Evolution Q4 & full year review

Analysis of Evolution's fourth-quarter earnings.

Welcome to my first company update on this channel. In this article, I will dive into Evolution’s latest quarterly report. While I typically will not update on a quarter-by-quarter basis, the company’s strong growth & low valuation make it an attractive opportunity to invest.

To understand more about the business, check out my three-part deep dive into the company.

Evolution reported Q4 earnings on Thursday. Despite solid results, shares fell 7% due to poor margin guidance for 2025. This weak share price movement followed continual price declines throughout Q4, providing a potential opportunity for long-term investors to buy.

While the financial performance remains robust, the company is working through several operational challenges, including Cyberattacks in Asia, reduced capacity from the fallout in Georgia, changing regulatory landscapes, turning around the RNG segment and higher taxes.

Strategy

Evolution continues to invest heavily in Gaming innovation and Capacity expansion to capture the large opportunity ahead.

Game Innovation: continues to extend the gap

In Q4, I found several comments about the company’s game strategy particularly interesting.

The company is continuing its “product leap years” by releasing the strongest slate of games to date in 2025, while also benefitting from the continued growth of 2024 releases (such as Lightning Storm) and continued strength from evergreen games like Crazy Time.

Evolution intends to release 110 games in 2025, in line with the release cadence from recent years. Unlike previous years, Evolution plans to launch the majority of these games in the first half of 2025, resulting in a considerable number of games entering Evolution’s portfolio from 2H 2024 through 1H 2025. This potentially signals an even higher game release cadence for 2026.

Notable releases include:

Casino War: Evolution’s take on the classic land-based game, Casino War.

Fireball Roulette: A mix of the classic game of Roulette coupled with the fireball bonus round from the popular game show, Lightning Storm.

Marble Race: A live racing game, taking bets on which marble will reach the end of the downhill track first.

Race Track: An RNG classic horse racing game.

Blackjack extensions: Evolution plans to launch twists on its Blackjack portfolio.

Along with these game developments, Big Time Gaming, NetEnt, Red Tiger & NoLimit City all plan to launch innovative games in 2025. This strong game pipeline, coupled with recent game successes from NetEnt, NoLimit City and Big Time Gaming, suggests that Evolution is close to turning around the RNG businesses.

While quality is at the heart of every game, Evolution is taking several new approaches to game development. Firstly, the company is focused on improving the entertainment factor of its games, by making them “short and snappy”. This approach is inspired by TikTok, with the hope it can provide entertainment not only for players but also for people watching, allowing the games to attract more players.

Secondly, Evolution is focused on providing market-specific games, most notably for the US, Red Tiger is also directing several of their new games to these markets. This focus is aimed at turning around the North American RNG segment, which, despite improvements, continues to underperform, ceding market share. This strategy is smart, Evolution has found success in the past when they have provided regional adaptations, examples include Bacarrat Red Envelope, Super Andar Bahar and Lightning Dragon Tiger. It is likely the best strategy to turn around the trailing US RNG business, only time will tell!

The final insight regarding games is Evolution’s commitment to maintaining its game advantage. In Q4, the company claimed its 3D animation capabilities were just behind Pixar. With this kind of capability coupled with competition that reportedly isn’t as focused on innovation, Evolution will likely continue to extend its gaming advantage. Furthermore, Evolution announced they are enhancing their focus on protecting patents and IP. Historically, competitors have let Evolution innovate before copying their games; this enhanced focus may allow the company to further differentiate itself from competitors, extending the company’s advantage even more!

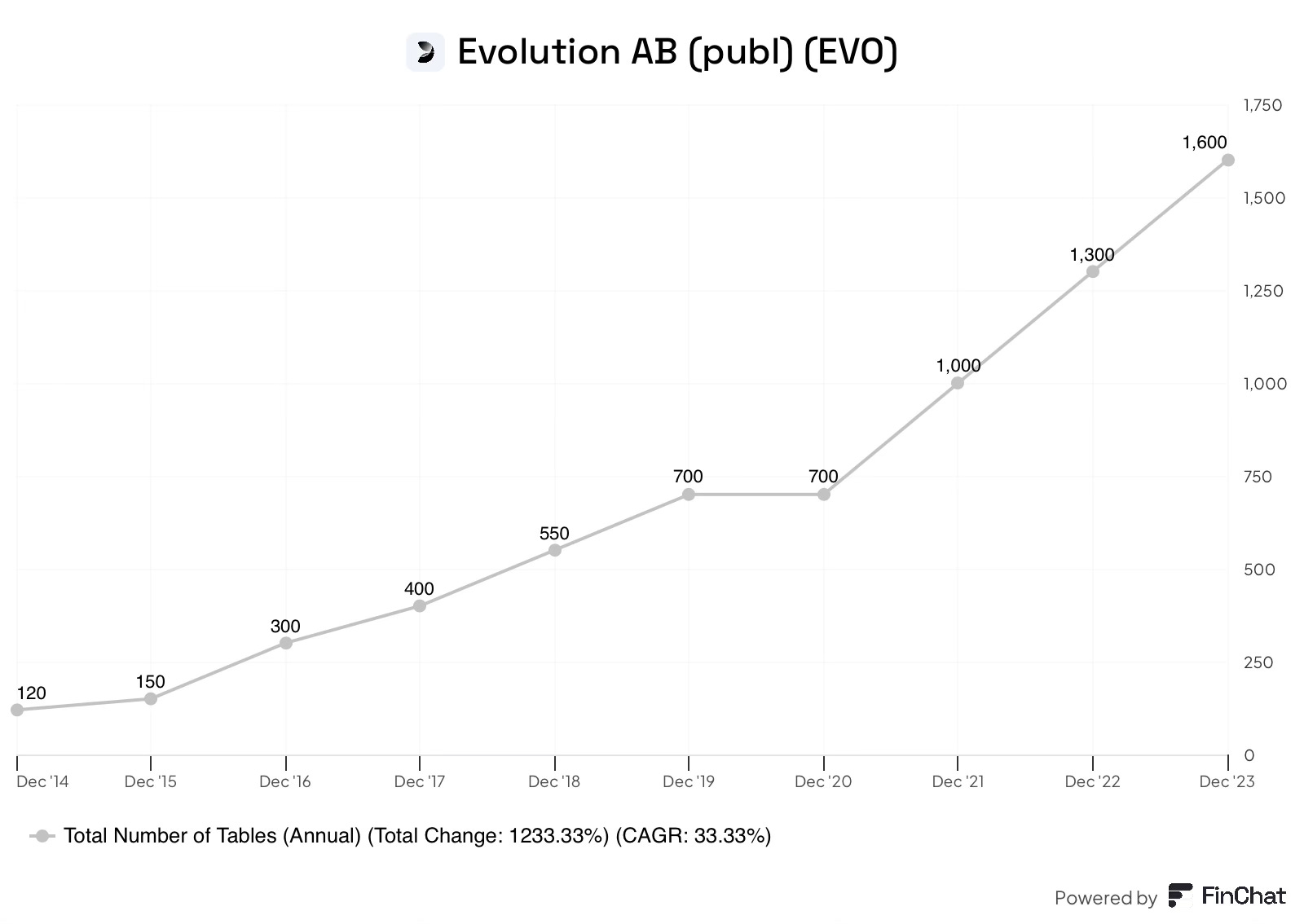

Capacity: Slow growth

For the full year 2024, Evolution had over 1,700 tables, a 6% increase from the 1,600 tables at the end of 2023. This capacity increase is significantly below the historical growth rate due to the capacity reduction in Georgia as a result of the union violence in the summer of 2024. During the year, the company added 300 tables. However, Georgia's downsizing resulted in a decrease of 200 tables, resulting in a net addition of 100. This slower-than-anticipated growth during the year resulted in a slight decline in activity during Q3, subsequently recovering slightly in Q4.

The situation in Georgia is reportedly stable. However, Evolution remains committed to keeping capacity at just 60%, likely constraining capacity in the short term until new studios open.

In 2025, Evolution plans to open 3 or 4 new studios to cater for the strong demand the company continues to experience, studios in Brazil and the Phillippines are both set to open during the year, while the other two locations have not been disclosed yet.

In addition to new studio openings, the company is optimising current studios in two ways:

Expanding capacity at existing locations, most notably in Colombia, to cater for Spanish-speaking demand.

Reshuffling operations to enhance the efficiency of the existing footprint.

Business Trends

In this section, I will discuss the different events that I believe are worth noting from Q4.

Cyber Attacks

Evolution continues to grapple with the Asian cyber attacks that began in Q3. These attacks have caused growth in Asia to decelerate substantially. In Q4, the region grew by 11.3% but remained flat sequentially. Margins are also affected due to the slower growth and additional costs.

The company elaborated more on the nature of the attacks in Q4, stating that its streams are being stolen, similar to someone downloading a movie from Pirate Bay instead of watching on Netflix.

The company has deployed several countermeasures that will make it more difficult to exploit the systems in the future. These measures have been implemented across the entire network, hopefully protecting it from future attacks globally. The impacts will take several quarters to work through, likely meaning Asia growth will continue to slow in the near term. The good news is underlying demand trends remain strong, positioning the company well for future growth once the company works through these issues.

Regulation

There were several interesting updates surrounding regulation this quarter, good and bad.

Incremental European restrictions

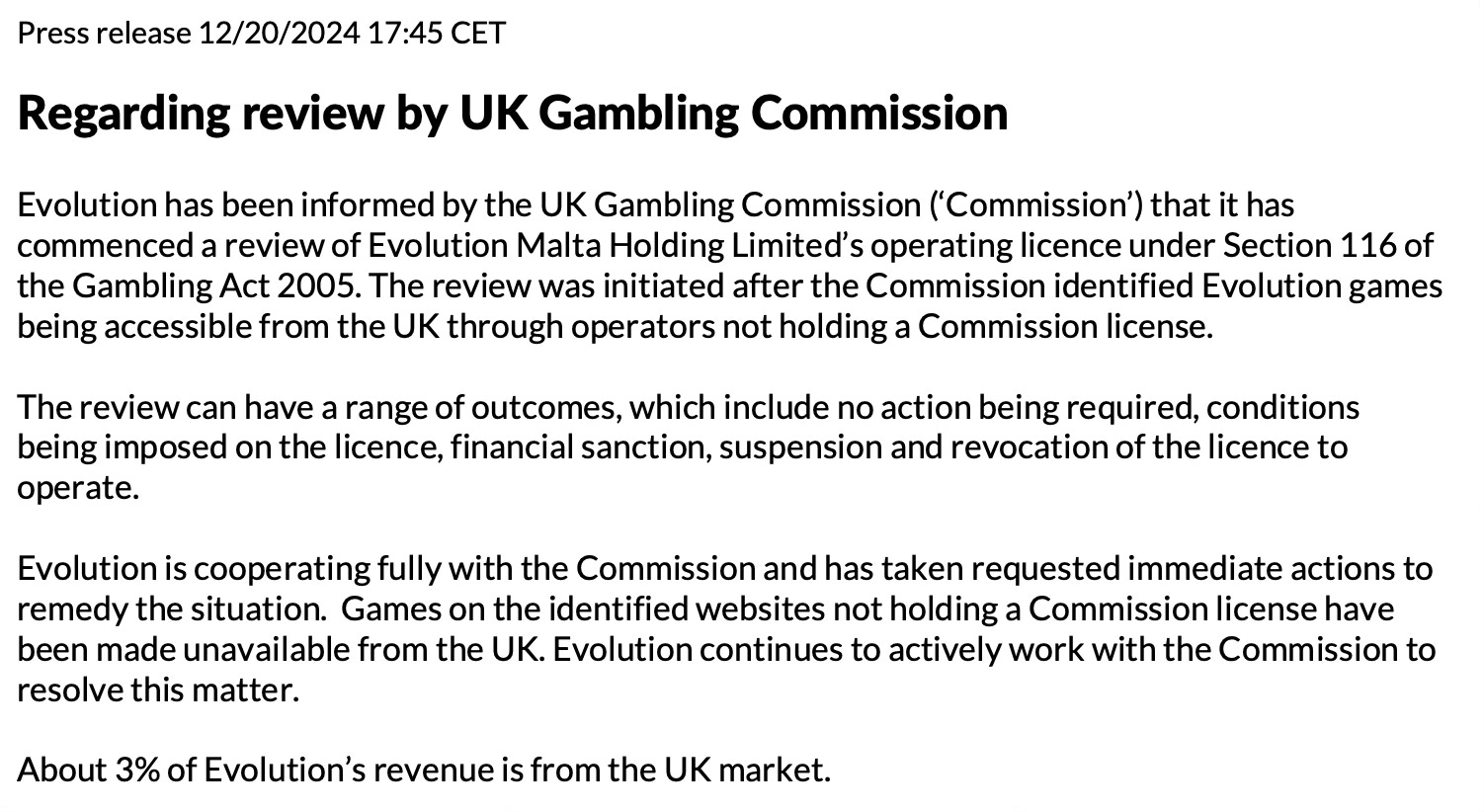

Starting with the bad, following a press release on the 20th of December regarding a UK Gambling Commission review into Evolution, the company reported on the Q4 earnings call that they were implementing measures to ring-fence regulated markets, predominantly in Europe.

The ring-fencing measures are designed to make Evolution’s games only available through licensed operators by restricting internet access to certain markets. The company is working to implement this in all regulated markets over time and comply with regulators everywhere. This is likely a good sign that the company will hold onto its licences in the UK.

The company claimed that the effects of these measures are “quite limited,” but they will likely be a slight drag on revenue growth in the near term. I believe if they implemented these measures across all geographies it could cause a greater impact than expected, resulting in another couple of percentage points of slowdown in the near term. I believe this is a small price to pay for ensuring the longevity of the company in these regulated markets.

New market: Brazil

On the positive side, Brazil introduced national legislation for online casinos, opening the market on the 1st of January 2025. Evolution reported that the initial weeks have been “a bit slow”, however, despite the slow start Brazil is set to be a large market for the LATAM segment with momentum expected to grow in the second half of this year.

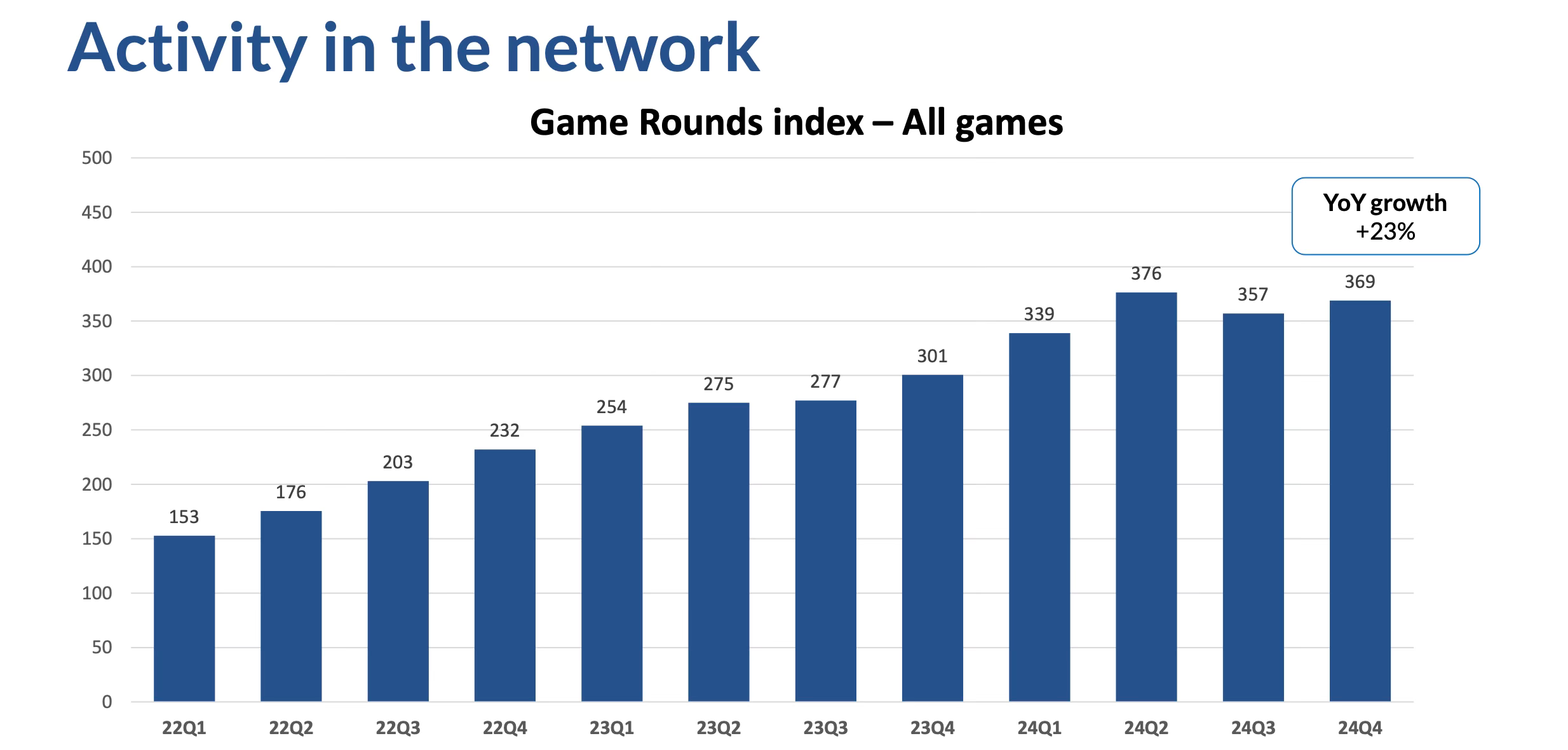

Live table index outgrows revenue

The game round index, an indicator of demand, continues to grow healthily, up 23% from the year-ago period. This growth is healthy despite the issues faced in Asia and Georgia, which continue to impact it. The index continues to grow faster than revenue growth suggesting a combination of factors such as new players and smaller bet sizes are creating headwinds to monetisation.

Insider purchases

While insiders may sell for any manner of reasons, the decision to buy is made for only one reason, they believe shares are undervalued.

Following the Q4 earnings announcement, several insiders purchased shares on the open market, demonstrating the continued belief they have in the business.

While insiders already have significant ownership of the business, these continued purchases should provide comfort to shareholders.

CFO departure & subsequent Swedish regulator investigation

In a recent news article, it was revealed that Swedish regulators were investigating Evolution for delaying the press release of the news that the UK Gambling Commission was reviewing the company.

Jacob Kaplan, CFO, is reportedly responsible for this. Furthermore, it was recently announced Joakim Andersson would replace him as CFO. While this may be a coincidence, it is also plausible they are linked.

Financial Performance

Headline numbers: Don’t tell the full story

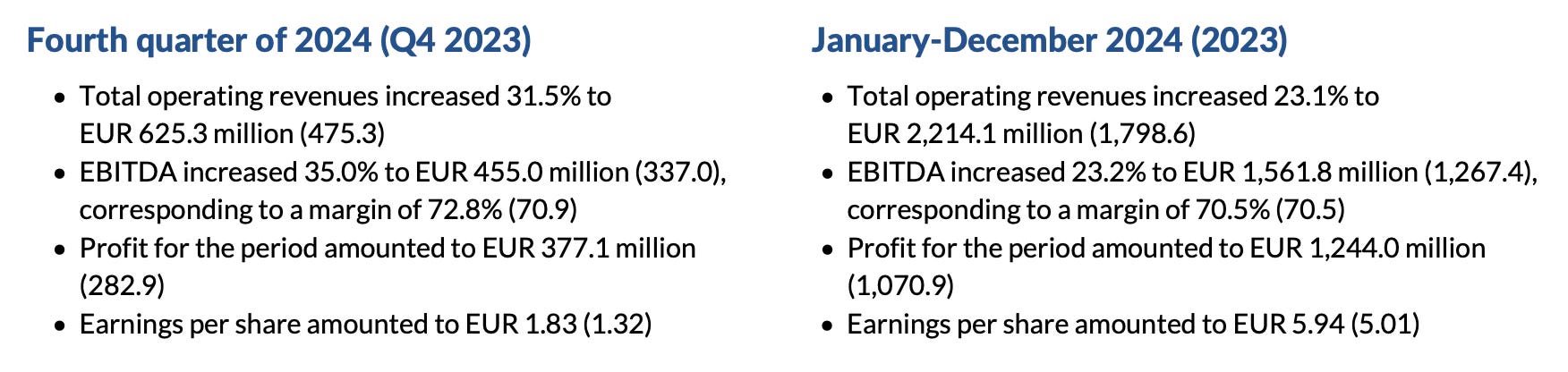

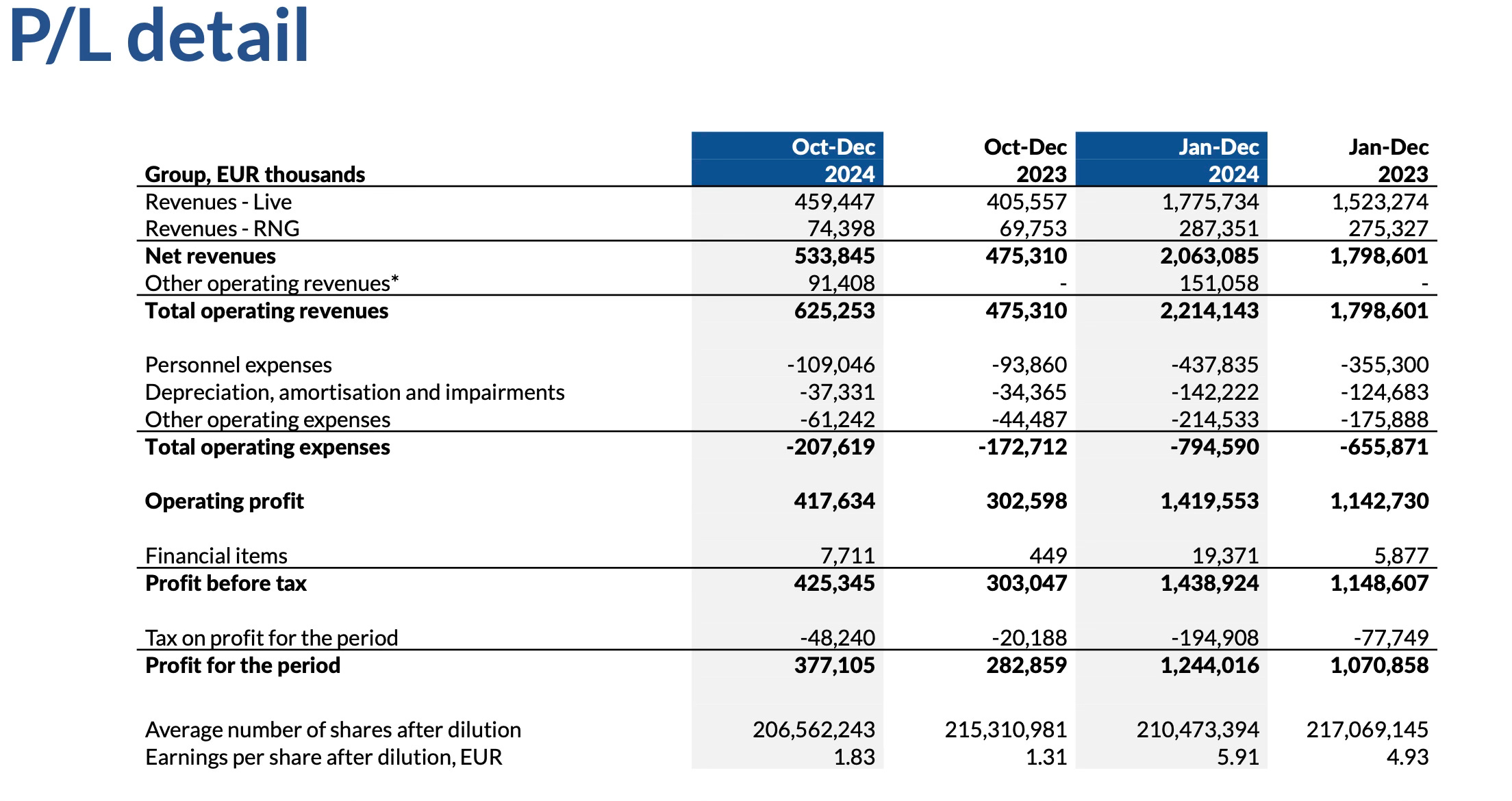

On the surface, the headline numbers look very strong, with operating revenue increasing by 31.5% and EBITDA growing by 35%. However, this growth was driven by an increase of €91.4m in other operating revenue associated with the reduction in earn-out liability from the acquisitions of Big Time Gaming and NoLimit City.

While this reduction in earn-out liability results in higher revenue and earnings for shareholders, I would have preferred the two acquired companies to have performed well enough to reach the targets.

In the rest of the report, I exclude this one-time benefit to understand the true business dynamics.

Revenue

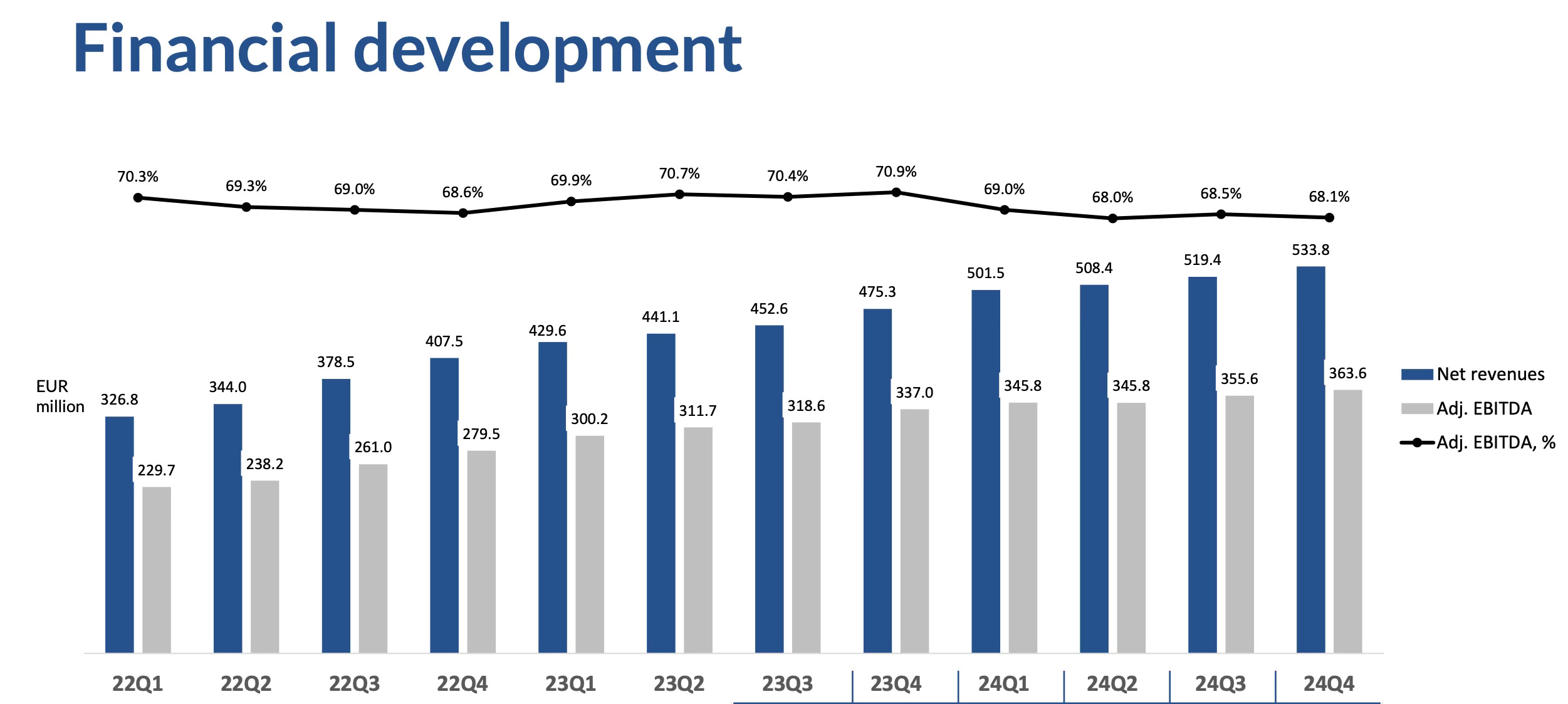

Evolution reported net revenue of €533.8m, a growth of 12.3% over last year.

FX continues to be a headwind for the company, impacting revenue growth by four percentage points in the quarter. Excluding FX, the business would have grown by 16%.

Continuing the trend from Q3, the cyber attacks in Asia (Evolution’s largest segment) were also a significant headwind to growth.

While both FX and Asia remain headwinds to growth, I view these as temporary. Despite these headwinds, it is clear that demand remains strong for the company’s products.

Segment performance:

Live revenue: (86% of revenue) grew by 13.3%, continuing the trend of slowing growth. The continued slowdown in this segment is likely due to capacity constraints and cyber attacks in Asia.

RNG revenue: (14% of revenue) increased by 6.7%, a slight slowdown from last quarter due to a tougher comparison from a year ago. However, this sustained improvement in the RNG business is an encouraging sign that it has potentially turned a corner.

Going forward, the continued tougher comparisons coming up will serve as a further test for the segment.

Geography

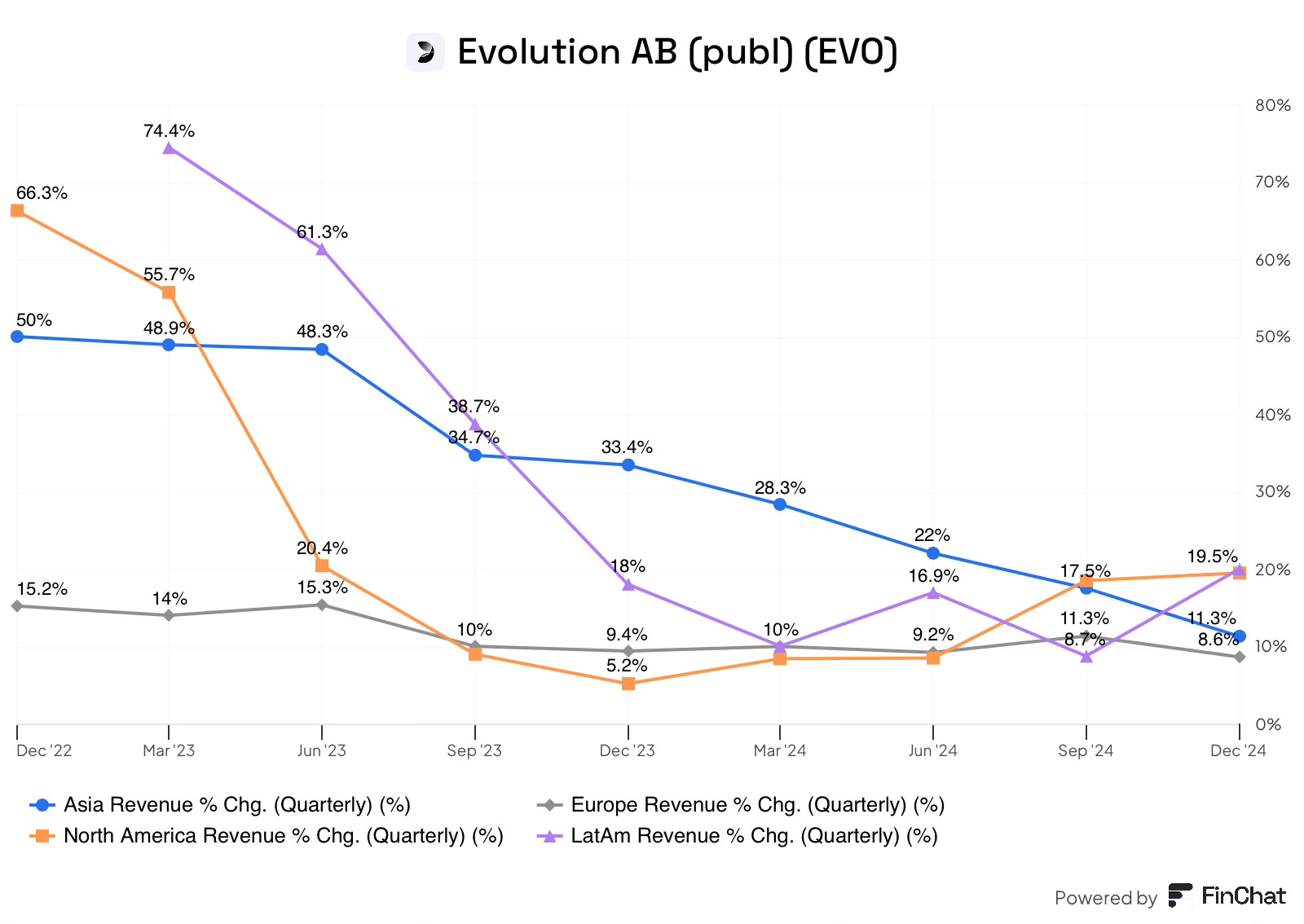

Geographic growth was a tale of two halves. On the positive side, North America and LATAM both accelerated growth, while Asia and Europe saw decelerations.

North America: The segment sustained a high level of growth from Q3, growing by 19.5%. The growth was driven by strong Live casino performance and improved momentum in RNG.

On the live side, the company experienced “brand expansion in all studios,” with partnerships announced with FanDuel and Atlantic Lottery. These partnerships will likely keep strong momentum for the coming quarters.

On the RNG side, the company experienced improved momentum from the declines it had experienced in previous quarters, despite this, the segment still lost market share. It is important to note the company has a dominant position in RNG in North America, so these losses are not surprising. The company is combating these market share losses by launching new tailored RNG games in North America, which I expect to help.

LATAM: LATAM experienced a strong rebound in demand during the quarter. The company did not disclose what regions drove this strong growth. However, the newly regulated Brazilian market will likely sustain this growth throughout the year, despite a slow start.

Asia: Asia's growth slowed due to the cyber attacks I discussed above. While revenue will continue to slow, investors should take comfort from the continued strong underlying demand, which will become evident over time.

Europe: Europe continued its steady growth, slowing slightly from the previous quarter. Part of this slight slowdown is likely due to the ring-fencing I talked about in regulation.

Going forward, several aspects leave me optimistic about the long-term growth of the business:

Live strength in North America

The effect of Brazil on the LATAM market

RNG turning a corner

Asia working through the cyber attacks

These factors should allow the business to maintain or even accelerate growth.

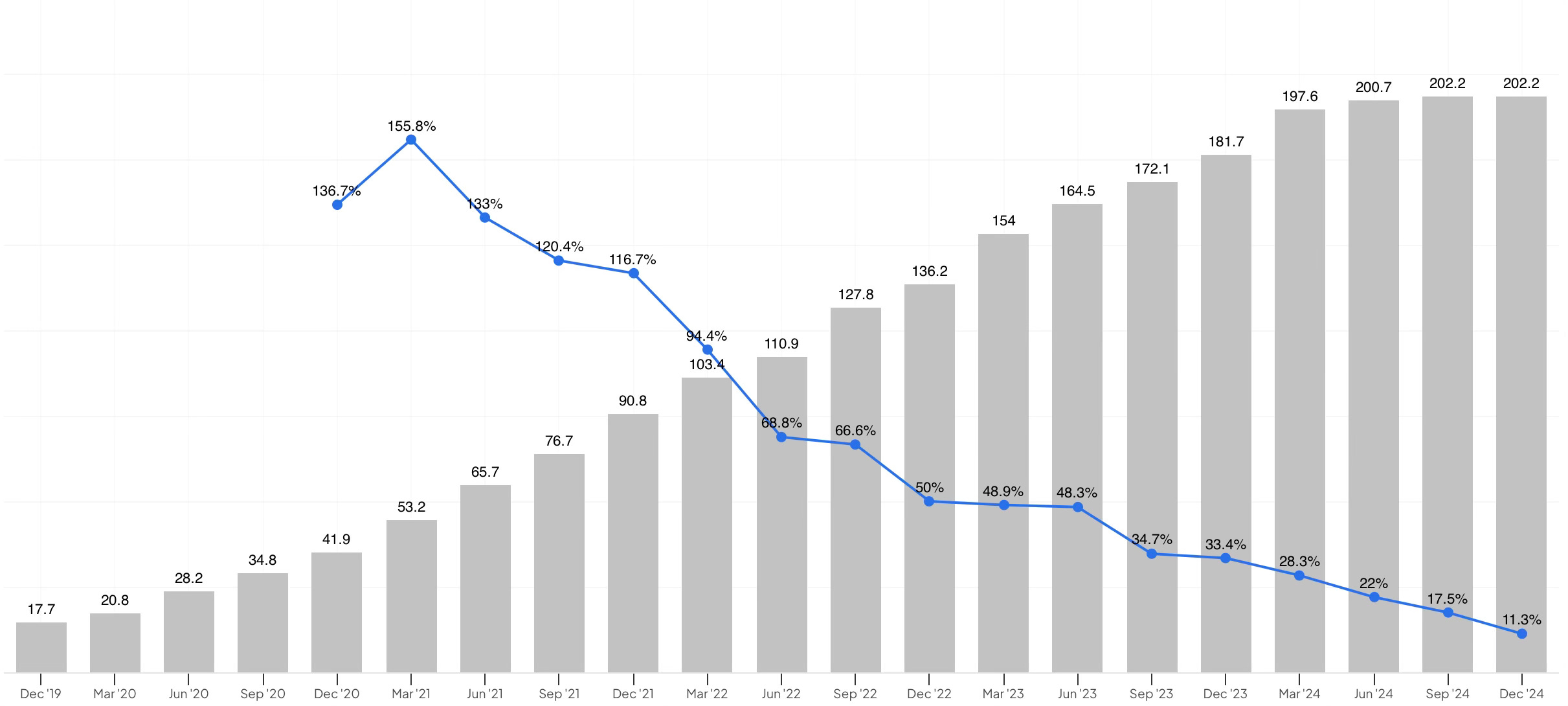

Earnings: margin compression and higher taxes

While the GAAP numbers point to strong margin expansion, the €91.4m in operating revenue hides the margin compression during the quarter.

The company reported €377m in profit before tax, however, when excluding the other operating revenue, this number drops to €285m, a 1% increase from the period last year.

While I don’t like to use EBITDA, the chart above clearly demonstrates the margin compression. Q4 margins contracted from 70.9% last year to 68.1%. The contraction was caused by.

Asia Cyberattacks: This was the largest contributor to lower margins, the reduced growth and increased costs resulted in the region experiencing lower profitability.

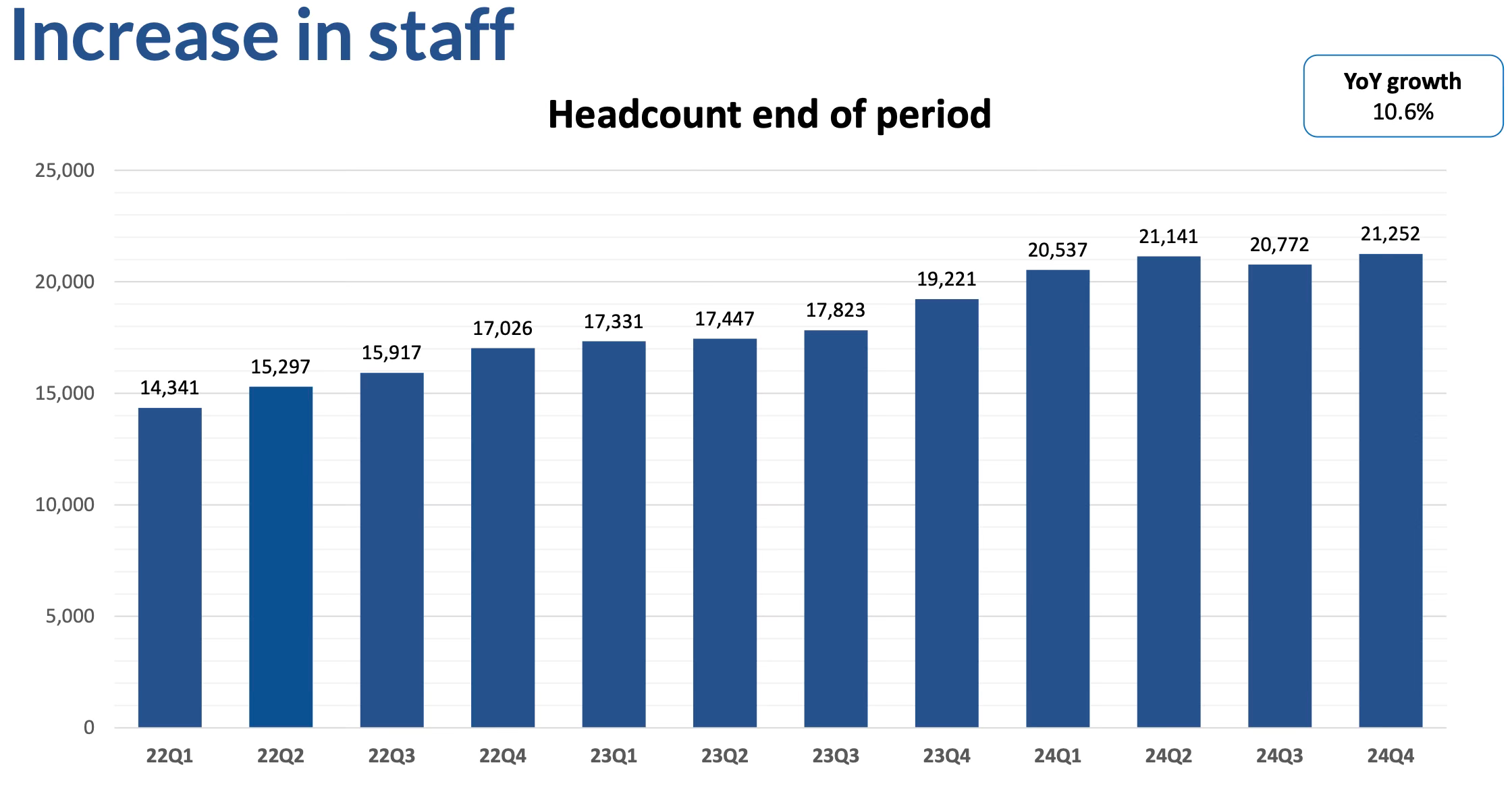

Increased employee costs: For the year, Evolution increased the employee count by 10.6%. The company is seeing strong momentum with its recruitment efforts, a positive indicator considering Evolution will need to staff 3-4 new studios and increase capacity in Colombia during 2025.

On the downside, personnel costs grew 16% due to the company working with a more expensive mix of employees.

The result of heavy recruitment efforts and slightly higher personnel costs will likely result in sustained higher expenses in 2025, potentially impacting margins further.

Investments: The company remains in a heavy expansion phase, impacting margins due to the costs of building studios, increasing capacity and investing in technical infrastructure. These factors likely caused other operating expenses to increase, and will likely continue increasing similar to personnel expenses.

Taxes: Tax costs for the quarter increased from €20m last year to €48m; these higher tax costs are unfortunately here to stay. However, beginning in Q1, the company will have had 4 quarters of higher taxes, which will mark the end of the headwind to profitability.

While it is never pleasant to see margins compress, the company is making the necessary investment to ensure the long-term success of the business.

Capital Allocation

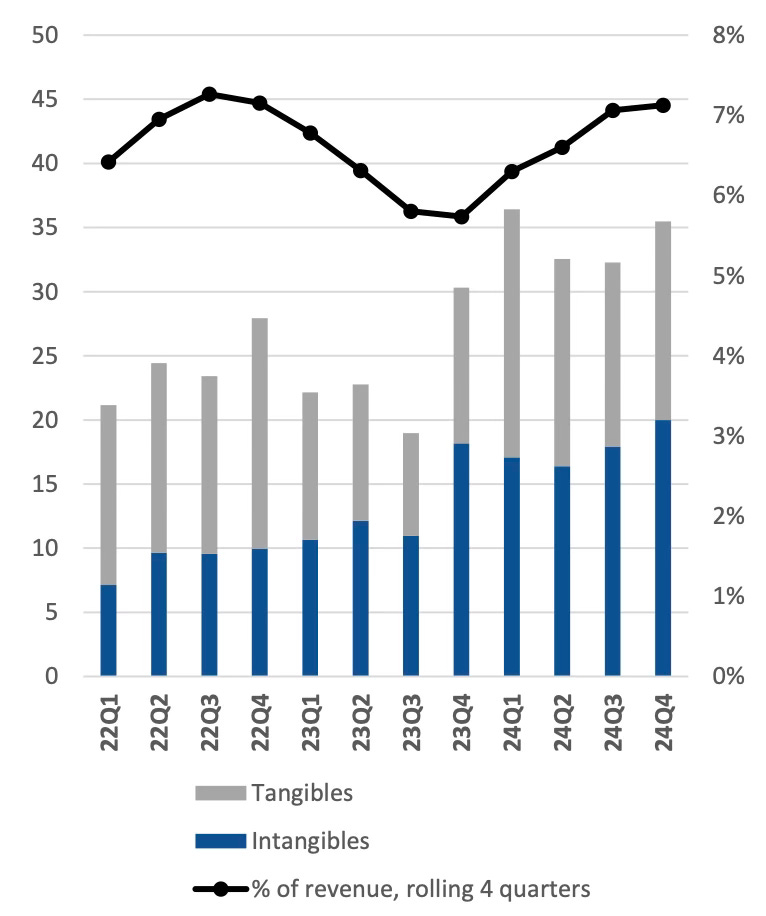

First and foremost, Evolution continues to invest in the business. They are doing this in two ways:

Tangible investments: studio expansion and technical infrastructure

Intangible investments: Game development

The combination of these two account for 7% of revenue.

I have discussed these investments in greater detail above.

Capital Returns

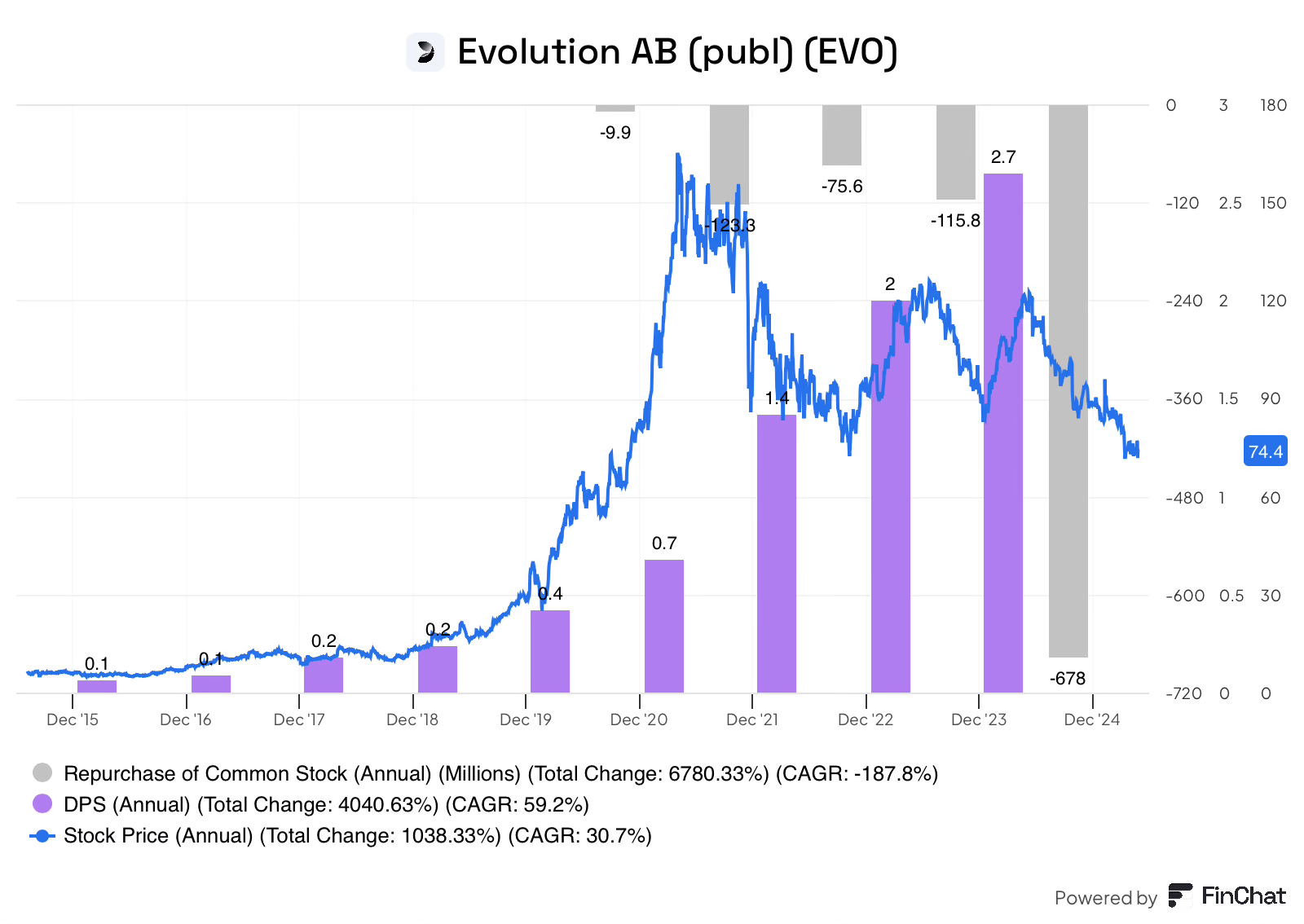

With the remaining capital left after investing in the business, Evolution is returning nearly all of it to shareholders through share repurchases and dividends.

Buybacks: In the quarter, the board of directors continued to take advantage of the weak share price by repurchasing shares worth €150m. For the full year, Evolution has now spent €678m on share repurchases, reducing shares outstanding by over 3%.

Furthermore, Evolution has committed to spending €500m on repurchases during 2025, which should result in another 3% reduction in shares outstanding.

Dividend: The company has announced that it will be paying a dividend of €2.80 per share for the full year, a 6% increase from the €2.65 dividend in 2023.

The combination of buybacks and the dividend means over 7% of the company’s market cap is being returned to shareholders each year!

While I can complain that I would rather have 100% buybacks, the return of capital is welcome either way!

Conclusion

It is clear from this report that the company has its fair share of troubles: Cyberattacks, capacity constraints, FX headwinds, US market share losses, a dynamic regulatory environment, CFO transition, and investigations from both the UK Gambling Commission and Swedish regulators.

The company continues to face these issues rather than shying away. They seem to be making rational long-term decisions to combat each of these issues, such as; building the necessary defences to prevent future attacks, building capacity, focusing on local games for the US, and working with regulators.

However, despite the headwinds, there is a lot to like.

The company is investing significantly in expanding its game advantage over competitors, the most important factor in the long run.

Strong Live casino performance.

The RNG businesses seem to be turning around one by one.

Capacity investments will result in 3-4 studios coming online in 2025, alleviating capacity constraints.

New markets opening such as Brazil.

Insider repurchases.

Significant capital returns to shareholders.

The combination of 16% underlying business growth along with 7% additional shareholder returns coupled with the stock trading at a 12.5X earnings multiple, make Evolution’s stock an attractive proposition currently.

Sources: Company filings & transcripts unless otherwise linked.

Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment decisions.