2025 Annual Report

Welcome to my full year portfolio update!

Substack Update

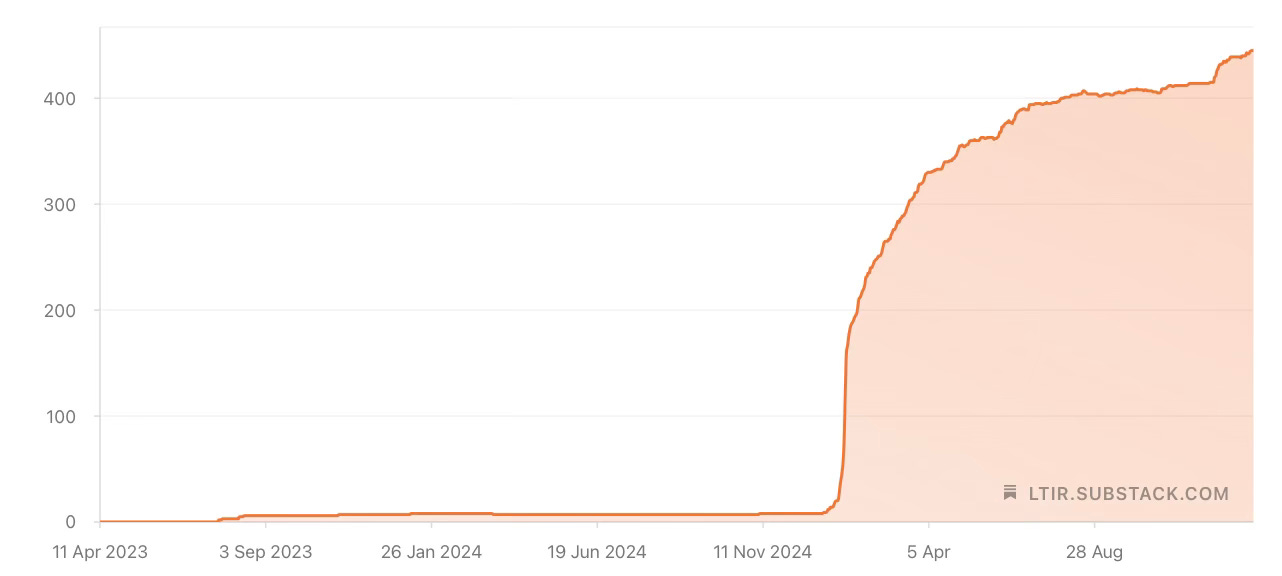

2025 was the year that I committed to posting my deep dives and performance solely on Substack.

As a result, my subscriber count grew from near 0 to almost 450!

Over the year, I published 8 in-depth company deep dives: Evolution AB, Airbnb, Crocs, Paycom, Xpel, Moncler, Charter Communications, and Judges Scientific.

Refinement

This year I have spent considerable effort refining my research and writing. My first deep dive: Evolution AB, consisted of three lengthy articles that covered almost every aspect of the business: understanding, financials, moat, competitive dynamics, opportunities, risks, and valuation.

Although this deep dive remains my most popular series (by a considerable margin), this is likely due to the company and circumstances under consideration. Since then, I have worked to cut through the noise and focus only on the most important aspects of the business, resulting in more concise and in-depth dives.

While most investors focus on the quarterly numbers, credit card data, headlines etc. I prefer to focus on the “roots” of a business, a term coined by Nima Shayegh to describe the underlying forces that cause the current and future economics of a business, these mainly qualitative factors include: the product, company culture, management capabilities and alignment, opportunities, and risks.

With most market participants focused on what the next quarters results will be, these qualitative factors should give me insight into a company’s reinvestment profile that give me an edge in identifying mispriced opportunities that I can hold for the long run.

The latest iteration of my research process can be seen in my Judges Scientific deep dive, where I set out to answer only three questions:

Why has the business been so successful up to this point?

What are the odds this success continues? And for how long?

Is it available at an attractive price?

It is important to stress: I by no means think this is the finished template for future deep dives, but I do believe it has more of what matters and less of what doesn’t when comparing my work to this time last year. I will continue to refine my approach indefinitely.

Portfolio updates

My monthly portfolio updates have also been a source of experimentation. However, I have decided to shift these to a quarterly basis. I invest in companies for long periods, 10+ year time frames, so it makes little sense to report on how these companies are doing from month to month.

The plan for 2026

In the future, readers can expect:

Specific company deep dives: Similar to before, I will aim for these to be single, 20-30 minute reading time reports. There will be no set time frame; instead, they will be as and when I find something of interest to research, whether that is a beaten down stock or a watchlist candidate.

Quarterly portfolio updates: Short articles outlining performance, portfolio holdings, transactions, etc. These will now be quarterly.

Company updates: If I feel it is appropriate, short company updates will be written on previously covered companies. Unlike many of the quarterly updates you see, these will be posted only if there is anything of consequence to discuss.

Thank you to all of you who joined me in 2025, I look forward to continued learning with you all in 2026!

Portfolio Performance

In 2025, the portfolio trailed my benchmark, the S&P 500, by a small margin, posting a gain of 16.5% versus the S&P 500’s 17.9% increase. After a strong year in 2024 (+35%), I consider this slight underperformance as acceptable.

While it may be entertaining to compare results on a quarterly or yearly basis, my true north star is to outperform over an investing lifetime.

On this front, the results are tight. Since I began on November 4, 2020, the portfolio has grown slightly ahead of my benchmark.

My portfolio: +115.18% (15.97% annualised rate of return)

(Note: returns are tracked across 3 brokerage accounts; calculations to combine these into one figure may contain mistakes. Calculation method remains consistent.)

S&P 500: +98.8% (14.26% annualised rate of return)

While I am happy to be ahead so far, a longer period, likely decades (and cycles), is required to determine whether this is luck or skill.

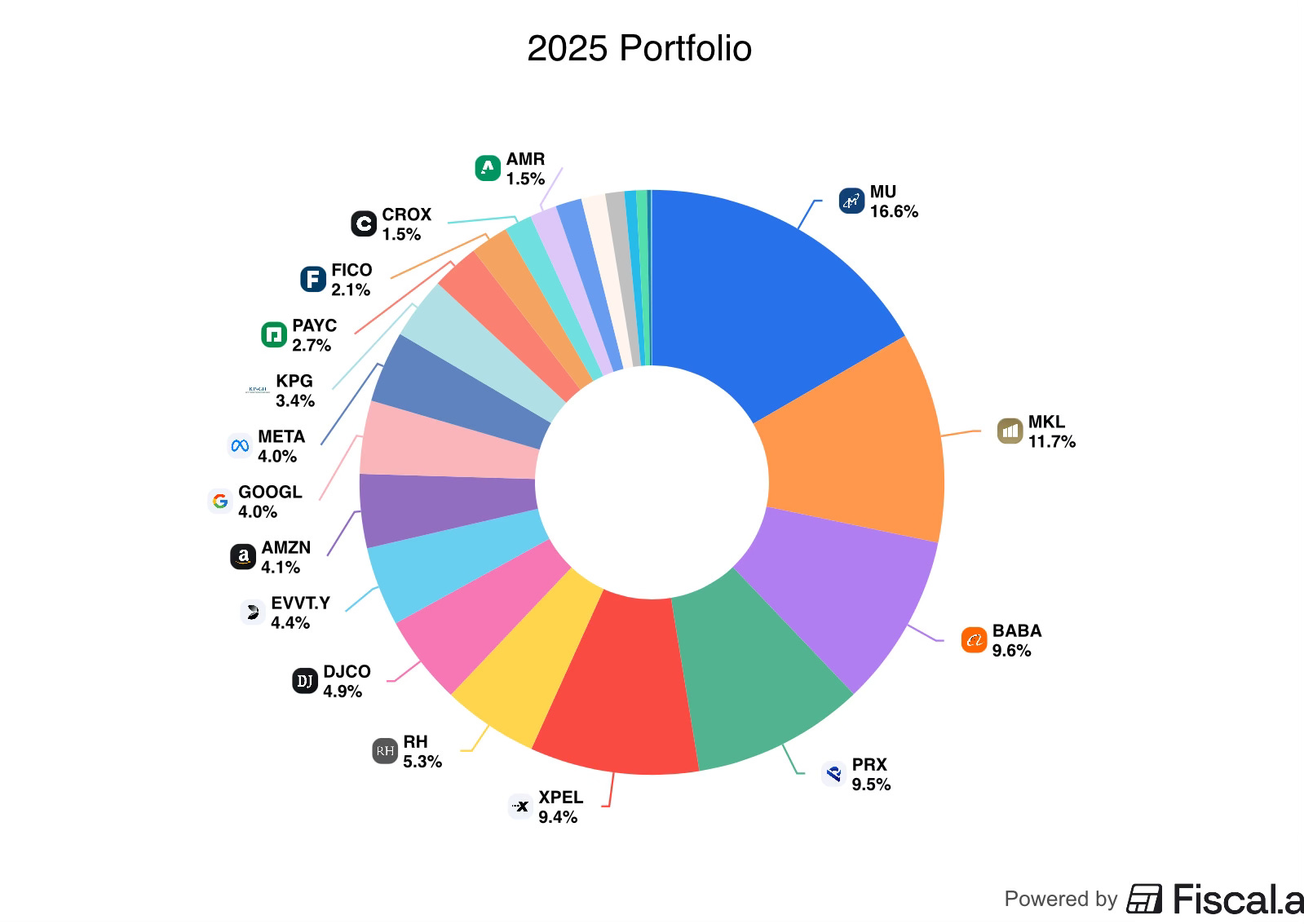

Portfolio Holdings

Investable Universe (watchlist)

Airbnb ($ABNB)

Moncler (€MONC)

Notable performances

2025 Top Performers

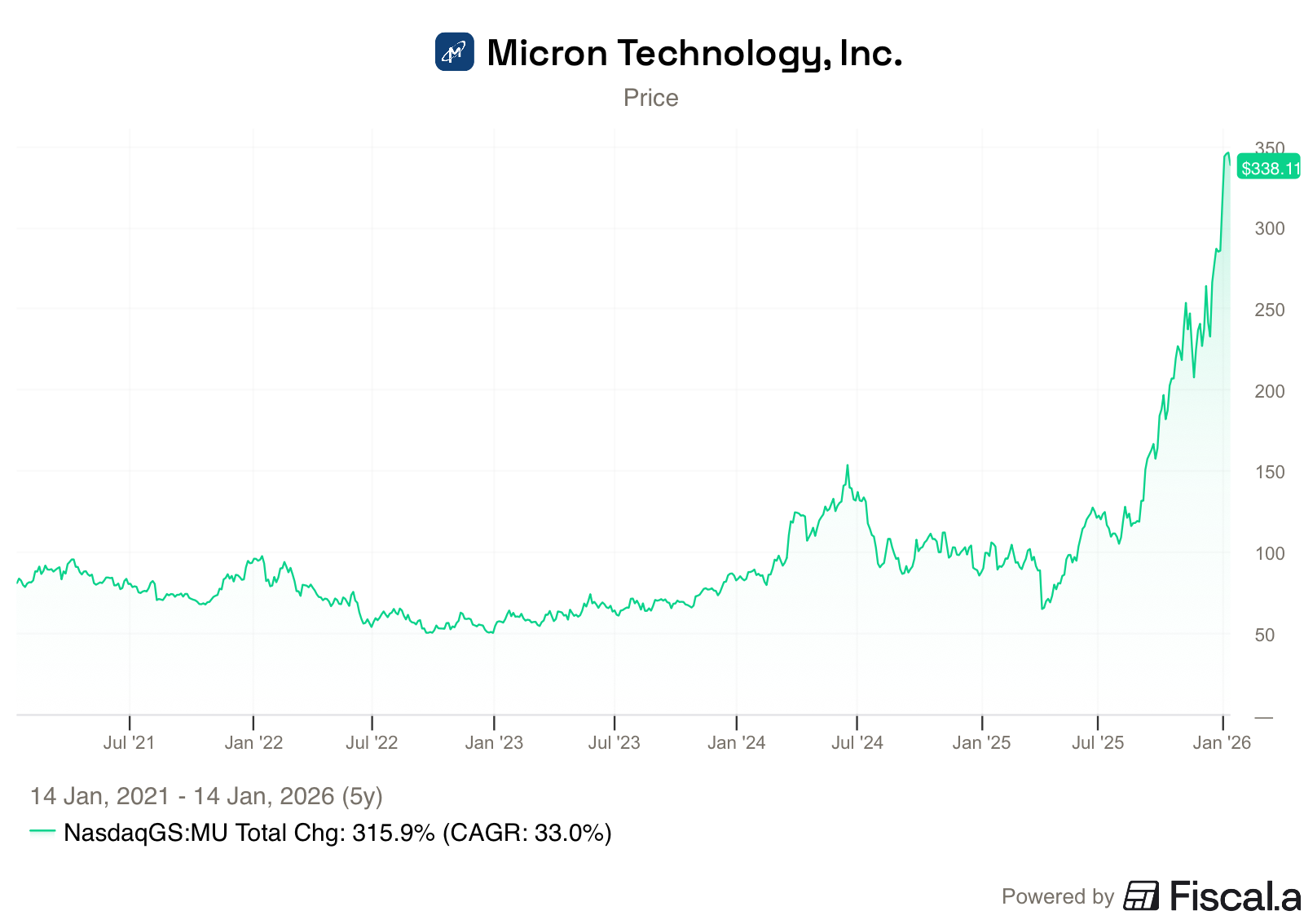

Micron Technology ($MU) +242%

Alibaba ($BABA) +77.5%

Alphabet ($GOOG) +59.3%

2025 Worst performers

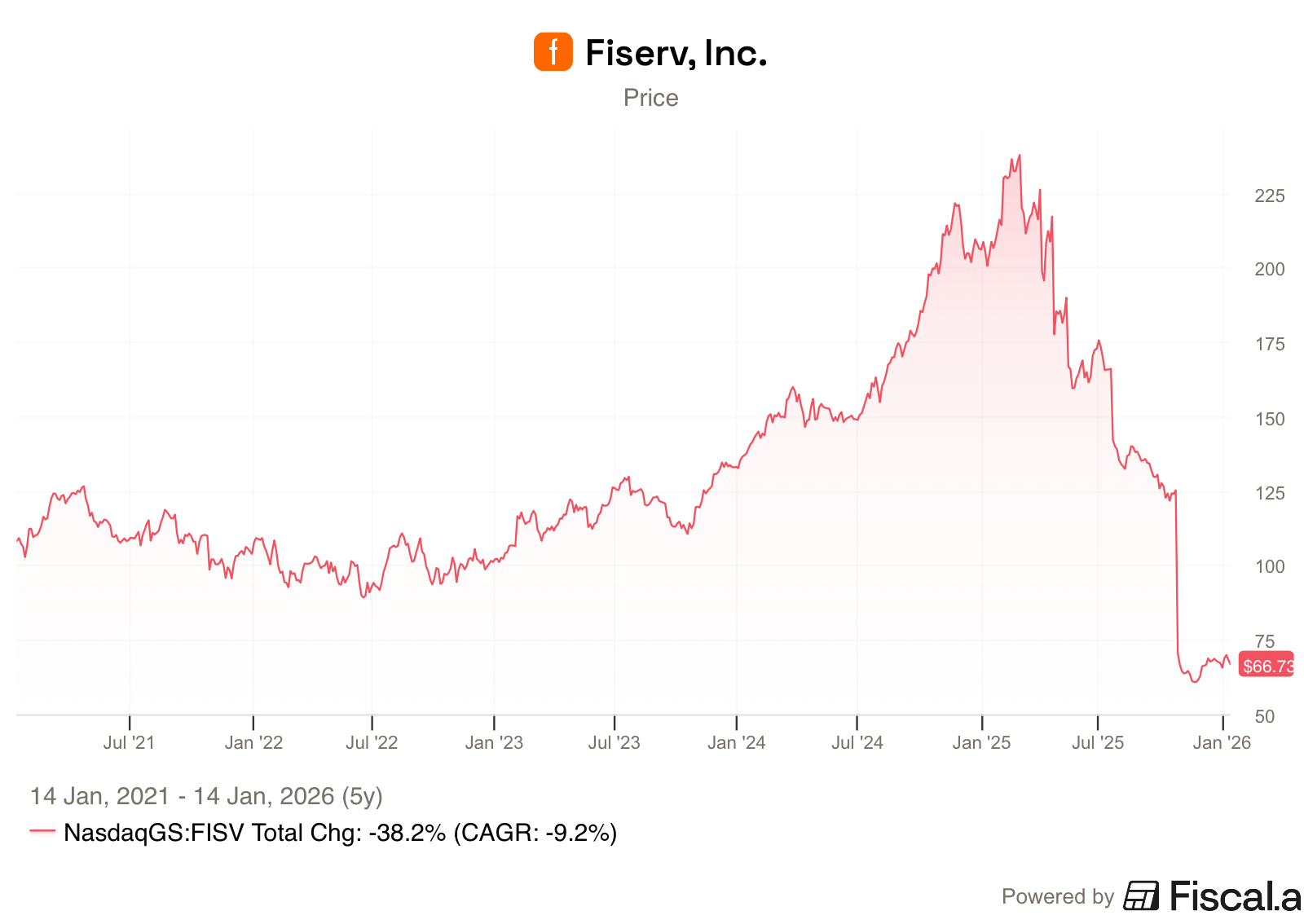

Fiserv ($FISV) -66.7%

RH ($RH) -48.9%

Charter Communications ($CHTR - no longer in portfolio) -40%

Portfolio performance has been a tale of two halves: The largest positions performed strongly while smaller holdings underperformed.

Micron Technology ($MU) was the most notable performer in 2025. Following a weak first half, the stock soared nearly 250% in the second half of the year. The strong performance was attributable to demand outstripping supply for leading edge HBM & DRAM chips due to the wave of AI demand, this tight supply environment led to chip prices rising several times over.

Although the chart looks ominous (bubble territory) at 30X earnings, it is not so clear to me that the business is egregiously overvalued. Earnings are expected to almost double in 2026 as the tight supply environment persists. The company has been historically cyclical, which has warrented a lower valuation versus the rest of the semiconductor industry. However, with demand shifting towards HBM products, which are significantly more resource intensive, Micron has been able to achieve greater pricing visibility. Additionally, the significantly higher wafer capacity required could create a persistent tight supply environment. Both factors increase the quality of the business, potentially warranting a higher valuation (versus historical metrics).

Another reason to hold onto the the position unless it become egregiously overvalued is the maxim that

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves” - Peter Lynch.

I am optimistic about the long-term opportunity ahead of Micron, so unless the stock reaches an obviously egregious valuation, I am happy to hold.

My long standing China investments ($BABA & $PRX) also turned green in 2025 as sentiment began to shift. The two stocks still look attractive as they position themselves to benefit from the AI wave, I continue to hold.

On the other end of the portfolio, Fiserv was the worst performer after the previous management understated the benefit Argentine hyperinflation was having on the business. Additionally, several actions to boost short term growth over long term sustainability came to light, such as underinvestment in critical technology, cost cutting, and agressive pricing actions at Clover to achieve short term targets. Incoming CEO Mike Lyons reset expectations to take corrective action, leading to a steep decline in the share price. Although Fiserv has prided itself on consistent double digit EPS growth, the business is becoming increasingly mature, higher growth segments must compensate for the lower growth segments, as a result, double digit growth is going to become increasingly difficult. Following Frank Bisignano stepping down from the CEO position, I seriously considered selling this stock, in hindsight, holding on was a mistake. Today, I am less optimistic about the future of the business, but view it as cheap, therefore, similar to my position in Charter, if more attractive long-term opportunities present themselves, this will likely be a source of capital.

Going into 2026, the portfolio continues to be (as a whole) higher quality and cheaper than the broader market, positioning it well for the future.

Transactions

I made very few transactions in 2025.

During the first half of the year, I continued to add to my small Evolution AB position, making it a full position by mid-2025 (7%+).

The tariff tantrum in April also presented an opportunity to add aggressively to existing holdings: Xpel, RH, Micron, and Crocs at attractive prices.

In December, I sold my small (1% position) Charter Communications holding, my first sale in 3 years. I have held Charter for over three years; during this time, the business has not performed as expected due to new forms of competition eroding its market share with no signs of stopping. Initially I believed this competition would be temporary, but this has proved wrong. As a result, the potential range of outcomes for the business has been meaningfully lowered. Additionally, my wrong analysis makes me question whether I truly understood the business. In the future, I may write a dedicated post on my learnings from this investment.

The proceeds of this sale were allocated to an initial position in Judge’s Scientific, which I viewed as a more attractive long-term opportunity.

In total, these transactions resulted in a continued turnover of less than 10%.

Concentration

“The way to win this game is extreme patience and extreme selectivity.” - William Green.

Top 5 positions: 57.3% of portfolio

Top 10 positions: 79.7% of portfolio

Total positions: 22.

Similar to the S&P 500, returns have gravitated towards the largest positions, naturally increasing the concentration of the overall portfolio. 12 positions continue to make up the remaining 20% weighting, which I consider to be too many. As I noted in my October update, I will reduce this number deliberately and methodically to reach just 12-15 total portfolio holdings.

While many may not be comfortable with this level of concentration, and some may argue it is not concentrated enough, I believe it is the right balance for me.

Learnings from 2025

“Any year that you don’t destroy one of your best-loved ideas is probably a wasted year.” - Charlie Munger.

My investment philosophy can be summed up by this quote from Santa Monica Partners:

Competitive advantages that allow for superior margins, predictable market shares and high returns on capital.

Continuous capital reinvestment (paying a dividend goes against the goal of wealth creation).

An attractive price/value relationship at the outset.

Executives who manage the business aggressively and conservatively with the incentives of ownership.

The importance of management

The most significant evolution in 2025 is a far greater appreciation of the role that management plays in outperformance. Although I have always placed meaningful attention on management, this focus was amplified in 2025, with a particular focus on looking for founder-led companies. Founders tend to have far more skin in the game and a long term focus which tends to suprise to the upside.

While many investors rely on compensation structure and insider ownership to assess alignment. The way a manager has acquired that ownership, thier character and motivation, and actions during tough periods are arguably more important indicators of true alignment. Ideally, I would like a management team that is not driven by financial rewards at all.

Although I am not exclusively looking for founder led businesses, this appreciation of the benefits an owner-operator brings, has led me to raise the bar hired management teams will have to surpass before I am willing to invest.

Reflecting on my portfolio: the businesses that have underperformed my expectations are not those run by founders (although this may be a coincidence). In fact, when analysing the compensation structure of these companies, the incentives in place tend to lead management into these undesirable shareholder outcomes by overly focusing on one metric (that is likely adjusted) at the detriment of all else, including long term health.

"I think I’ve been in the top 5% of my age cohort all my life in understanding the power of incentives, and all my life I’ve underestimated it. Never a year passes that I don’t get some surprise that pushes my limit a little farther." - Charlie Munger

It comes as little suprise that Charlie Munger had it right all along!

Being Wrong

This is a lesson that I have learnt the hard way, but has been expertly articulated by Bill Nygren in a recent interview. Nygren points out that investors, even the best, are rarely right more than 50% of the time. Despite this, you can outperform the market handsomely over time due to the markets convexity: the important thing is how you respond to the mistakes.

A common habit of investors is to hold onto a position following news that alters the thesis or leaves questions around how much they know the business in question. The typical response is to wait, hoping for greater clarity as more news comes out. Nygren disagrees with this approach, arguing that the best response is to sell if the news would mean that you would no longer buy the stock (if you didn’t already own it).

Oakmark’s data shows that following a mistake on a particular company, they are at higher odds of making subsequent mistakes on that same name. Implying that the best course of action is to simply move on. You want to be patient when the stock market is not acting right, and impatient when the business is not performing as expected.

This act of recognising mistakes early and quickly recycling that capital into higher probability opportunities has led to Oakmark outperforming the market by a significant margin over time.

Disclaimer: Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment

Really enjoyed your 2025 annual review it’s a strong way to step back from quarterly noise and see the bigger themes, trends, and lessons that actually mattered over the year. Summarizing performance with context helps highlight where conviction paid off and where flexibility was more important. That makes me curious: looking ahead into 2026, what’s the one theme from 2025 you think investors should keep and one they should discard?

I’ve subscribed and would be happy to support each other.

Jorrit