May portfolio update

Welcome to the May portfolio update!

Substack update

On June 1st, I published the first part of my deep dive into Xpel ($XPEL). This lengthy report marks a conscious shift from more frequent monthly articles to less frequent, more in-depth reports that better align with my investing style. The link to this deep dive can be found below.

My investing style revolves around holding superior (ideally founder-led) businesses for the long term. Beyond my recent sale of Thor Industries THO 0.00%↑, it has been multiple years since my last meaningful sale, leading to an extremely low turnover (I haven’t calculated turnover, but I would expect this to be in the region of 5-10%).

This low turnover means that new names enter the portfolio rarely, typically 1-2 names per year. These new businesses must pass a high bar to enter the portfolio, which requires me to understand each business intimately, hence the shift toward more in-depth reports.

I hope to finish the second part of my Xpel deep dive in June. Stay tuned!

If you haven’t read any of my previous deep dives, please check out my profile or follow the links below:

Cumulative performance

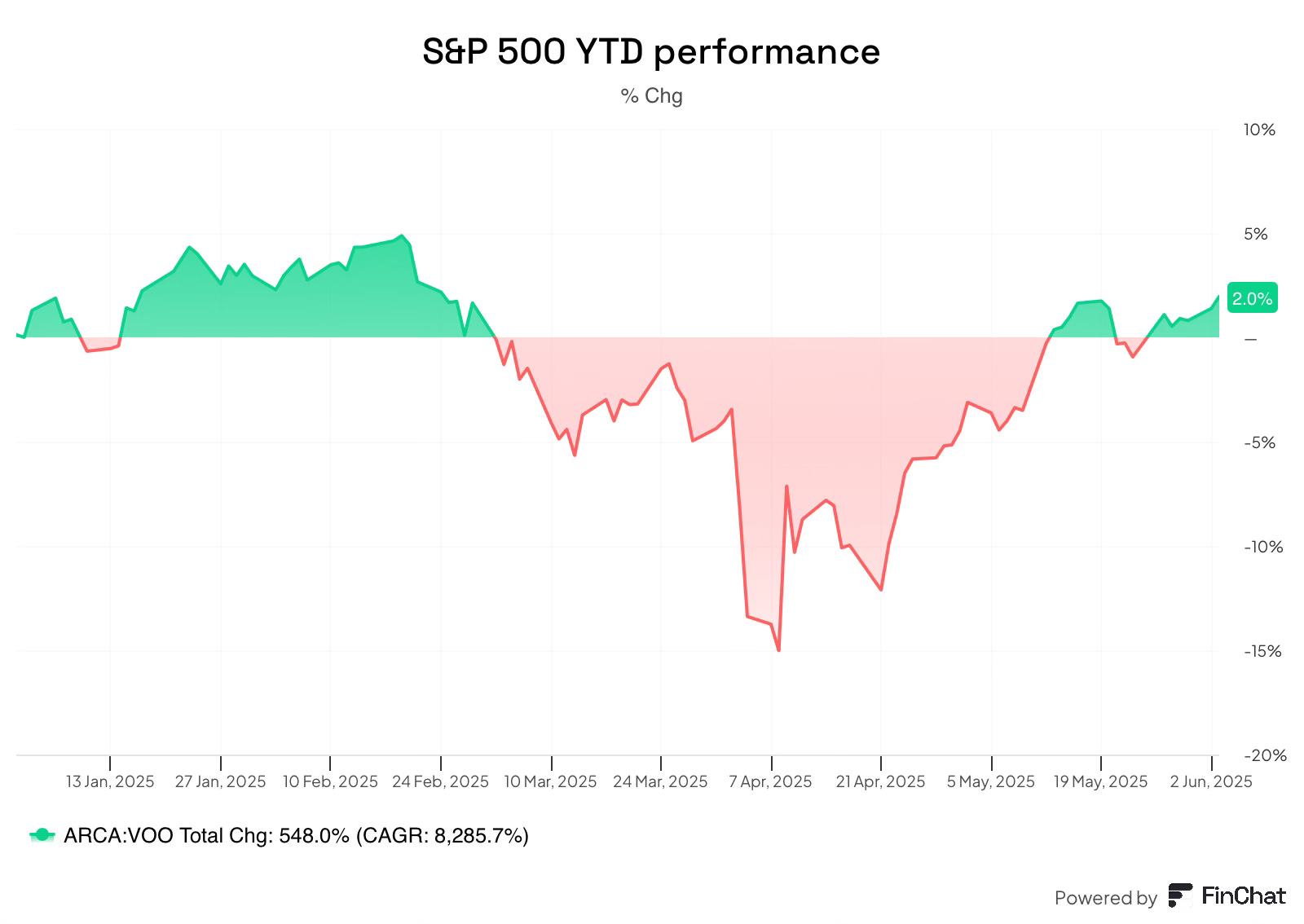

My investment record goes back to the 4th of November 2020. Since inception, I am currently ahead of the S&P 500, my benchmark:

My portfolio: +70.5% (12.3% annualised rate of return)

(Note: returns are tracked across 3 brokerage accounts; calculations to combine these into one figure may contain mistakes.)

S&P 500: +73.4% (12.8% annualised rate of return)

This is the first month since starting my substack that total returns have fallen below the cumulative returns of the S&P 500. As I noted consistently while being ahead, I will repeat it now that I am behind. A longer period, likely decades, is required to determine whether I will outperform the index.

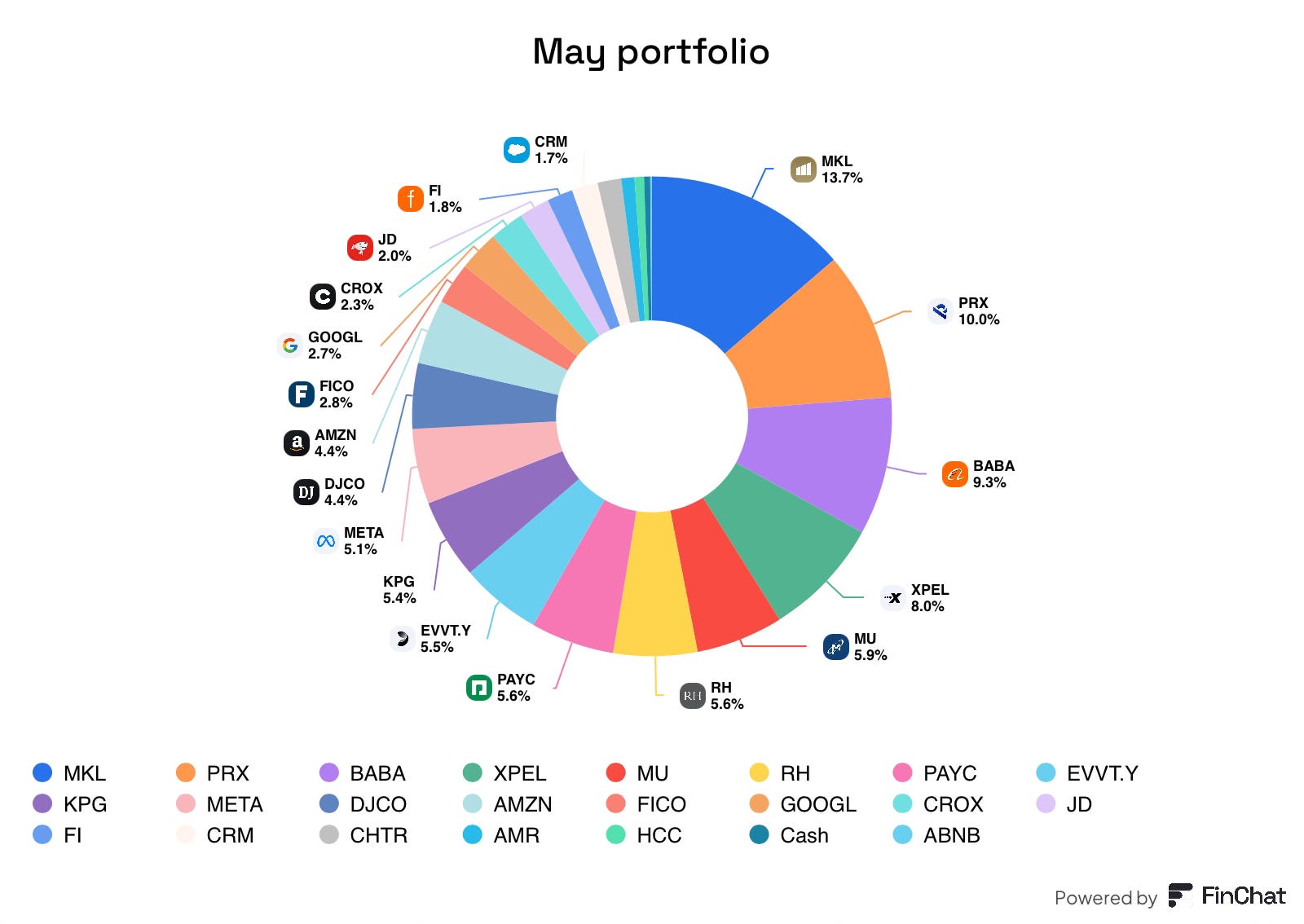

Portfolio

In May, the portfolio increased by just under 5%, slightly behind the gains of the broader S&P 500. Similar to the S&P 500, the portfolio as a whole rebounded strongly.

Unlike the S&P 500, the portfolio gave back roughly 8% in the second half of May.

Part of those losses were due to FX headwinds, and the remaining amount was due to isolated stocks underperforming; these included:

Alibaba

Kelly Partners Group (KPG)

FICO

Fiserv

Concerning Alibaba and KPG, there was no company-specific news to report. Alibaba reported strong earnings, but the stock continues to be influenced by the tariff noise surrounding Chinese-listed names.

For FICO and Fiserv, I will delve deeper into these below:

FICO

A noticeable detractor in the quarter was FICO, which dropped 32% in a matter of days, before recovering partially (still down 22%). The reason for this drop was comments made by Bill Pulte, director of the Federal Housing FHFA.

Pulte aimed FICO’s pricing actions amid concerns of rising costs of ownership. These concerns are both hardly surprising and misguided at the same time.

Over the past several years, FICO has increased the cost of a mortgage score by as much as 500%, a dramatic increase. This has undoubtedly grabbed headlines. However, closing costs for a house typically range from 2-5% of the purchase price. To put this into perspective, a trip-merge report will result in FICO receiving $14.85 in total! So, despite these price increases, FICO still represents a tiny fraction (0.2%) of the total costs to buy a house, meaning any concerns regarding rising costs are not because of FICO.

Despite this fact, investor fears are understandable. Has FICO raised prices too quickly? Is Icarus flying too close to the sun? In short, nobody knows, my gut would say FICO’s long-term pricing power remains intact, but maybe a few slower years may be in order!

Fiserv

Fiserv was another portfolio holding that performed poorly in May, dropping almost 20% following comments made by Rob Hau, CFO, regarding slower-than-expected growth at Clover.

In Q1 2025, Clover, a meaningful part of Fiserv’s business and one of the key pillars for future growth, reported softer-than-expected volume growth of 8%, down from 14% in the previous quarter. While disappointing, this slowdown is in line with peers. Additionally, the company had several factors that inflated the prior year’s figure; adjusting for these, volume growth was closer to a 10-12% growth rate.

When analysing Clover, volume growth is only one part of the story, the product is becoming the operating system for the small business. Including value-added services (software) and hardware sales, Clover achieved 27% growth, a healthy figure that keeps Clover on track to achieve $3.5B in sales for the full year, which would account for 15-20% of Fiserv’s total sales.

Xpel

On the positive side, Xpel, following several quarters of negative reactions to earnings reports, Q1 was a positive surprise, rising by 20% on the day!

In Q1, revenue accelerated from +1.9% in Q4 to +15.2%. This growth was boosted by strong performance in both the US and China.

In the US, growth accelerated from 6.2% to 11.6%, potentially due to some pull forward in buying habits due to looming tariffs, along with strong growth of the window film segment, likely due to the new windshield protection film product.

In China, Xpel’s on-the-ground team seems to be making inroads into the sell-in/sell-through dynamic that is unique to China. This should lead to results more accurately reflecting the underlying demand.

The company’s cost-cutting efforts have also begun to bear fruit, with margins expanding for the first time since June 2023.

These results, coupled with a P/E ratio of just 15X, resulted in a strong rebound.

Transactions

Following a heavy buying spree at the start of April, I have made no transactions in May, I remain fully invested with no capital inflows into the portfolio.

In June & July, I expect to receive several sizeable dividends from Evolution and Alibaba (regular + special dividend). Currently, I view Evolution as the most likely source of any new funds, however, this can change between now and receiving these dividends.

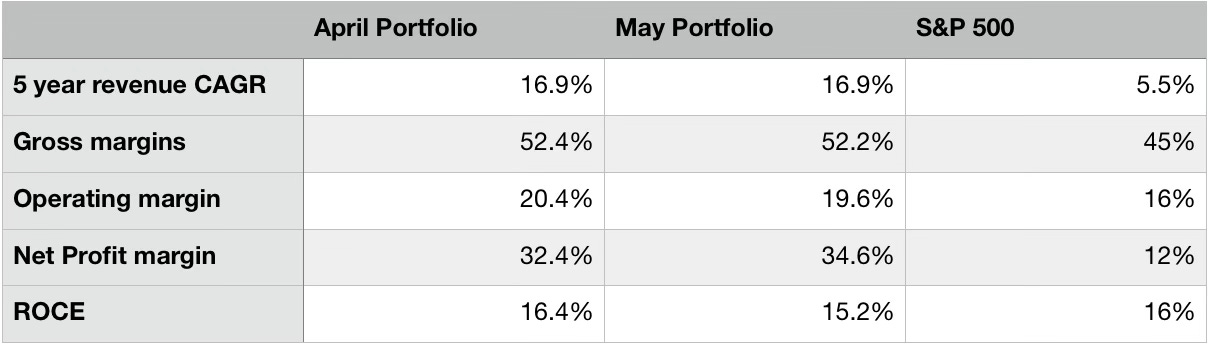

Portfolio positioning

In May, the portfolio characteristics as a whole got slightly worse but remained superior to those of the S&P 500.

Since I made no transactions, these changes must be down to stock movements affecting portfolio weightings and earnings reports. I remain convinced that the portfolio as a whole is under-reporting margins and ROCE, as investments continue to be made that should increase the long-term value of my holdings.

Thank you for reading!

Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment decisions.