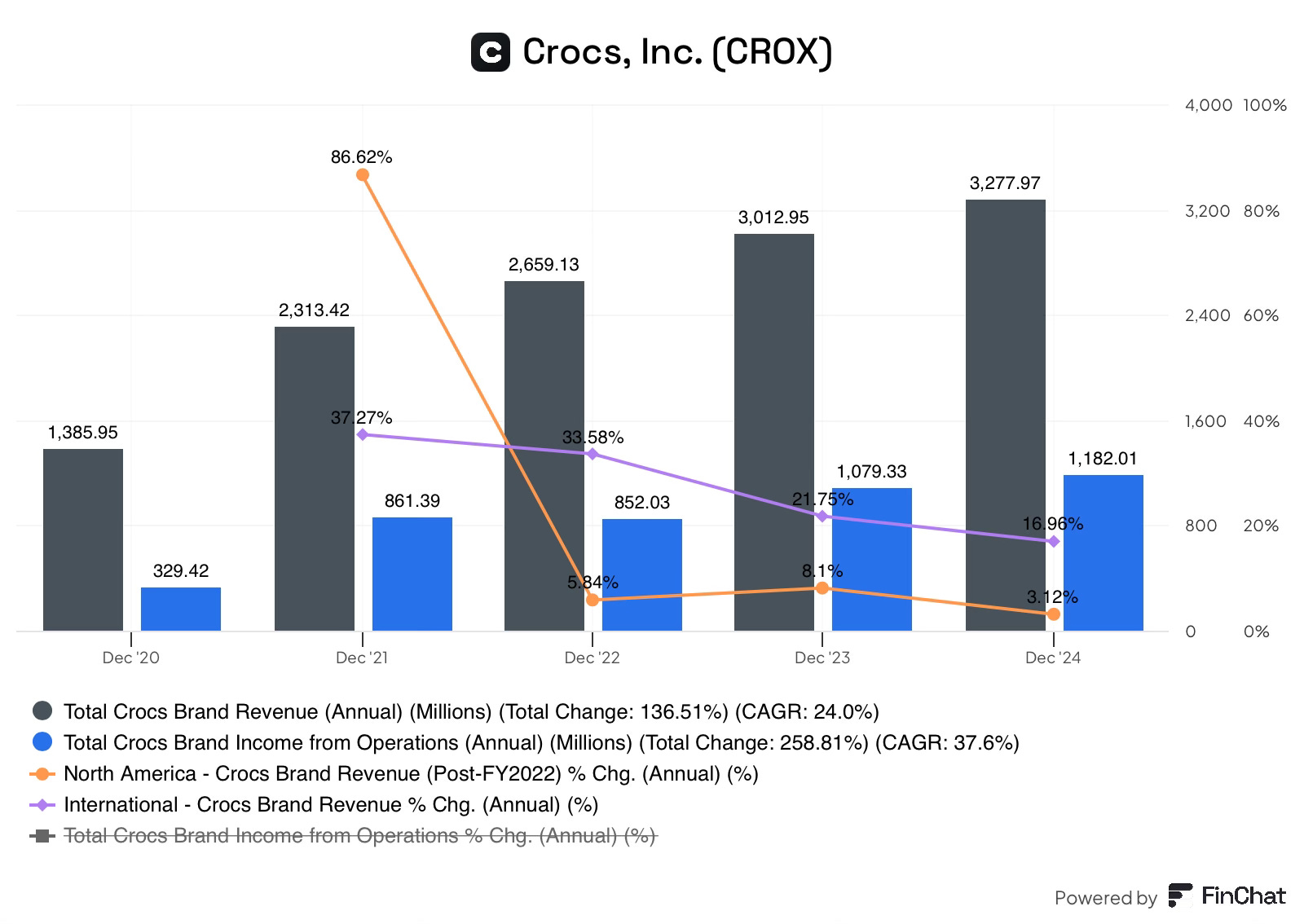

Crocs

Total Crocs revenue grew by 8.8% in 2024, driven by 6.2% growth in volumes and a 2.4% increase in the average selling price to $25.5. On a geographic basis:

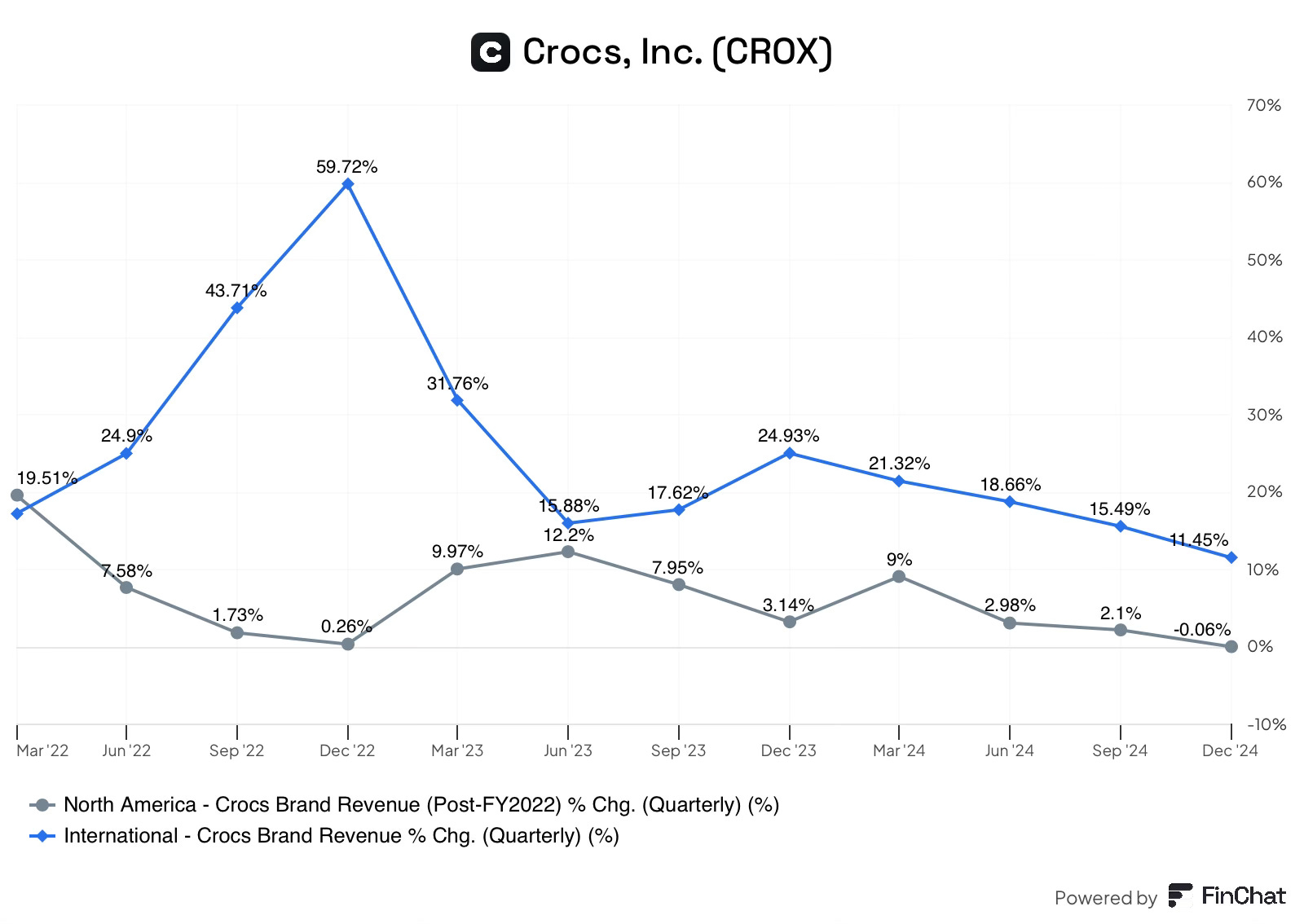

Crocs North America, grew 3% in 2024, but a weaker consumer environment persisted throughout the year, which affected the already well-penetrated Crocs brand.

Crocs International grew 17% in 2024 but slowed throughout the year due to weaker environments in China and FX headwinds. Growth throughout Europe, the Middle East, Africa and Latin America remained strong growing over 20%.

Crocs generated $1.2B in operating income, a 9.5% increase from 2023, representing a 36% operating margin, a slight increase from 35.8% in 2023, likely due to the higher ASP.

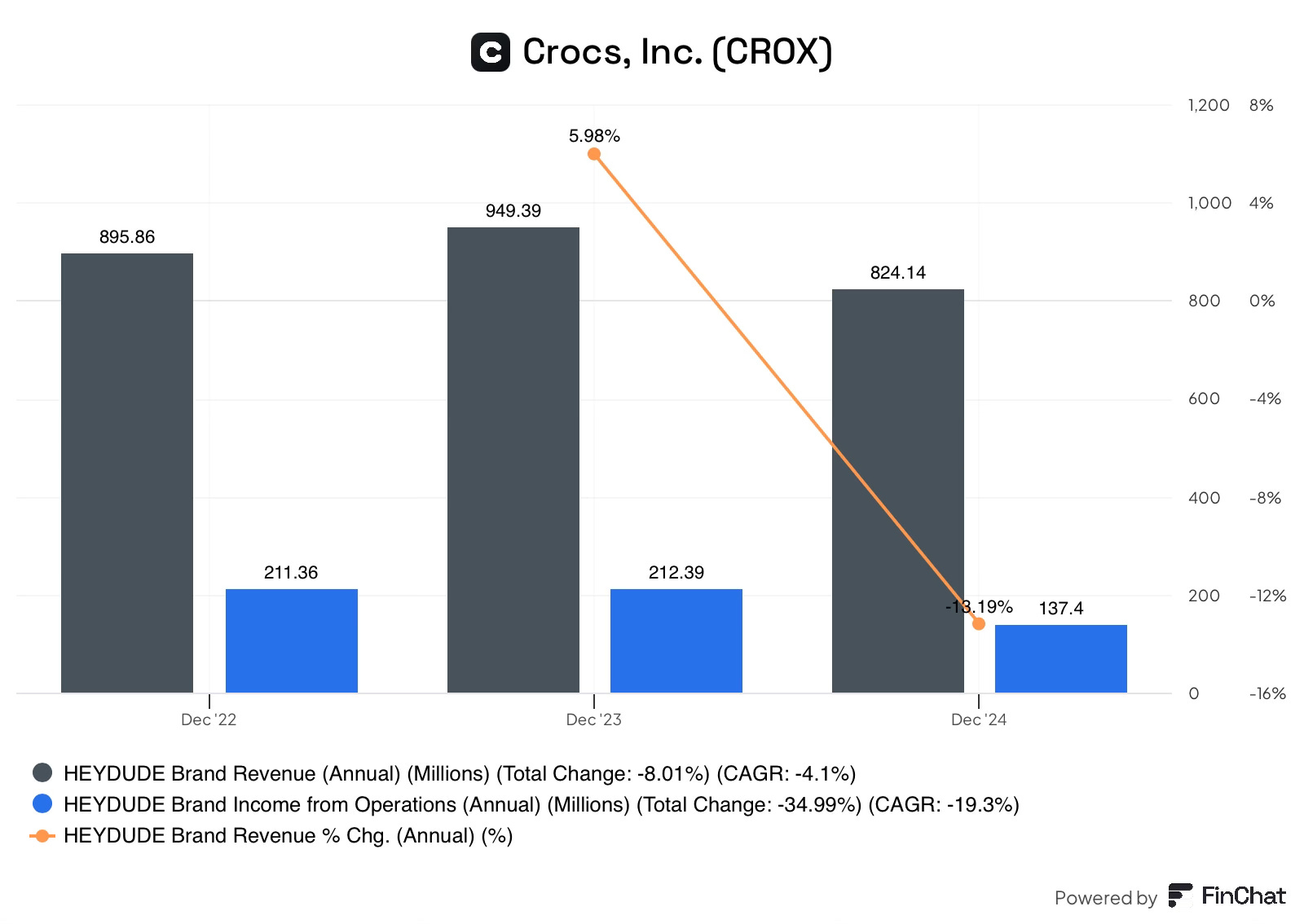

Hey Dude

Hey Dude, shrunk by 13% in 2024, as the company focused on brand health, inventory rationalisation and Average selling price stabilisation. In Q4 2024, The brand posted better than expected results, reporting flat revenue, a significant improvement from the -17% in Q3.

While Hey Dude's gross margins increased 370 basis points to 47.7%, income from operations decreased 35% to $137m. This decrease was driven by higher SG&A costs as the company invested in turning the business around.

The Investment case

Keeping the slowing performance of the past few years in mind, Crocs represents a compelling opportunity for investors at the current valuation. The business demonstrates quality characteristics such as industry-leading margins and high returns on invested capital. Management has a strong track record, first turning the Crocs brand around before executing its growth strategy. The business likely has several opportunities to sustain earnings per share growth over the long term from sources such as:

International expansion and expansion into new silhouettes within Crocs

The turnaround of Hey Dude

Share buybacks

I will analyse these opportunities in greater detail in the following section.

Competitive advantages

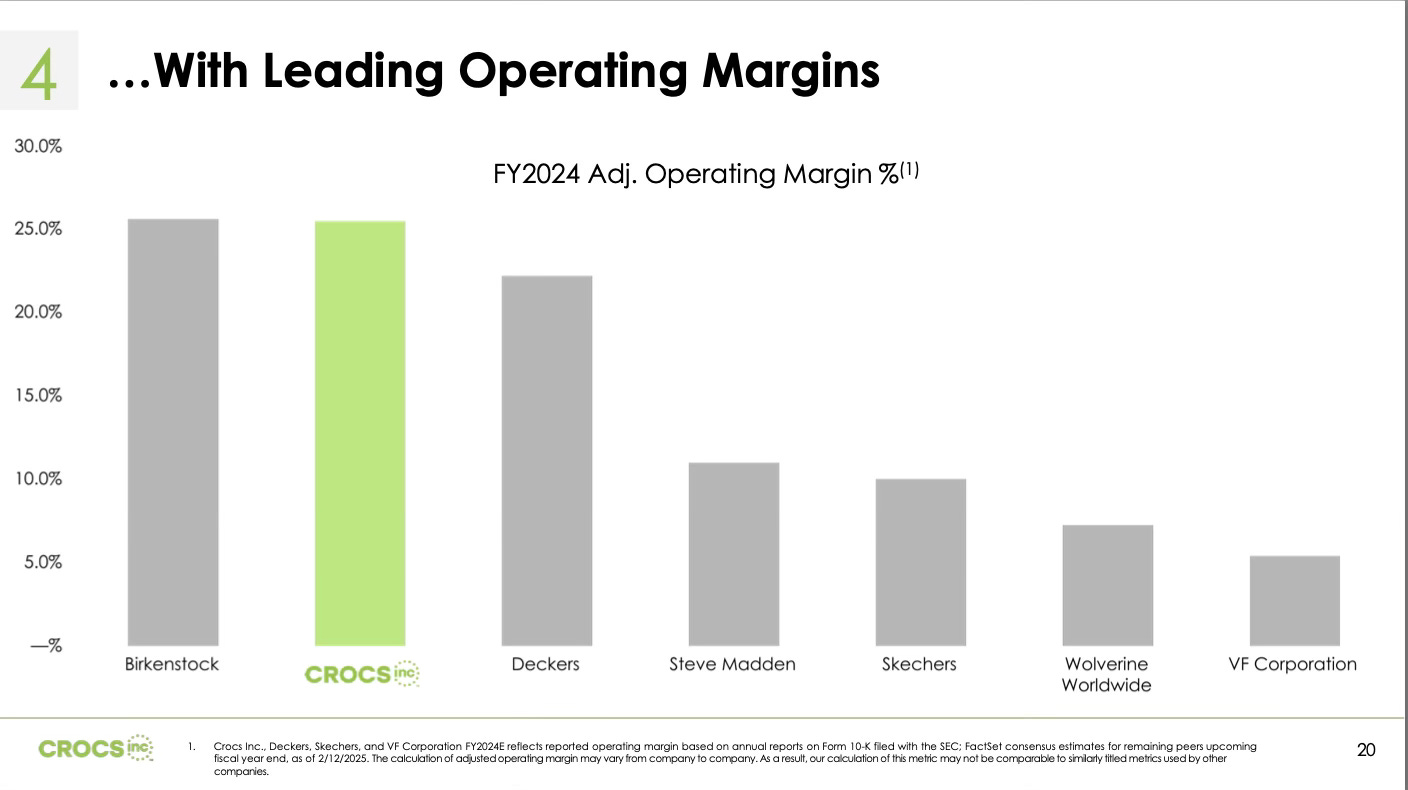

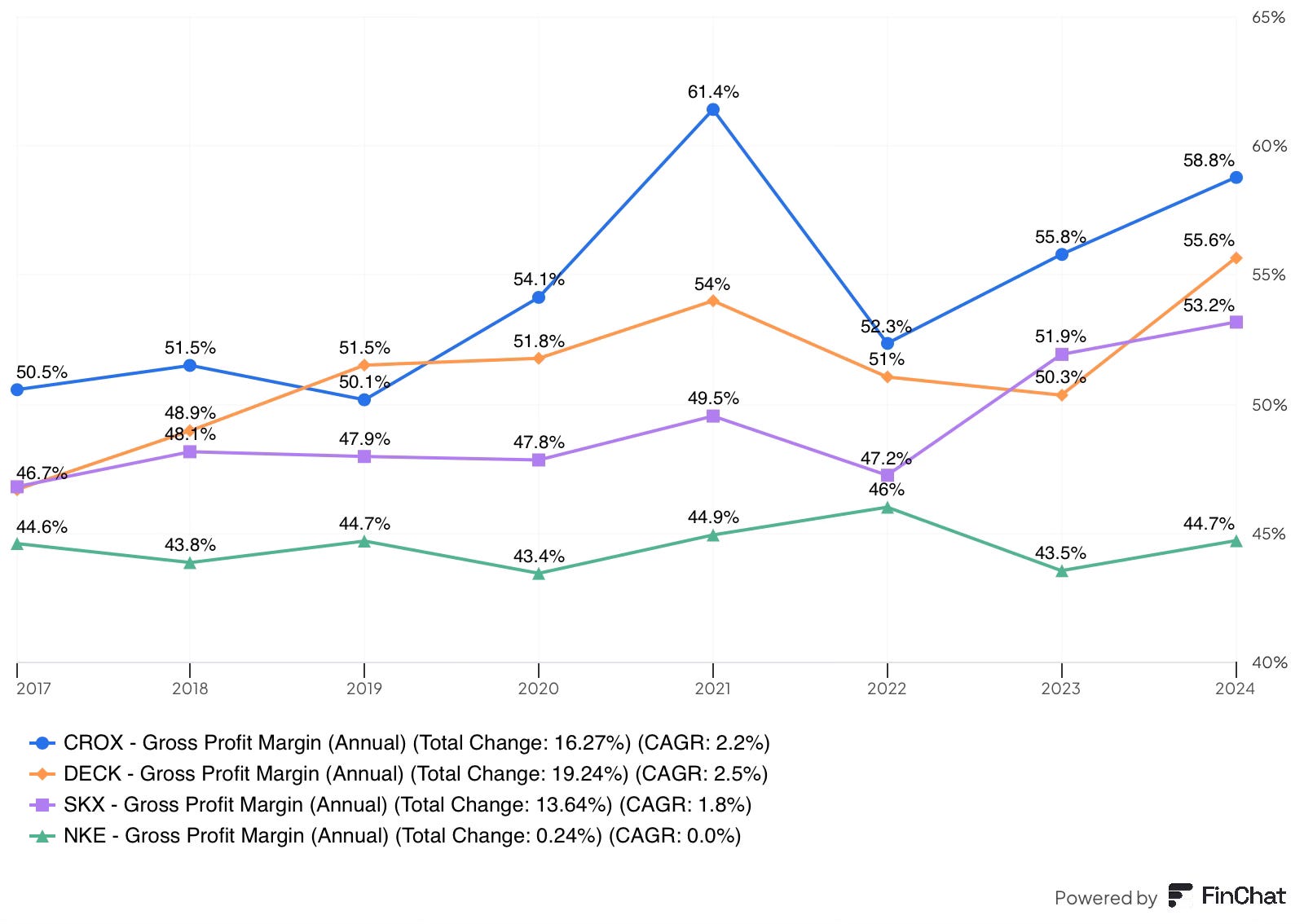

While Crocs competes in a highly competitive casual shoe industry, the company looks far different from its peers. These differences along with the capital-light nature allow the business to earn industry-leading margins and strong returns on invested capital while also selling products at the lowest average prices.

Over the past several years, Crocs has achieved operating margins of around 25%, only Birkenstock has topped this. This achievement is even more impressive when factoring in the average selling prices of the respective brands. Birkenstock is positioned as a premium product and often commands prices between $99 and $250, while Crocs’ average selling price is $25.52 and Hey Dude’s are $30.5.

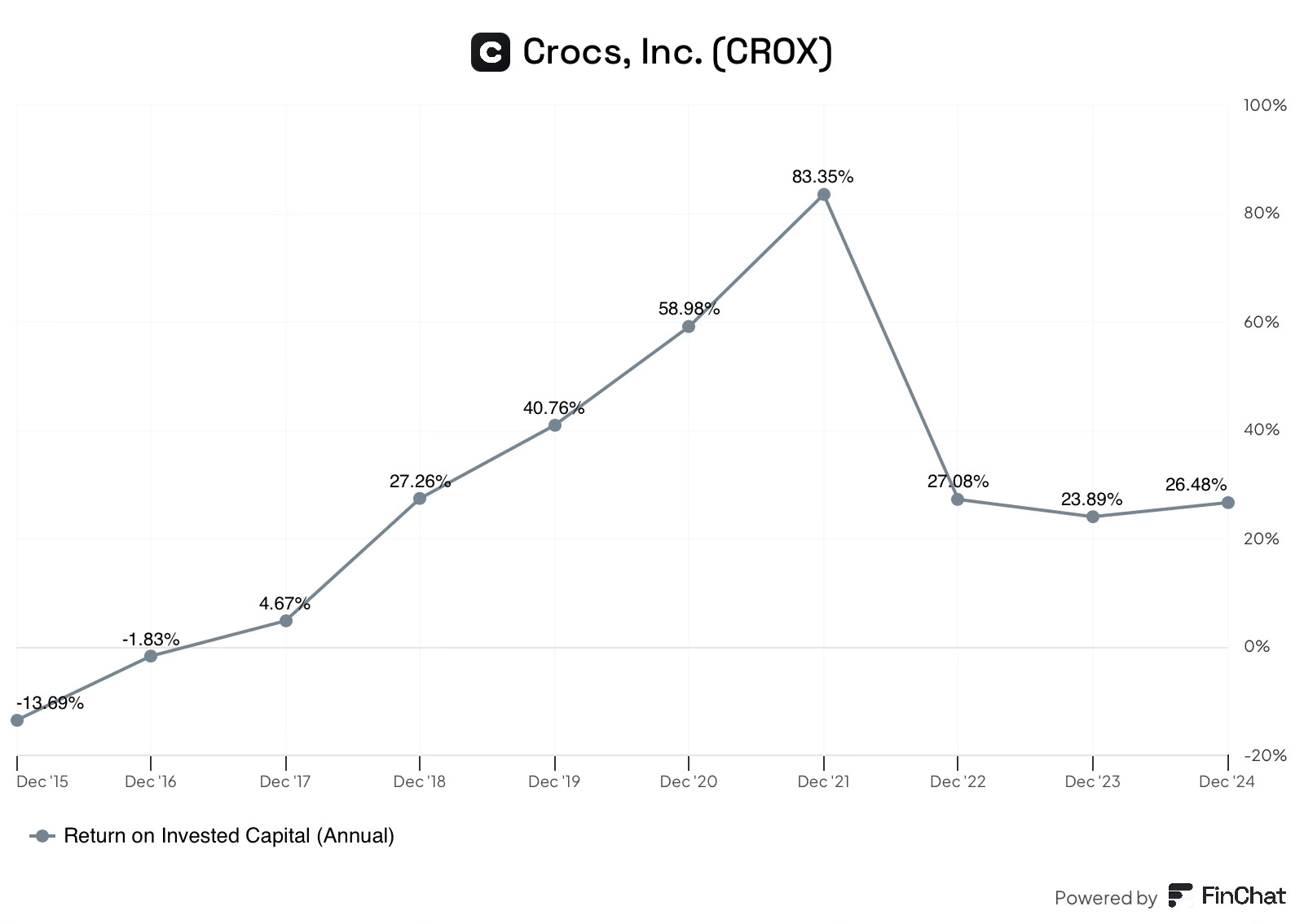

While total returns on invested capital (ROIC) have been brought down by the acquisition of Hey Dude in 2022, the Crocs brand is still generating ROIC north of 50%. The true returns Hey Dude can generate are still yet to be seen.

Two advantages allow the business to generate these high margins and strong returns.

Moulded Technology

While Crocs does not manufacture shoes themselves, the Cost of Goods is still one of the biggest line items. Most shoe companies use various types of canvas, rubber and stitching to manufacture shoes, this is time-intensive, difficult to automate and produces a lot of waste products.

Crocs on the other hand, utilises moulded technology using proprietary materials such as Croslite, LiteRide and Free Feel technology, which not only differentiates the look of the product but also offers versatility of use cases and durability. Using moulded technology allows the company to achieve economies of scale, reduce labour costs through automation, and be very efficient with materials, reducing wastage.

Another key advantage of this manufacturing process is the ability to iterate very quickly on product design, allowing the brand to offer different colours and patterns, something other brands can not do as easily.

This cost advantage allows Crocs to have the highest gross margins among peers, however, this does not tell the full story. Crocs includes freight costs in the cost of goods sold, while many peers do not. Excluding this cost, Crocs would likely extend its gross margin advantage over the competition.

Brand Value and Marketing Strategy

Crocs has fostered strong brand recognition around the globe, in part due to the controversial nature of the clog design and partly to management’s extreme focus on strengthening the brand through digital channels.

Controversiality: The classic clog has long been a talking point, you either love it or hate it. Those who view Crocs negatively often cite its perceived ugliness, while those for Crocs argue for their comfort, versatility and personalisation. Either way, the conversation and associated media attention is great for the brand.

Marketing: Crocs’ marketing strategy is a key differentiator. The business typically spends 7-8% of sales on marketing, which likely generates very high ROI by achieving significant media attention and engagement at a fraction of the dollar value larger competitors spend, this allows the business to punch well above its weight.

The company leverages social media platforms such as Instagram and TikTok to create social hype. Collaborations have been a core feature of this strategy, with partnerships ranging from McDonald's to K-pop bands and the movie Cars. These typically limited releases generally sell out instantly and generate significant media attention. Later these limited editions can typically be found on resale websites for several multiples of what the company has charged, demonstrating the appeal they drive.

This strategy has also allowed the company to attract younger demographics, keeping the brand relevant while also allowing the business to create brand value that is comparable with competitors with significantly more financial resources.

Both of these advantages allow the business to have the lowest cost base amongst peers, despite having less scale. With the business expected to continue growing, these advantages will allow Crocs to sustain their competitive position, and maintain industry-leading margins and healthy returns on invested capital.

Management

Crocs has a management team with a proven track record,

Background

Andrew Rees has over 25 years of experience in the footwear and retail industry. Prior to joining Crocs as President in 2014, he was a managing director at L.E.K consulting where he founded and led the retail and consumer products practice for 13 years. Before that, he was VP of strategic planning at Reebok International.

Track record

Since Andrew Rees took over as CEO in 2017, he has achieved a revenue CAGR of 25% and EPS of 58%, while turning the business from loss-making to industry-leading margins by focusing on brand value. This has led to over $5.5 billion in value created for shareholders, given the market cap of$6.1B, this is an extremely impressive track record.

Ownership and Compensation

While insider ownership isn’t massive at roughly 3%, Rees owns just under 2% of the business, valued at $145m, with an estimated net worth of $159 million, he certainly has skin in the game.

Executives are paid a base salary and receive incentives via a mix of an annual bonus award and long-term equity grants. To achieve these awards, the company focuses on financial metrics and strategic initiatives.

The financial metrics include adjusted EBIT of the enterprise, Crocs and Hey Dude along with Free Cash flow,

Strategic objectives include growth in Sandals and China, while Hey Dude is focused on inventory management and gross margin improvement.

While not perfect incentives, it is clear management is incentivised to grow Crocs and turn around Hey Dude, both of which align with the interests of shareholders.

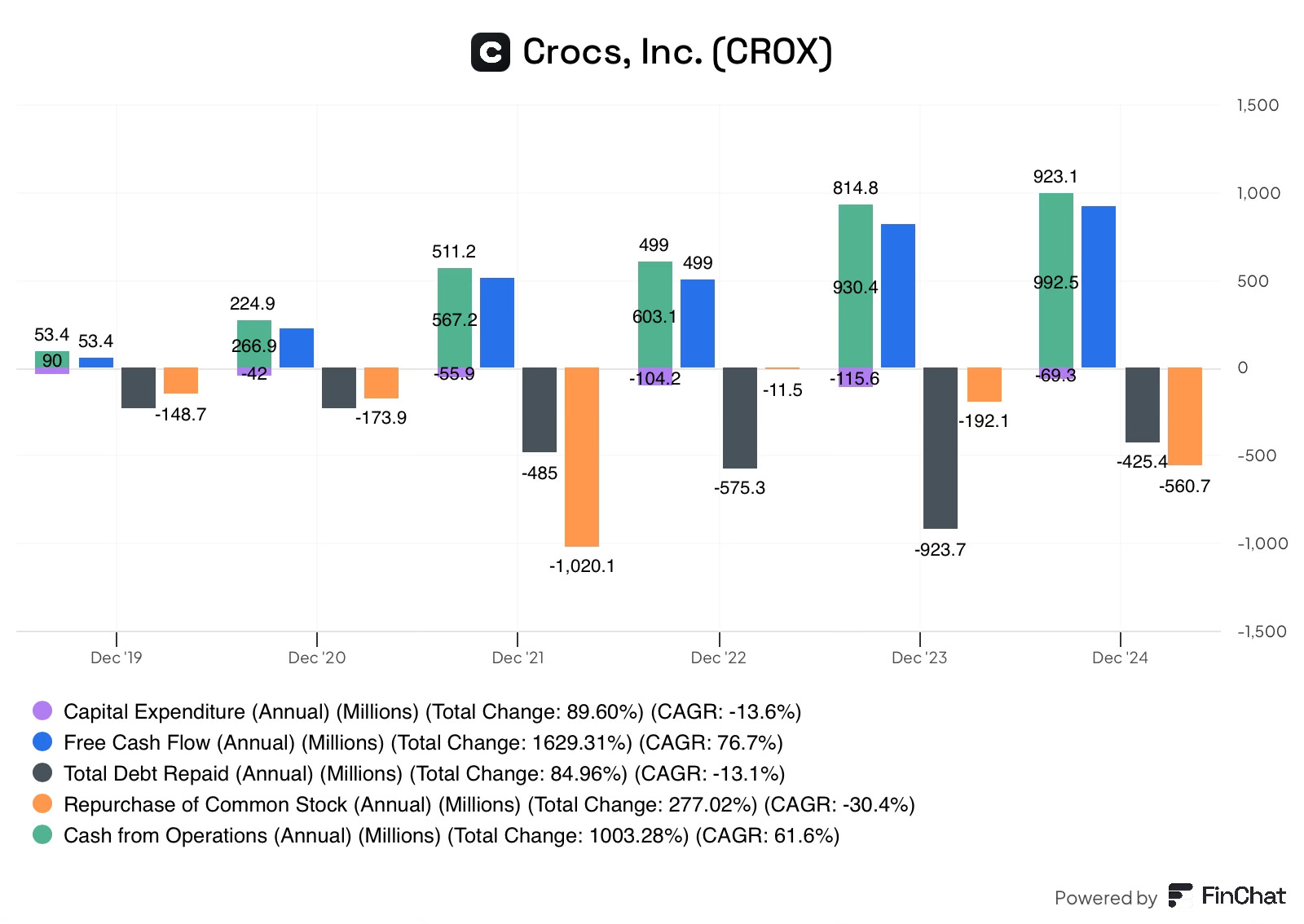

Capital Allocation

Management’s first capital allocation priority is to re-invest back into the business. The business is inherently capital-light, the company does not manufacture its own shoes, meaning the business is essentially a marketing and distribution engine. This makes the business highly cash flow generative.

Of the capital that does get re-invested, there are several areas to invest:

Brand building - Marketing campaigns and product innovation

Talent

International expansion

Inventory

Distribution capabilities

Technical capabilities

The majority of these are invested through the income statement, leaving the company with little Capex requirements, allowing the business to generate significant free cash flow.

The second and third priorities are maintaining a healthy balance sheet and returning cash to shareholders. Following the acquisition of Hey Dude, the company prioritised paying down debt, before returning cash to shareholders.

Opportunities

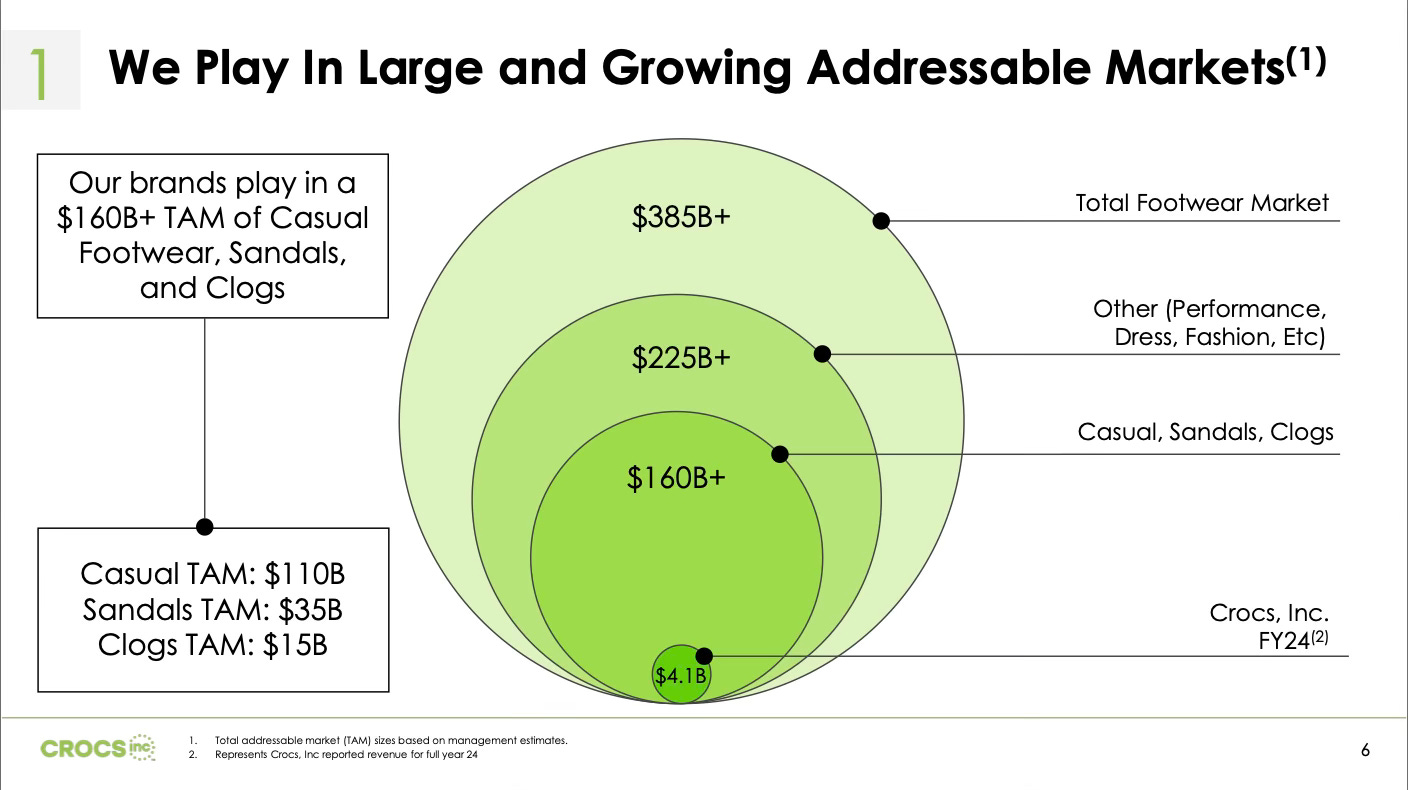

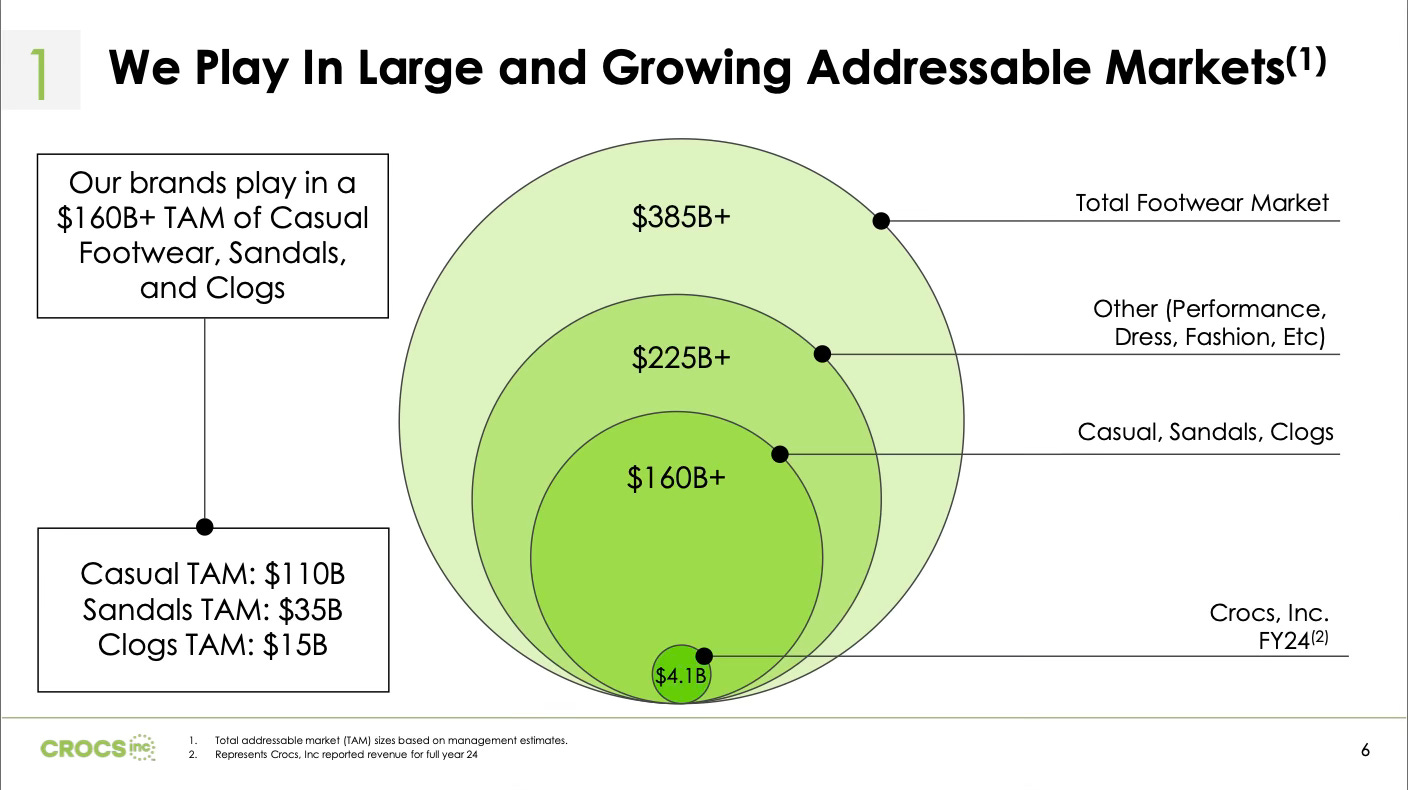

TAM

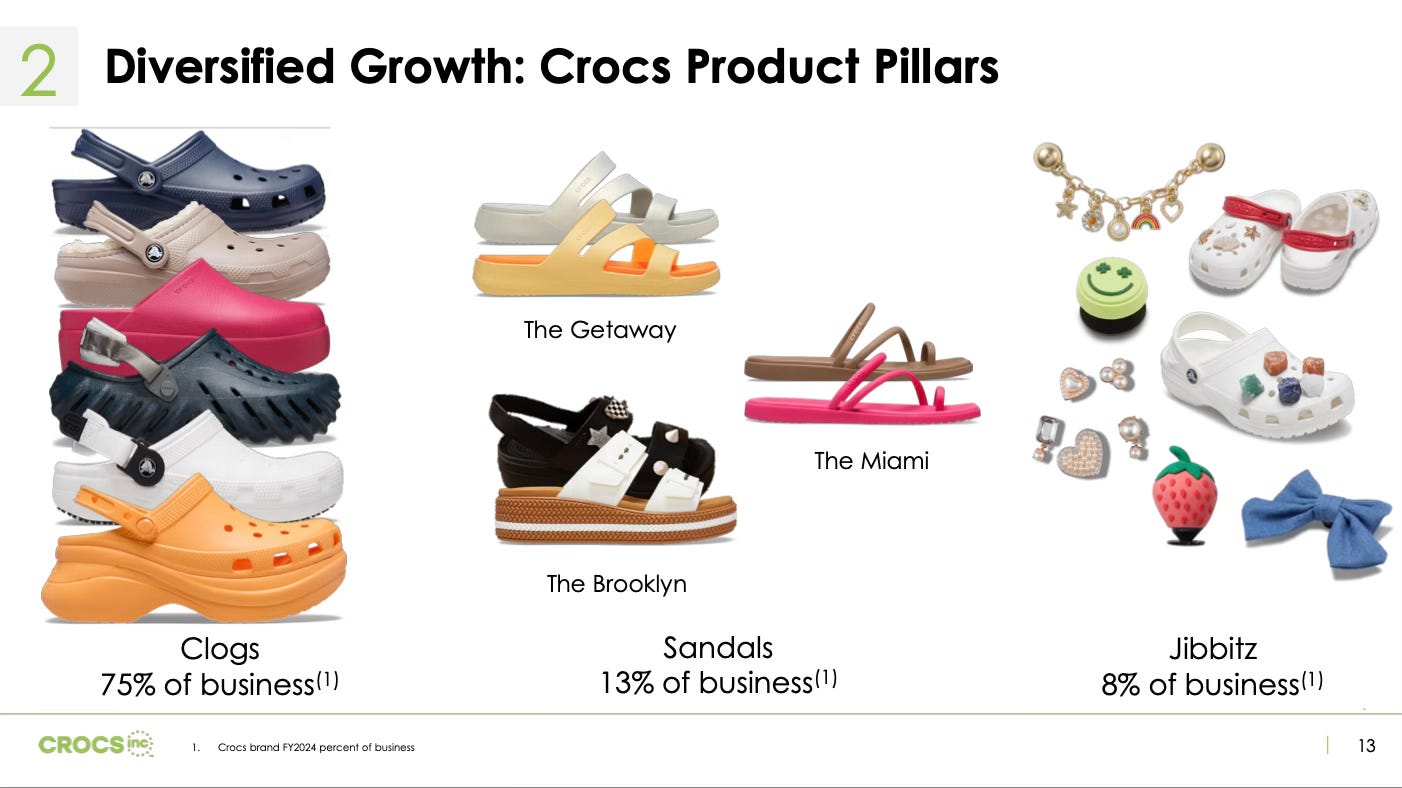

The business operates in the $160B+ casual footwear industry. The total business generates $4.1B in revenue, however, the majority of this revenue ($2.25B+) comes from the classic clog, which represents just $15B of the total market. This representation likely means that Crocs expansion beyond Clogs and the acquisition of Hey Dude have significant headroom to grow, while Clogs are likely well saturated, especially in North America.

Crocs

Crocs represents 80% of the business today and remains the most important aspect, something that the share price doesn’t necessarily reflect. At a high level there are only 2 ways to grow the brand: sell more shoes (volume) and charge more.

While I expect the North American brand to continue growing modestly in the future through a combination of both volume and price, the business has been likened by management to a cash cow, giving them the cash to invest in both International and Hey Dude. This suggests growth of the core business will likely be limited over the next few years. In the long term, the North American business will likely benefit from the company’s expansion into Sandals and sneakers, which represent just 13% of revenue today, this will likely take time to become evident.

Future Crocs brand growth will likely come from;

International expansion

expansion beyond the core Clog (longer term).

modest pricing power

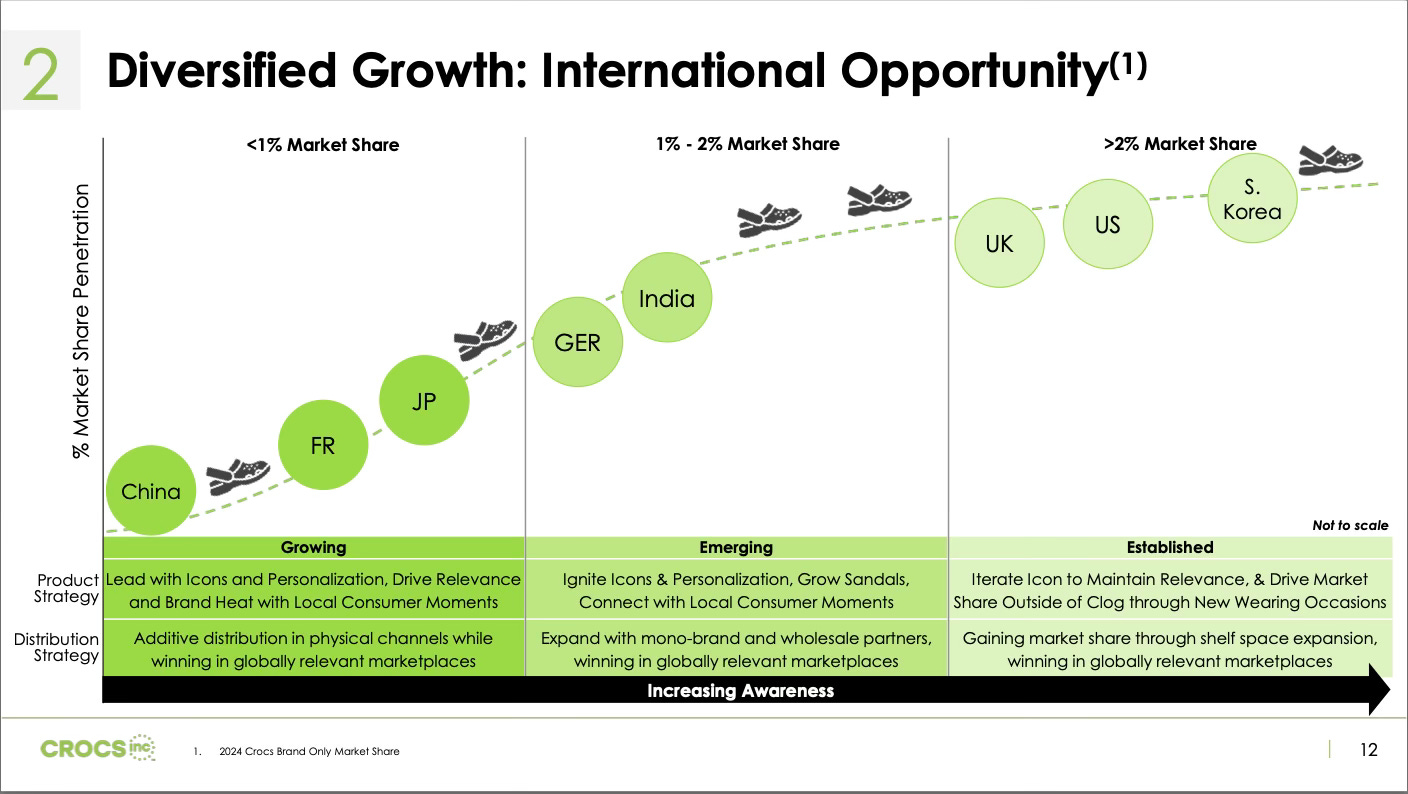

International

International revenue currently makes up 44% of total brand sales and represents the biggest growth opportunity for future growth. While the brand is well penetrated in the US, UK and South Korea, market share in major International countries is approximately one-quarter of that. If correct, the International business could theoretically quadruple from current levels, representing a roughly $6B opportunity. This growth would more than double total brand sales.

In 2024, International growth contributed two-thirds of total brand growth. In future years, this contribution will likely further increase, with double-digit revenue likely sustainable.

Crocs is currently focused on Tier-1 markets, which include the US, UK, Japan, South Korea, Germany, India, China and France. However, there are likely two markets that will drive future growth: China and India.

China: China is the second largest market for the company, making up 6% of sales. The country has been on a rapid growth trajectory over the past few years, in 2024 China grew 64%, on top of triple-digit growth in 2023!

In Q3, the company reported a slowdown due to more cautious consumer behaviour in Tier 1 cities such as Beijing and Shanghai, resulting in growth of 20% y/y. While this growth re-accelerated in Q4 to 25%, it remains meaningfully below recent growth rates.

A primary driver for the growth in China is their expansion of partner-operated stores (mono-brand stores). At the end of 2024, the company had nearly 400 of these stores, of which over 150 had been opened this year, almost doubling the footprint. These stores likely take at least a year to hit their full revenue potential, suggesting the potential for growth to accelerate in 2025. Despite a potential acceleration, The company is unlikely to reach these triple-digit growth rates of the last few years.

Nike, likely the most recognised Shoe brand in the world, currently generates revenue from China which is one-third of North America. Given Crocs’ well-known brand and significant traction, I see no reason why Crocs couldn’t also generate a similar contribution from China.

China currently represents 6% of the Crocs brand, generating revenue of roughly $200 million, while Crocs’ North American business generates over $1.8B in sales. Given the same one-third weighting, China could become a $600m business, a 2X from current levels.

India: The country is likely a huge opportunity for the company, given the enormous population. Recently, the company has made some changes to its go-to market in the country that will likely drive significant growth in the future.

The company has shifted some of its manufacturing footprint into India from places such as China and Vietnam. While only partly operational, the ramp will continue throughout the year. This manufacturing footprint shift has significant implications. Under the rules of the “Make in India” scheme, Crocs is now able to sell directly to consumers (DTC), previously it had to go through wholesale channels.

Historically, Crocs worked with one major franchise store operator, Metro. With manufacturing now in place, Crocs is shifting a lot of their digital platforms to be directly operated. This DTC model will be able to benefit from the company’s innovative marketing strategy, which should generate brand “heat”. These changes should significantly expand the brand’s presence in the country, driving future growth.

New wearing occasions

The Sandals industry has a market size of $35B, up from $30B in 2021, over double the size of Clogs. At just 13% of current sales, Sandals represents a large opportunity for the business to expand into and is a natural extension of the already moulded classic clog. Furthermore, with the company experimenting with sneakers, the $110B casual footwear market could soon be targeted as well.

In 2021 at the company’s investor day, management laid out a bold goal to grow Sandals by 4 times in 5 years, if achieved this would have resulted in revenue reaching approximately $1B by 2026. While there are still two years to go, it is unlikely that the business will be able to reach $1B from the $425M at the end of 2024.

This slower-than-expected growth rate is likely due to multiple factors; including supply chain disruptions that delayed product newness and a weaker environment in markets such as India, which has been called out as a large growth driver. However, the biggest factor is probably a distracted management team, which acquired Hey Dude shortly after announcing those goals.

Despite this, the business has still grown faster than both the classic Clog and the broader Sandals market in 2024, demonstrating that consumers value the product. In 2025, the company will introduce newness in the Getaway and Brooklyn lines which performed well in 2024. Continued product newness and a management team that can spend more time on initiatives such as Sandals will likely allow the segment to continue becoming a larger part of sales, driving growth.

Sneakers also represent a large opportunity for the company, while still in the experimentation phase. The released Salehe Juniper sold out quickly, highlighting consumer appetite for the product. This will likely be a longer-term driver for the business.

Hey Dude

The turnaround of the Hey Dude brand could drive significant upside for the company, not only by the shift from detractor to contributor on the financial statements but also through the market allocating a higher market multiple to the stock.

Not a demand issue

The first question to ask is whether consumers still want the product. or was it a fad?

While the financial results have demonstrated a brand that is generating less revenue and therefore selling fewer shoes than a year ago, there is not a demand issue.

The business has been seeing strong underlying sell-out trends and has performed as a top brand for many wholesale partners. Furthermore, the performance in channels such as TikTok shop, where they ranked third best brand in December, demonstrates sustained strong demand for the product. This has been masked by strategic account rationalisation and grey market issues. Underlying demand will become evident over time as the grey market inventory depletes.

Taking the right steps

Over the past year, the company made several significant changes, these are likely the right actions.

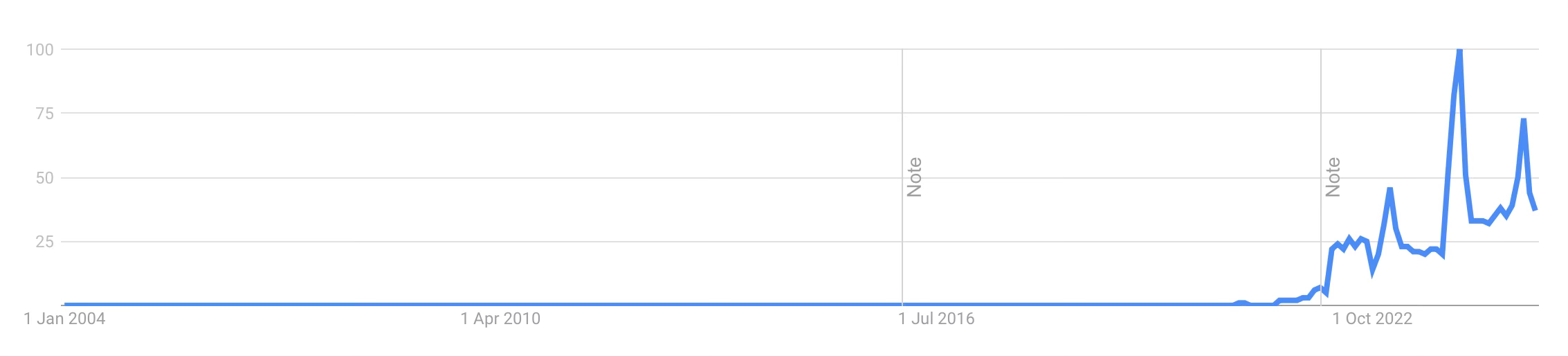

New Management: The first and likely most important change is the new management at Hey Dude. Terence Reilly, the previous Crocs chief marketing officer, has rejoined the company as president of Hey Dude following a stint at Stanley (cup company). During his 4 year stint at Stanley, he is credited for taking a 100-year-old brand and turning it into a social phenomenon, as demonstrated by Google Search trends.

Going on the offensive: Since taking charge, Reilly has made several changes to the strategy:

Focusing on Icons: Similar to Crocs’ turnaround, the company is prioritising the classic silhouettes, Wally and Wend, driving innovation around the core.

Increased investments in marketing: Management has significantly stepped up the marketing investments. In Q3 2024, the brand pulled away from performance marketing, instead focusing on building the brand. The company is now marketing towards the female youth culture, which they believe drives many of the consumer trends today. In doing so, Hey Dude announced Sydney Sweeney as its global brand ambassador, this content has seen the most engagements to date.

Expanding distribution channels: While the company has been rationalising its strategic wholesale accounts, the company has been opening other channels.

Outlet stores: In 2024, the company opened 38 outlet stores, bringing the total to 52. These stores allow Hey Dude to educate consumers about the brand, providing a comprehensive view of the product offering and attracting more consumers to the brand. The performance of these openings has been in line with the company’s expectations

Direct-to-consumer: While the company already has its own E-commerce store, Hey Dude has been leveraging TikTok shop to connect with a new, younger demographic. The company has seen an excellent response; TikTok followers surpassed Instagram followers, and the company was ranked as the number three footwear brand in December.

International: Historically, Hey Dude has had a limited presence beyond North America, other than a small distributor in Italy and Spain. The company is now laying the groundwork for a larger international presence. In 2024, the company expanded into direct markets such as the UK, Germany and Australia, leveraging the existing Crocs teams for E-commerce and Wholesale partnerships. Additionally, the company has signed new distribution agreements which will go live in 2025, such as India.

These actions demonstrate that Reilly is the right person for the job and is taking the appropriate steps to achieve long-term success. He has previous experience working for the company, likely being instrumental in the turnaround during the 2010s, and he has proven that was not a fluke by taking Stanley to the forefront of youth culture in under four years.

Confidence in the turnaround

Investors should take comfort in the fact that this management team has already turned the Crocs brand around, they have a time-tested playbook, focusing on the core and introducing a socially led marketing strategy which is currently unfolding here. While it will take time to improve, the potential upside is large if successful.

The opportunity

If the company manages to turn around the Hey Dude business, the company likely has a large opportunity for growth ahead.

Larger TAM

Hey Dude theoretically has a larger addressable market than Crocs currently. Hey Dude competes in the $110B casual footwear market, while also introducing some sandal options, expanding the TAM further. If the company successfully executes the brand vision, the brand could theoretically be larger than Crocs.

Brand Awareness

North America represents the vast majority of the company’s revenue and penetration. Even in this market, the company only has 32% brand awareness. This means that 70% of consumers have never even heard of Hey Dude. Through innovative marketing campaigns and partnerships, the company has already increased awareness from 18%. Awareness will likely continue increasing as the company sees returns on the increased marketing investments and the rollout of the outlet stores; this, in turn, should drive revenue. In 2024 Crocs generated $1.8B in revenue from North America, reaching this parity would double revenue from current levels.

International expansion

Hey Dude likely has a huge opportunity to expand internationally. Currently, brand awareness is zero outside of North America. By leveraging Crocs distribution relationships, Hey Dude will be able to expand into key Tier-1 markets where the company already has a presence.

I mentioned in Crocs’ international expansion section that the opportunity represented a $6B revenue opportunity, given Hey Dude operates in a much larger TAM, the opportunity could theoretically be even larger. However, it is important not to get ahead of ourselves. That kind of opportunity would be decades away, currently, the brand is only experimenting in International markets, and it will take several years of execution for International revenue to even move the needle, let alone drive total company revenue. A more rational scenario would be for the company to achieve similar contributions from international markets like Crocs. Currently, Crocs generates 44% of revenue internationally, representing a roughly $400m revenue opportunity.

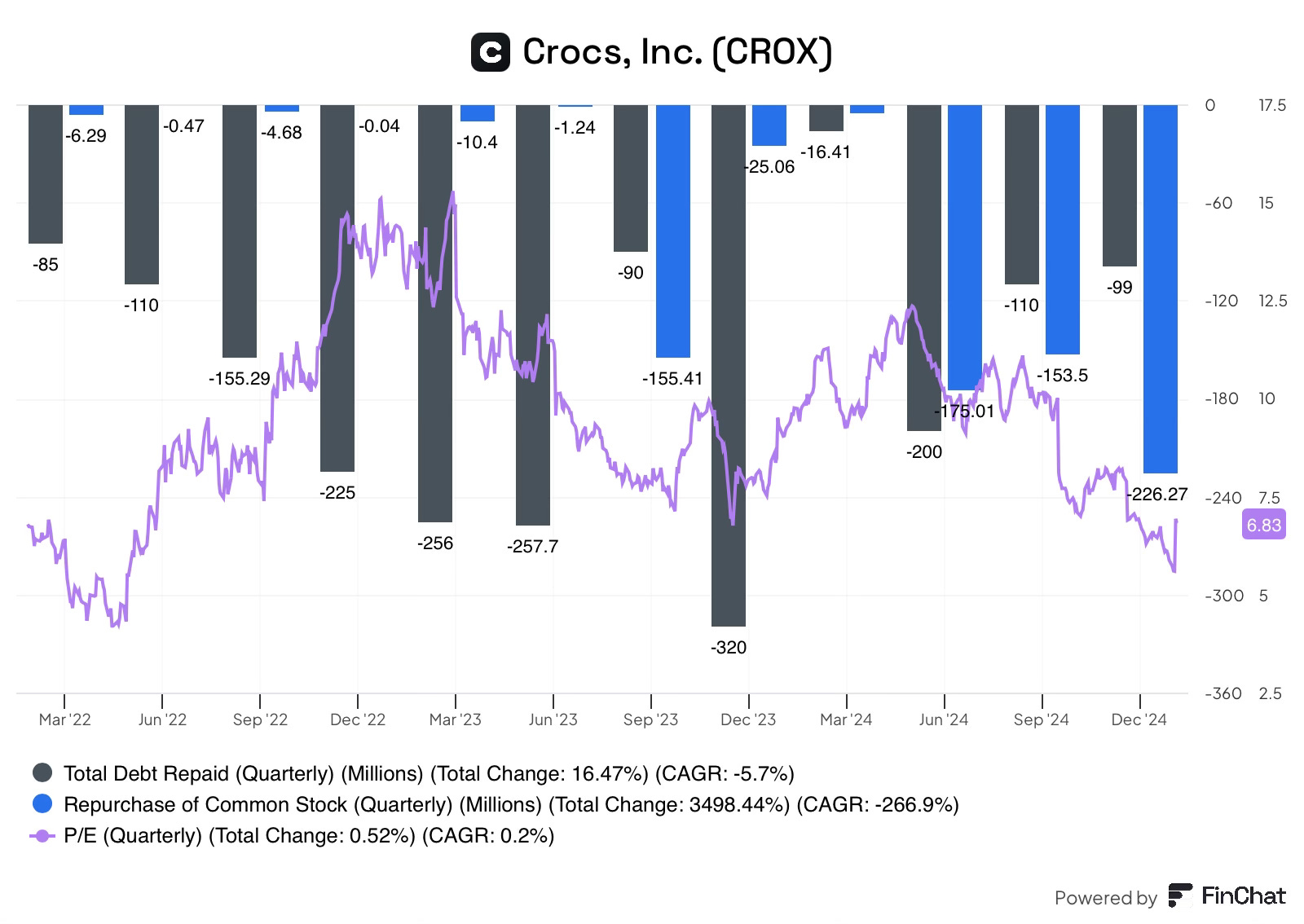

Buybacks

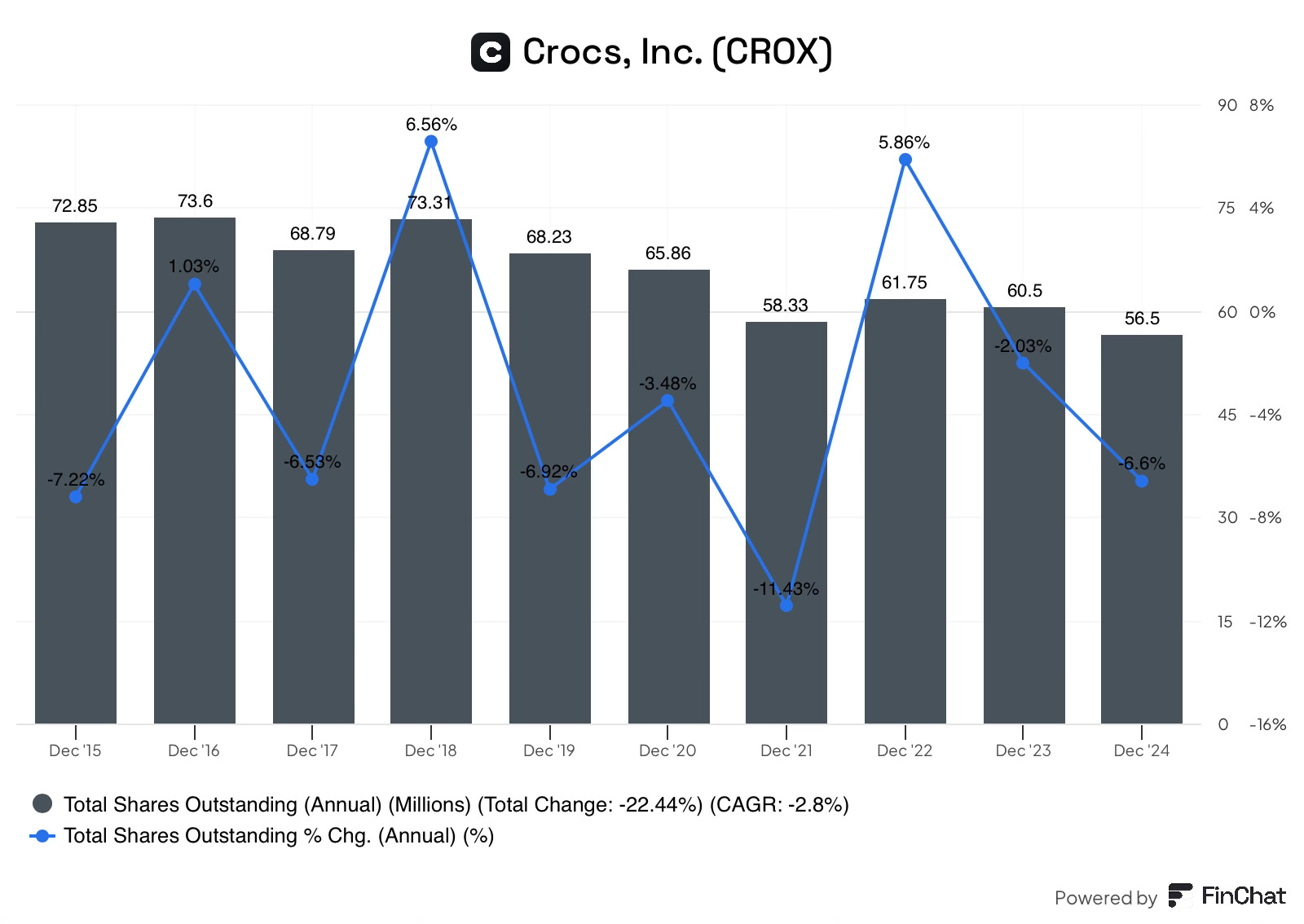

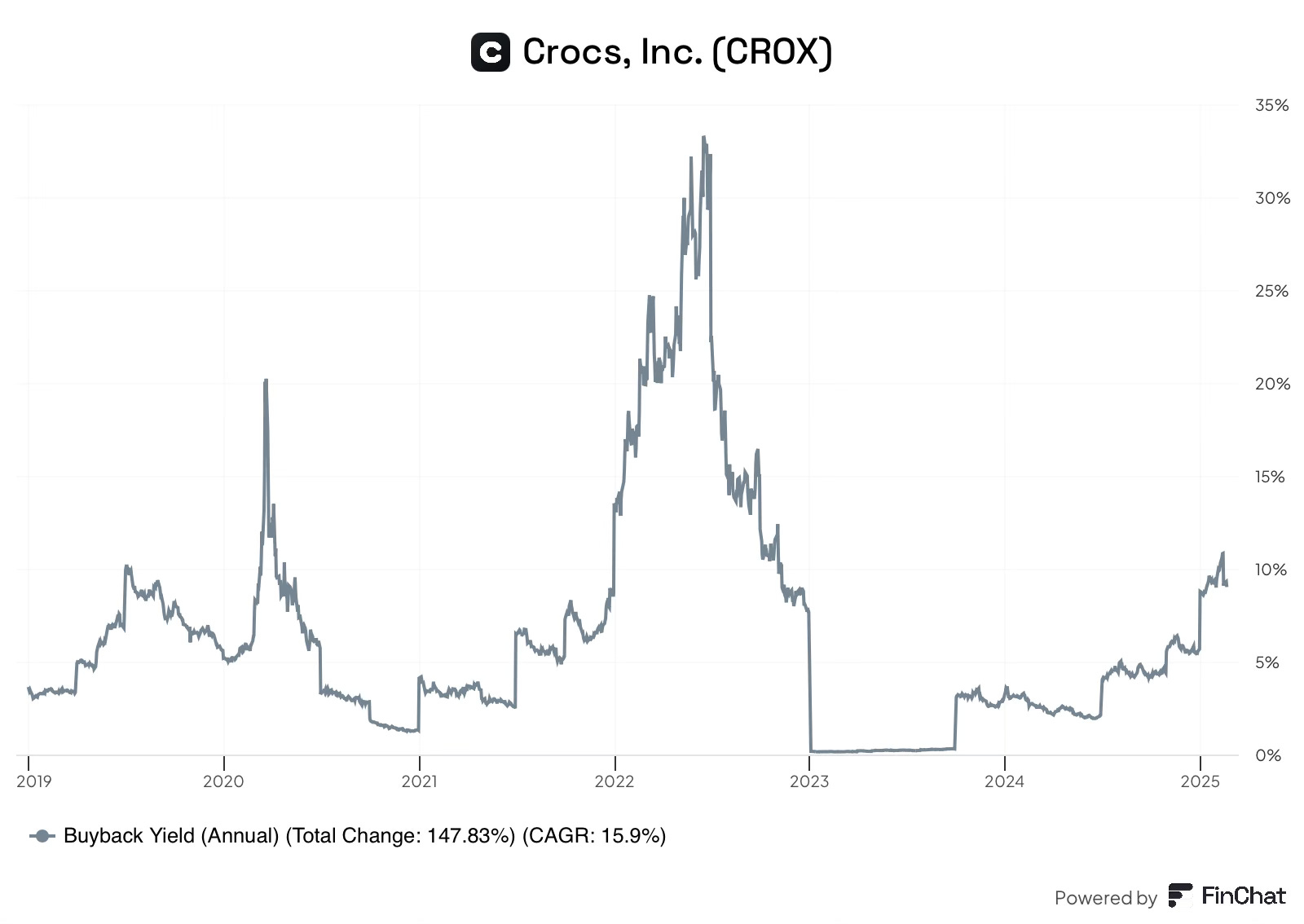

Crocs has the potential to become a share cannibal.

Crocs has a long history of returning cash to shareholders through share repurchases. This has resulted in shares outstanding declining by almost 3% annually. Prior to the Hey Dude acquisition in 2022, shares outstanding actually declined by almost 4% annually.

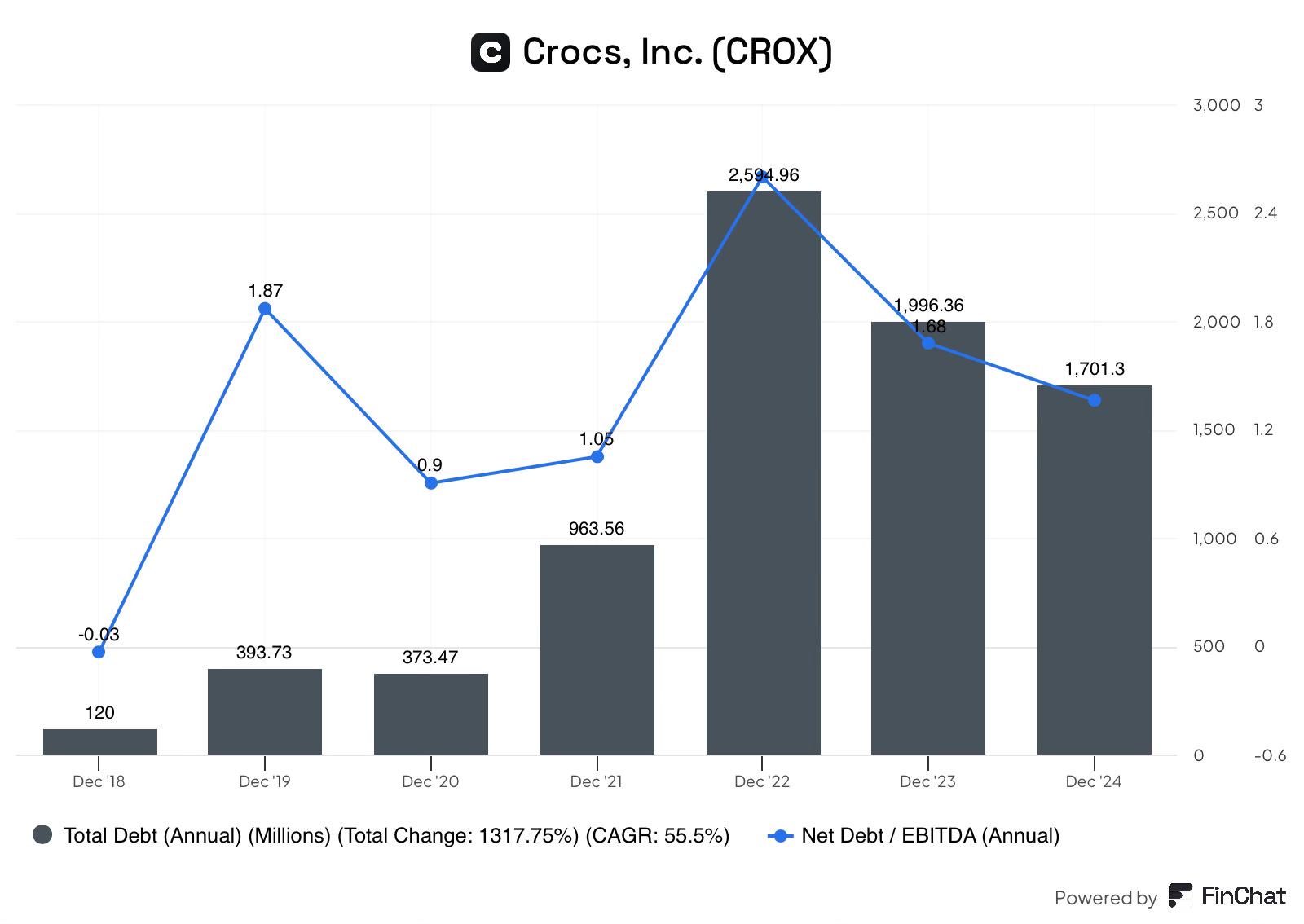

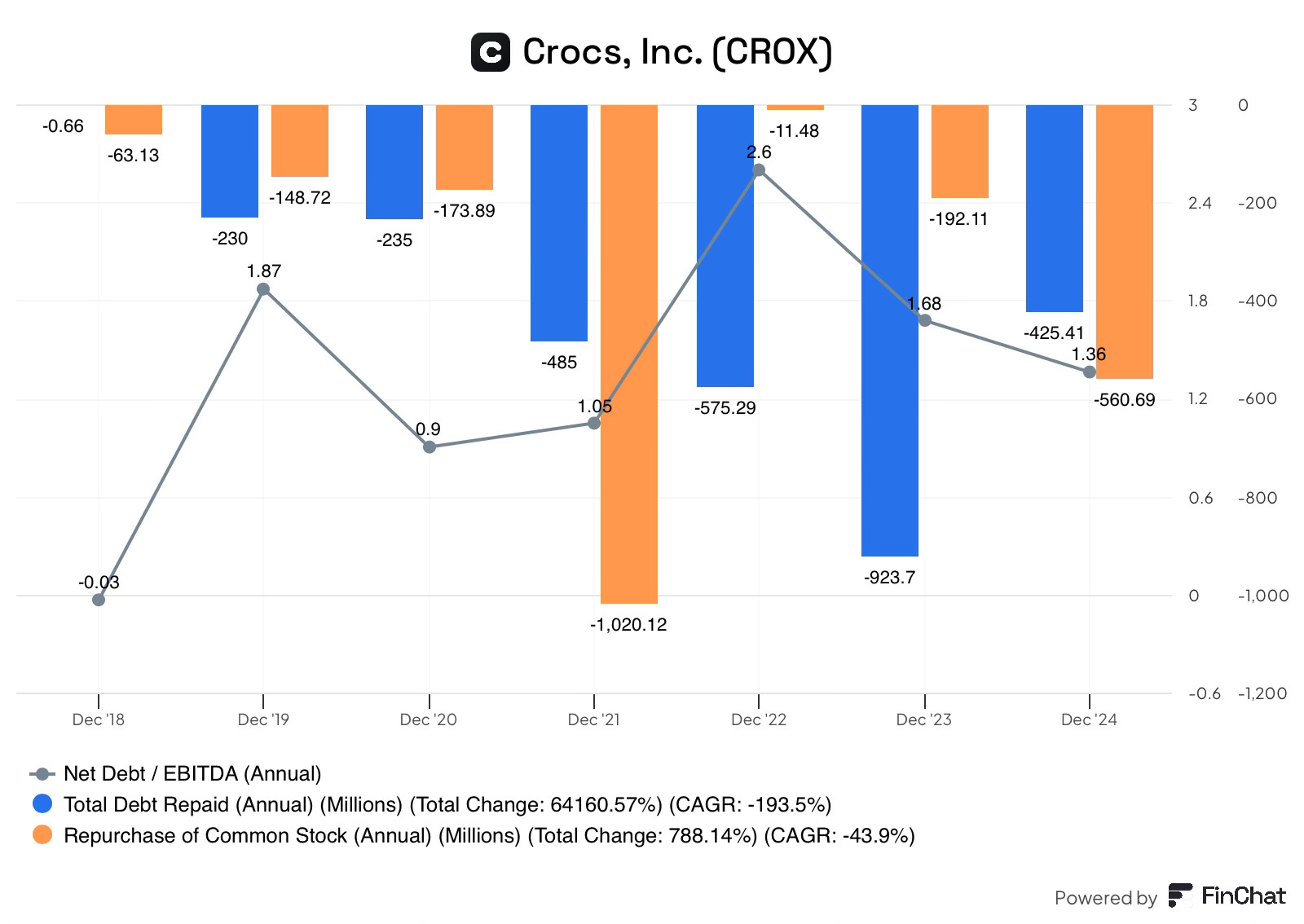

In 2022, Crocs acquired Heydude for $2.5B, as part of the deal 20% ($500m) of the price was paid in stock, resulting in shares increasing by 6%. Additionally, the remaining 80% ($2B) of the purchase price was paid in debt, increasing debt/EBITDA to 2.6X.

To bring down this high leverage ratio, the company focused on paying down debt rather than repurchasing shares. As the company neared the target 1-1.5X leverage ratio, capital began flowing back into share repurchases.

With the current debt levels in line with management’s leverage targets, 100% of free cash flow can be allocated to share repurchases, resuming the company’s historical trend of being a share cannibal.

In Q4 2024, the board of directors authorised a new buyback program, increasing the authorisation to $1.3B, representing almost 22% of total shares. At current levels, management can buy back 9% of shares per year! This kind of allocation would be extremely accretive to shareholders, especially if it is sustained over a long period of time.

Additionally, management seems to understand share repurchases. The company has historically increased share repurchases as valuation has decreased, demonstrating an orientation towards shareholders.

Valuation

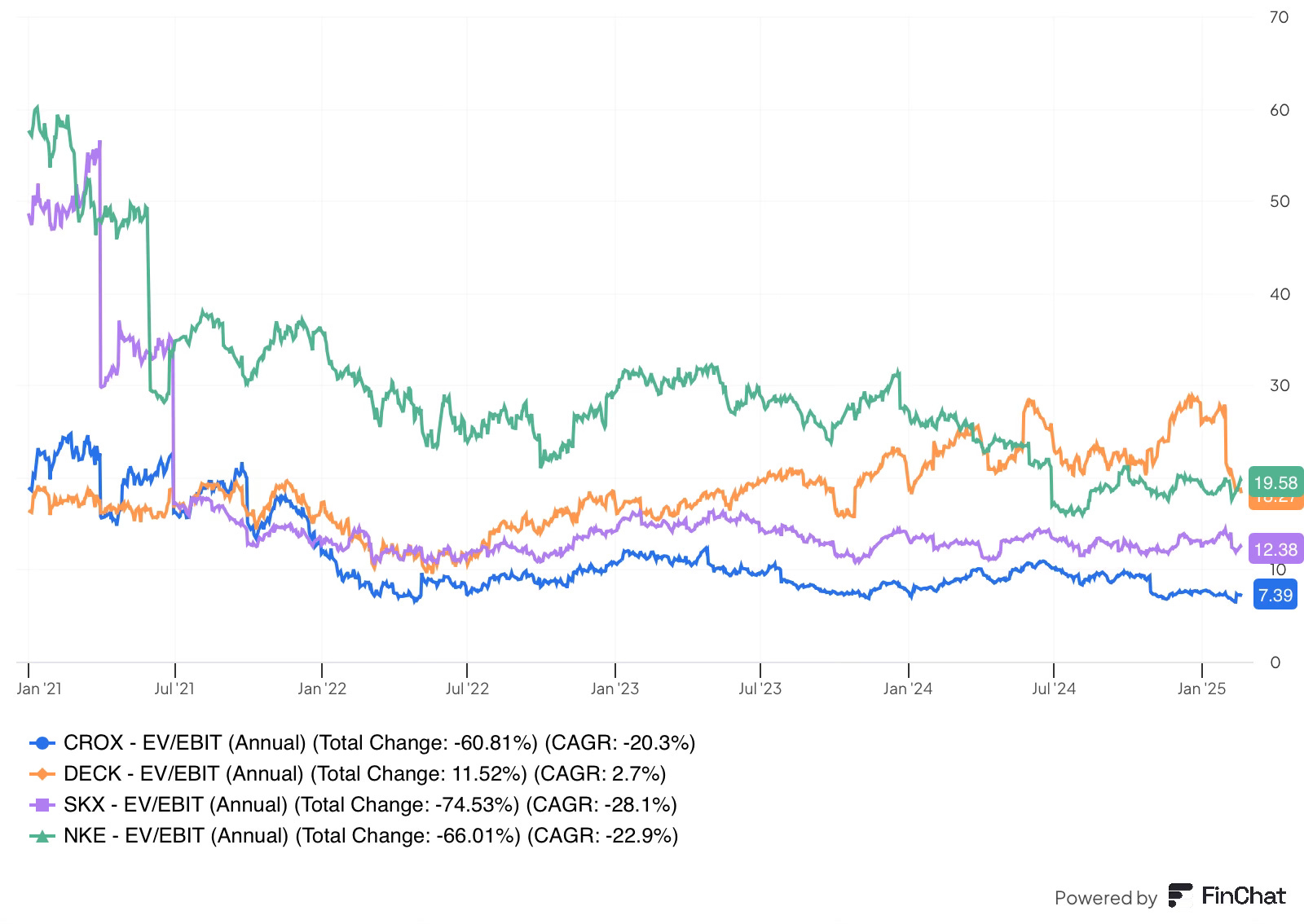

As a long-term value investor, I am looking to buy shares at a margin of safety to intrinsic value, currently Mr. Market values Crocs significantly below peers.

Peer Comparison

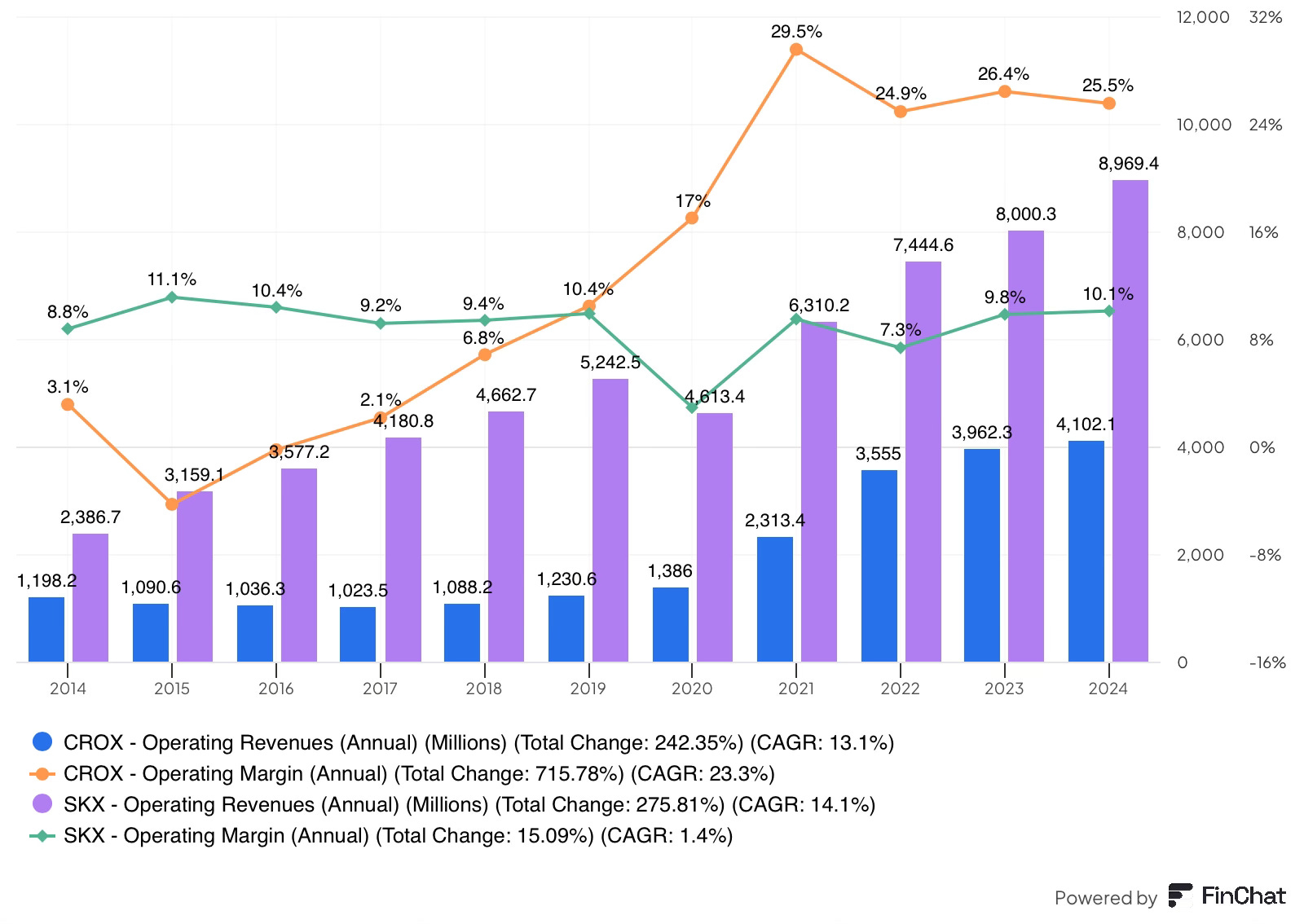

It is clear from the chart that Crocs trades at nearly half of the lowest-valued peer, Sketchers. When comparing the two companies, Crocs has achieved a comparable growth rate over the past decade, yet achieves operating margins of 25% versus Sketchers 10%. I would therefore argue, that Crocs is deserving of a premium valuation over Sketchers.

This relative undervaluation is likely due to investor concerns surrounding the Hey Dude acquisition and the sustainability of Crocs, which I have argued against during this deep dive.

Scenario-based Valuation

Applying several different scenarios to the stock makes it clear that Crocs is likely undervalued today.

In 2024, Crocs generated free cash flow per share of $15.4, I will use this for the below scenarios.

Bear Case: In a downside scenario for the company, FCF grows just 2% per year as low single-digit growth from Crocs is offset by declines from Hey Dude. Share repurchases are modest yet drive the 2% FCF/share growth. The P/FCF of 8X has increased slightly. After 5 years the company would generate FCF of $17 per share and be worth $136.

This represents a 5% CAGR from current levels.

Neutral case: In a conservative scenario for the company, FCF grows 7%, driven by the robustness of Crocs North America and contribution from International expansion. Hey Dude stems the declines but contributes minimally to FCF. Management leans into share repurchases, contributing 3% of accretive growth.

The P/FCF slightly re-rates to 10X, still below peers. After 5 years the company would generate $21.6 in FCF and shares would trade at $216.

This scenario would generate a 15% CAGR.

Bull Case: In a positive scenario for the company, FCF grows 10%, driven by healthy growth in Crocs, International expansion remains in the double digits, and new wearing occasions drive strength in Sandals. Hey Dude, sees positive growth as brand awareness improves and international expansion goes well. Share repurchases are utilised aggressively and opportunistically, contributing 3-4% of accretive growth. The P/FCF re-rates to 12X, in line with Sketchers. After 5 years, the company would generate $24.8 in FCF, and shares would trade at $298.

This positive scenario would generate a 23% CAGR over 5 years.

It is clear from this valuation exercise that even modest growth and a slight re-rating would generate asymmetric returns that would likely outperform the market based on historical returns.

Risks

Hey Dude

The biggest risk associated with the company remains the turnaround of Hey Dude. I have made my case in this report as to why the company has taken the right actions to turn the business around. However, only time will tell.

Fashion trends

With the rise of fast fashion, changing consumer trends is always a big risk for any fashion brand, Crocs is no different. However, the company’s moulded technology process and innovative marketing strategies allow the business to bring newness to market very quickly. In fact, Crocs has been focusing on speed to market, in 2024, they increased speed to market by 60%.

Furthermore, the company has been expanding their product offerings, allowing the business to cater for more styles and wearing occasions.

Knockoffs

Knockoffs are a big issue for the brand, it is very easy to produce a similar-looking clog and undercut the company on price. On closer inspection these shoes do not have the same kind of materials, giving them a cheaper, less durable feel.

To counteract knockoffs the company first has a global intellectual property portfolio that should protect the company from being copied. However, where this is ignored the company takes proactive action (including legal) against anyone within their network who may be facilitating, producing and selling any counterfeits. The biggest risk for these goods is in Asia.

Beyond legal action, there are two defences the company is taking to protect themselves:

marketing, by creating brand heat the company is creating a brand that consumers are willing to pay up for, rather than settling for fakes.

Product innovation, by introducing new designs and materials such as the new LiteRide material technology, knockoffs have to continually invest to keep up, making it more difficult.

While knockoffs will always exist for a product like this, these actions should allow the company to continue expanding in regions such as Asia.

Conclusion

Crocs is a compelling opportunity at current levels, the business has a strong competitive position that allows the business to generate best-in-class financials, management has a strong track record and the business has the opportunity for sustained growth on the top and bottom line.

Additionally, the stock is available at just 6.5X FCF, representing an asymmetric opportunity.

Crocs currently represents 1% of the portfolio, however I am considering taking advantage of any share price weakness.

Sources: Company filings

Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment decisions.

Nice article! Big fan of the CROX stock at this levels. I suppose you have used the multiple approach for terminal values in your valuation estimates?

Great write-up. Used to be long, now short as the alt-data has turned negative. Andrew Rees is a great CEO however.