Trimming Micron ($MU)

The rational behind trimming my largest holding

Disclosure: I am long shares of Micron Technology ($MU)

Note: this article should not be considered investment advice; please see the full disclaimer at the bottom.

Welcome to Leeder Capital!

I have previously covered Evolution AB, Airbnb, Crocs, Paycom, Xpel, Moncler, Charter Communications, Judges Scientific, and, most recently, Duolingo.

I have not covered Micron Technology ($MU) on Substack because my initial investment pre-dates this channel. However, the stock, thanks to its recent run-up, has become a significant portion of the portfolio, and I thought my decision to trim required its own write up seperate to my quarterly review.

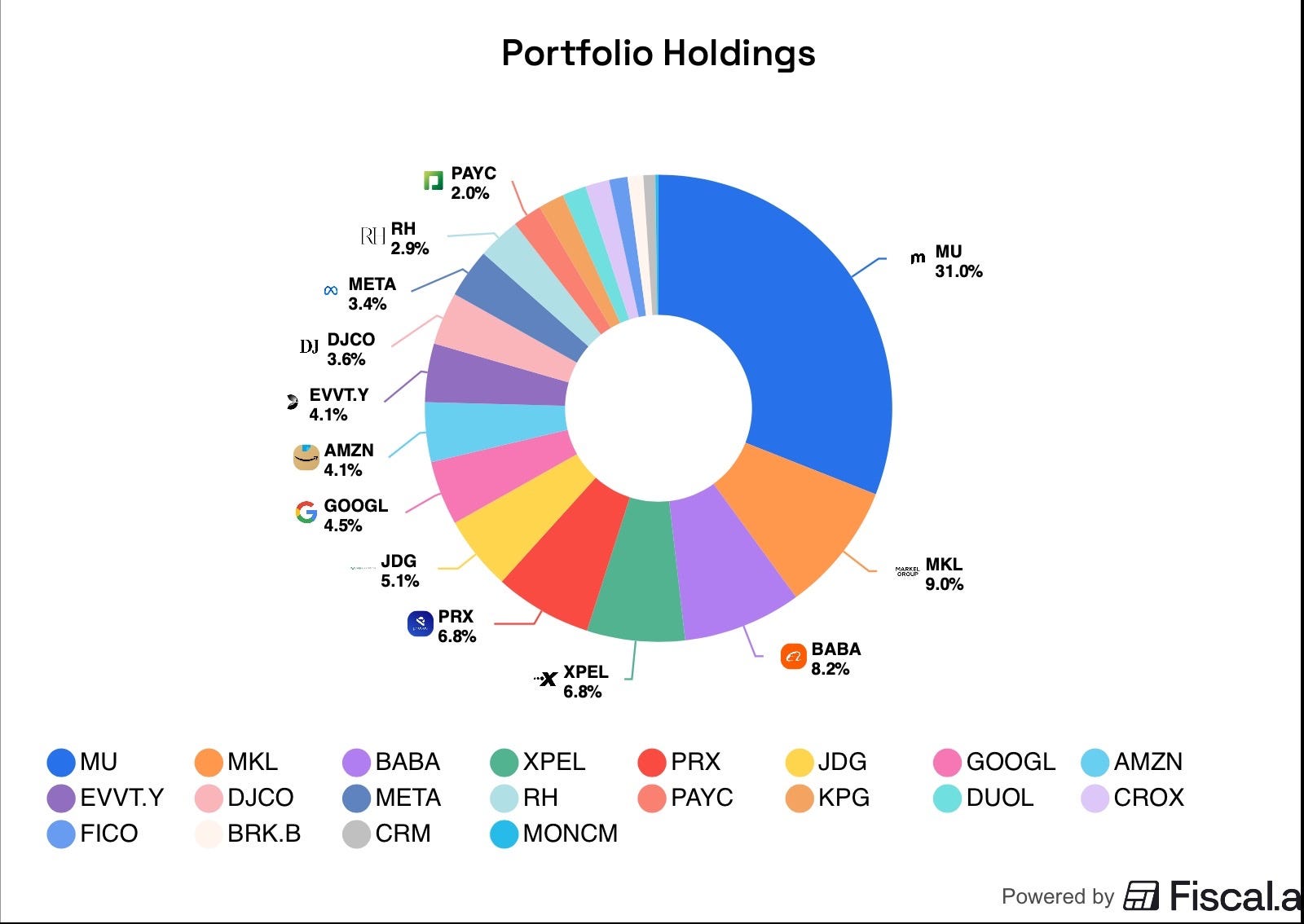

In May, I sold over two-thirds of my stake at varying levels from $700-$1,050+, a gain of 800-1,300% (my first 10-bagger). At the time, Micron accounted for over 31% of the portfolio, up from a 4-5% weighting at cost.

Although I am not afraid to hold a position with that kind of concentration, in this case, I was unwilling to accept the risks I believed present after such a meteoric run-up.

My ideal holding period is forever. I aim to think and act like a true owner of the business; reminded by quotes like;

“The first rule of compounding: Never interrupt it unnecessarily.”— Charlie Munger.

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” — Peter Lynch

In the past however, I have refused to sell positions that have looked egregiously overvalued, which has not ended so well.

As Micron’s share price has risen, I have found it increasingly difficult to justify scenarios that could generate a 10%+ annualised rate of return over the next decade, skewing the asymmetry to the downside. Learning from past experiences, I have taken a more proactive approach, heavily trimming the position; a decision that I have not taken lightly.

What has happened?

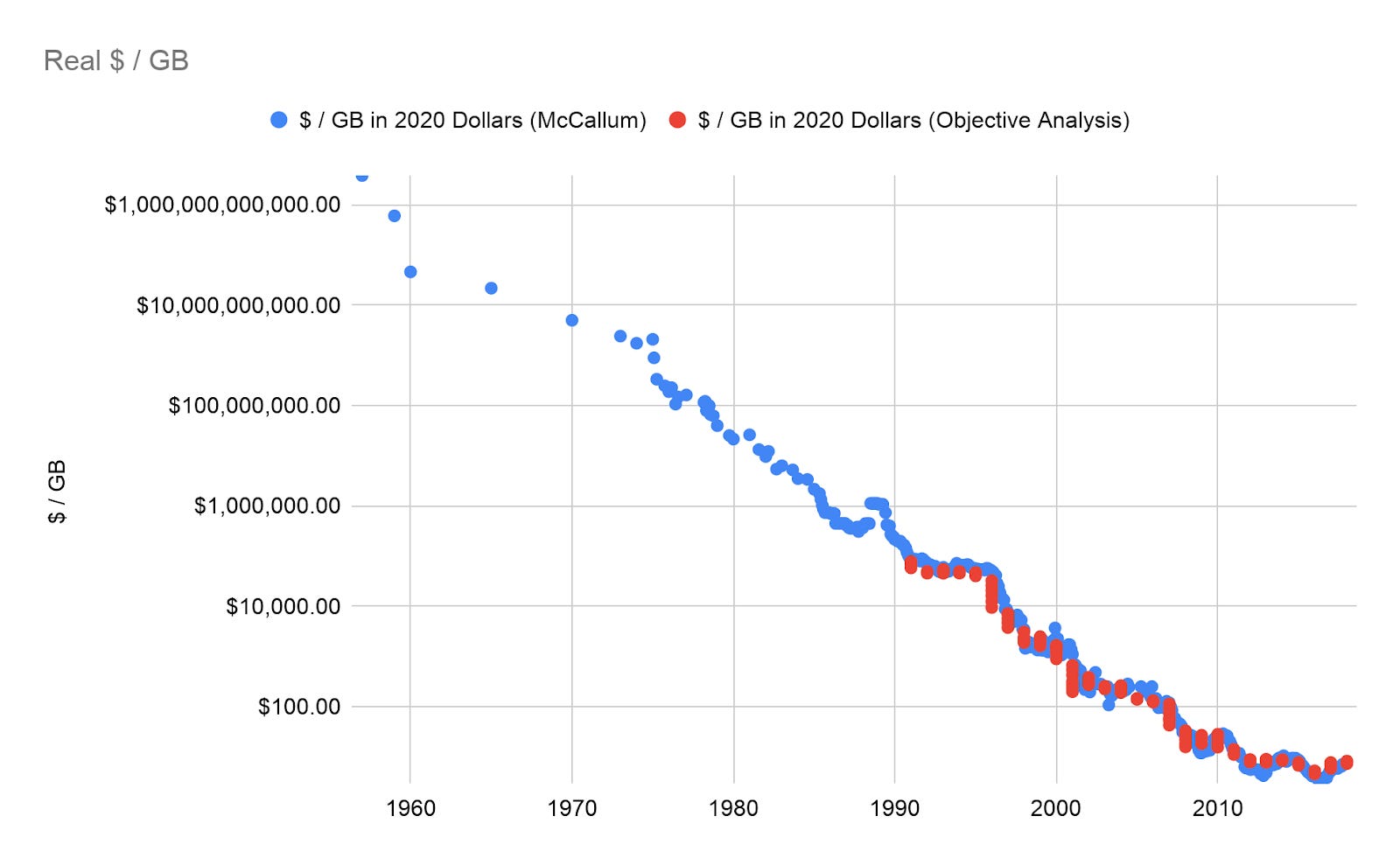

At the time of initial purchase (2022), the memory industry was experiencing a downturn from oversupply, high inflation, and China lockdowns. To most investors, memory was considered a bad business, valued on a price/book basis: the investment case was far from obvious.

My initial thesis was based on two factors: demand would grow across cycles, and competition had rationalised. Combined, these factors would allow Micron (and the other two DRAM players) to earn sustained satisfactory rates of return on incremental capital employed across cycles, something that had previously been elusive due to the cutthroat dynamics of the industry.

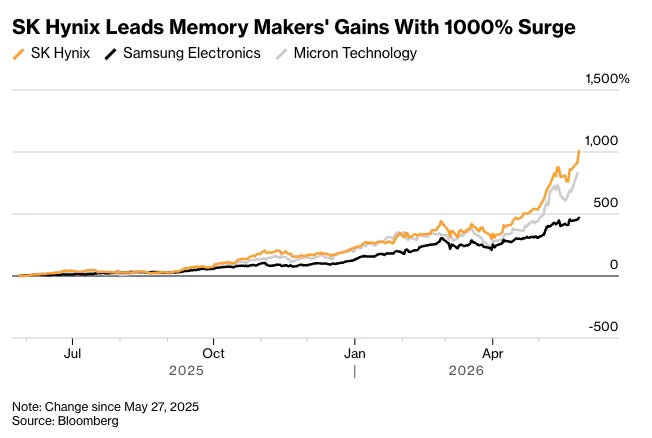

Since this initial purchase at $77 in 2022, demand for memory, crucial to AI, has increased beyond anyone’s expectations. Beginning in late 2023 and continuing to this day, demand has outstripped supply as AI has ushered in a new supercycle: hyperscalers, at whatever cost, have raced to build the infrastructure required for an AI future.

At the same time, HBM, then a side note, emerged as one of the most important parts of the semiconductor stack, and has been a primary contributor to the current bottleneck. Two factors have played a role here: The architecture of HBM (vertically bonded) requires approximately 3-to-1 wafer capacity versus traditional DDR5, and current yields that are meaningfully below previous 2D products.

As HBM demand grew exponentially, the industry shifted allocation towards HBM supply. So not only was supply failing to keep up with unprecedented HBM demand, but shifting allocation squeezed the supply of other memory products.

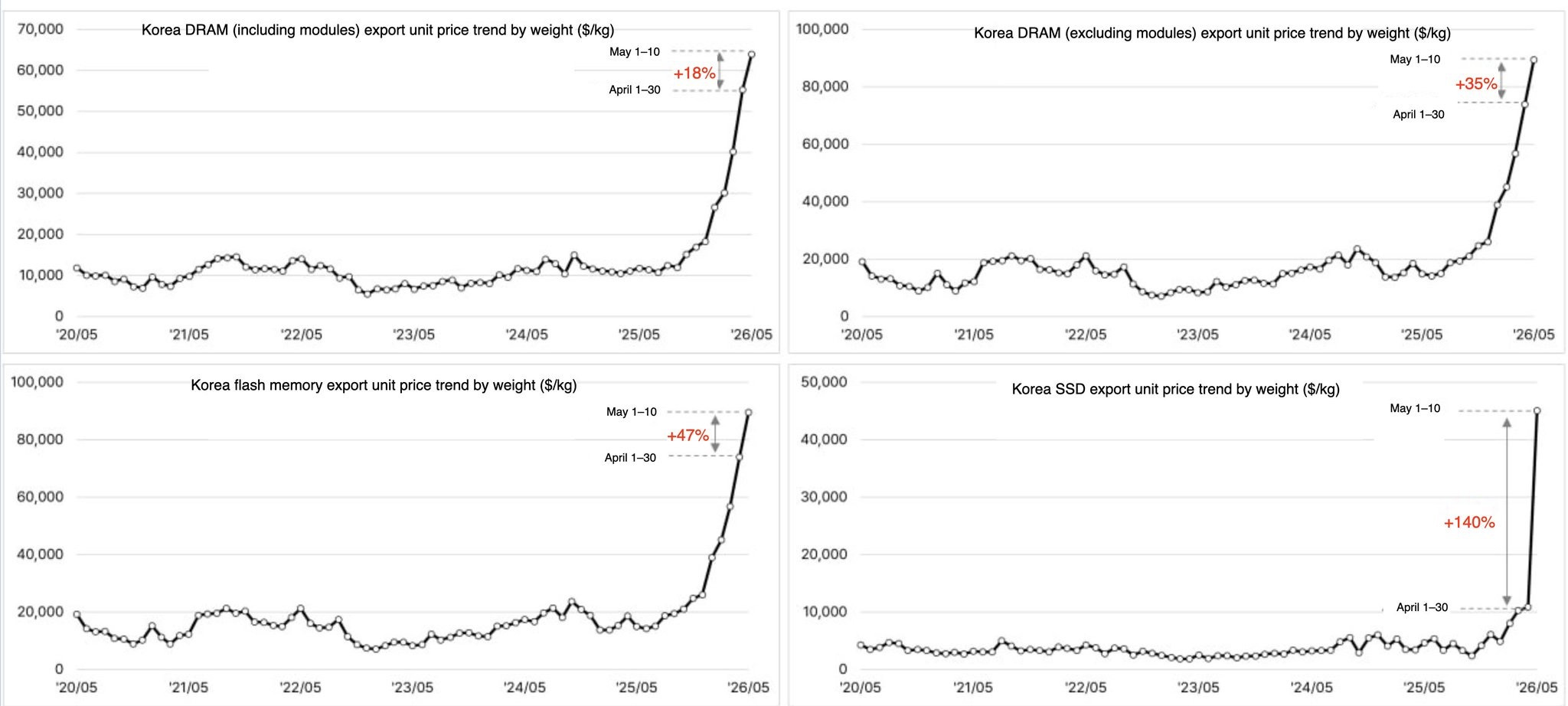

Long lead times (3-5 years) to reach volume production of a new fab have meant that new capacity is yet to come online, sustaining the bottleneck. With no new supply and demand continuing to grow, memory prices have gone vertical.

HBM is commanding contract prices up to 5x higher than traditional DRAM, while part of this delta is due to the nasency of this technology, the main component is the negotiating power memory currently holds over customers. For more commoditised products, spot prices have still grown by 200-400%, and still climbing!

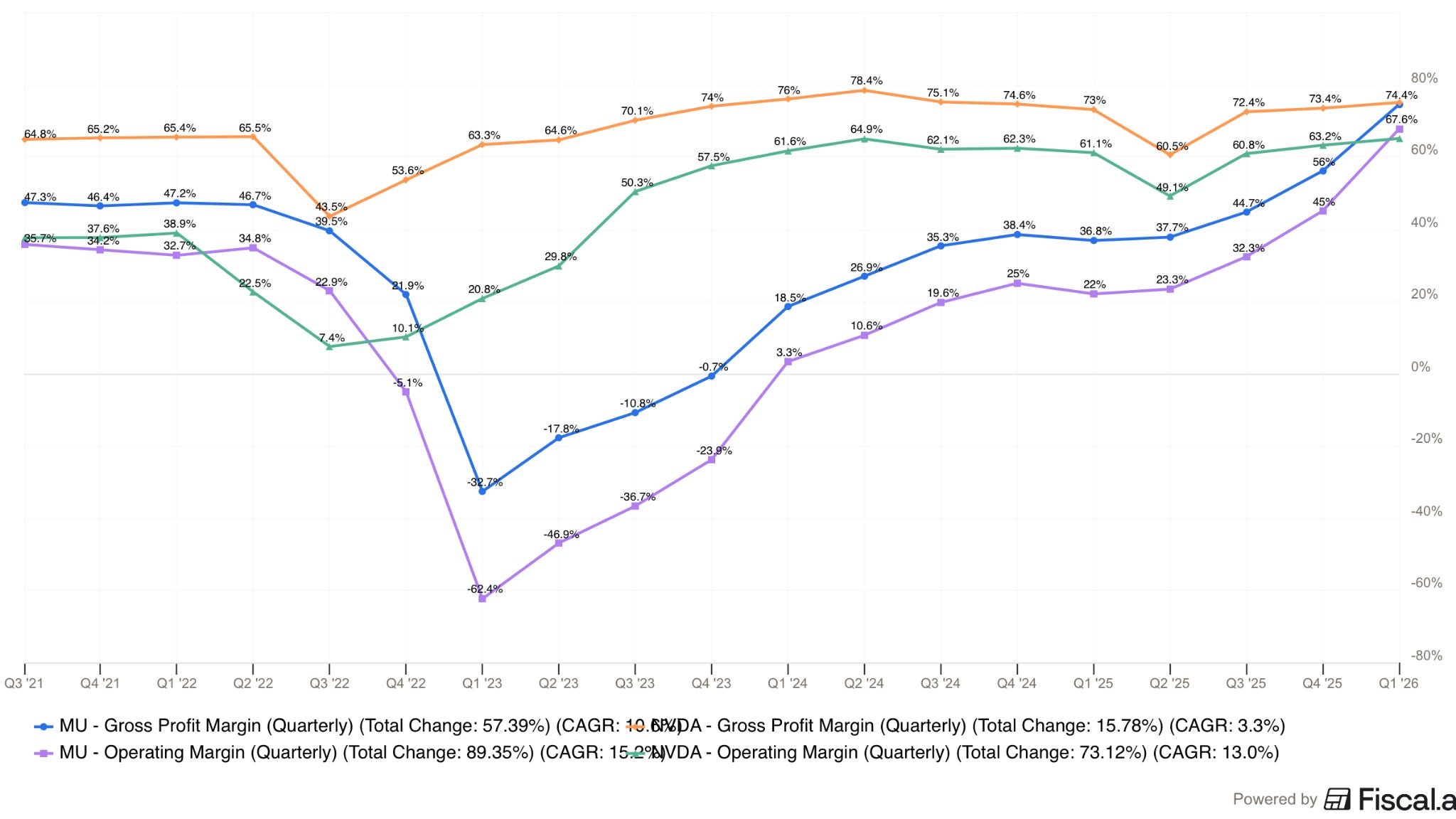

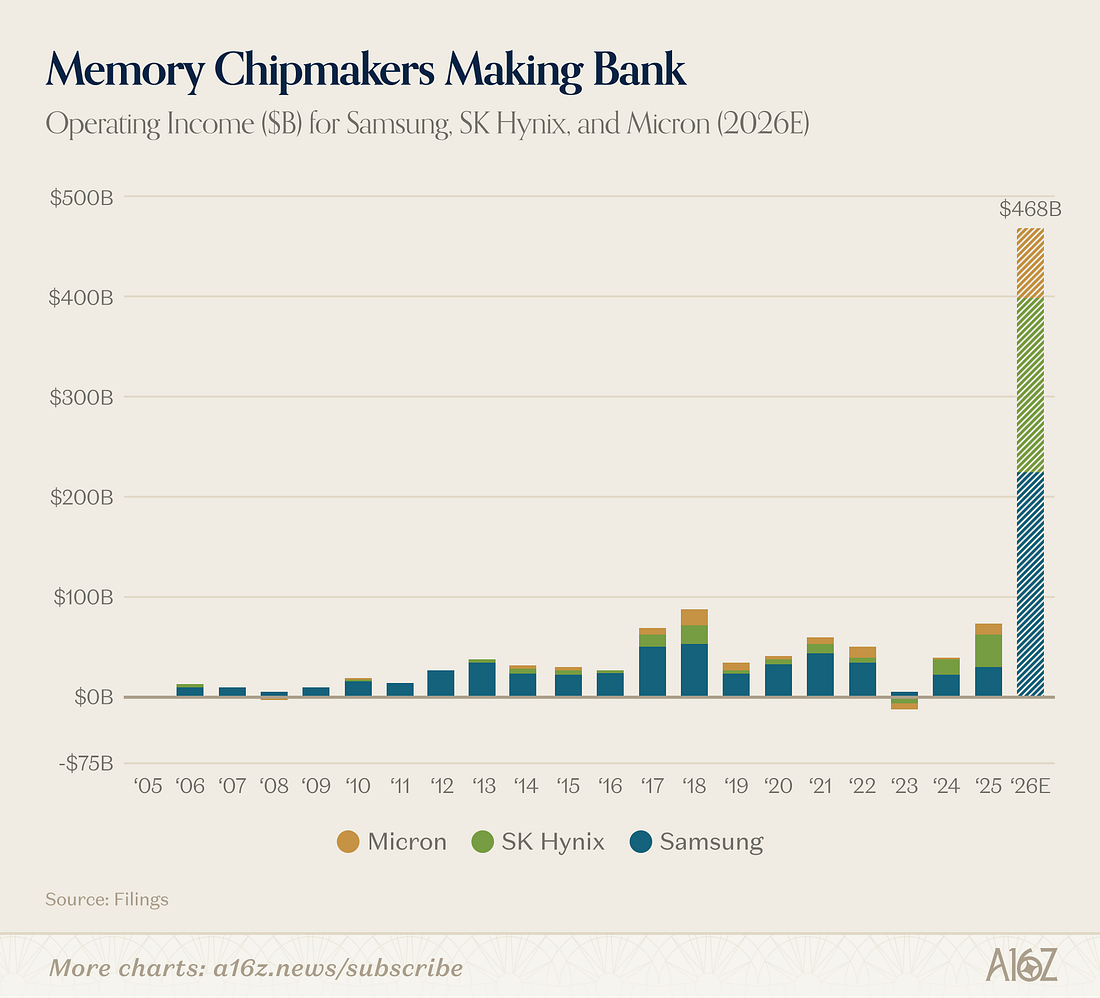

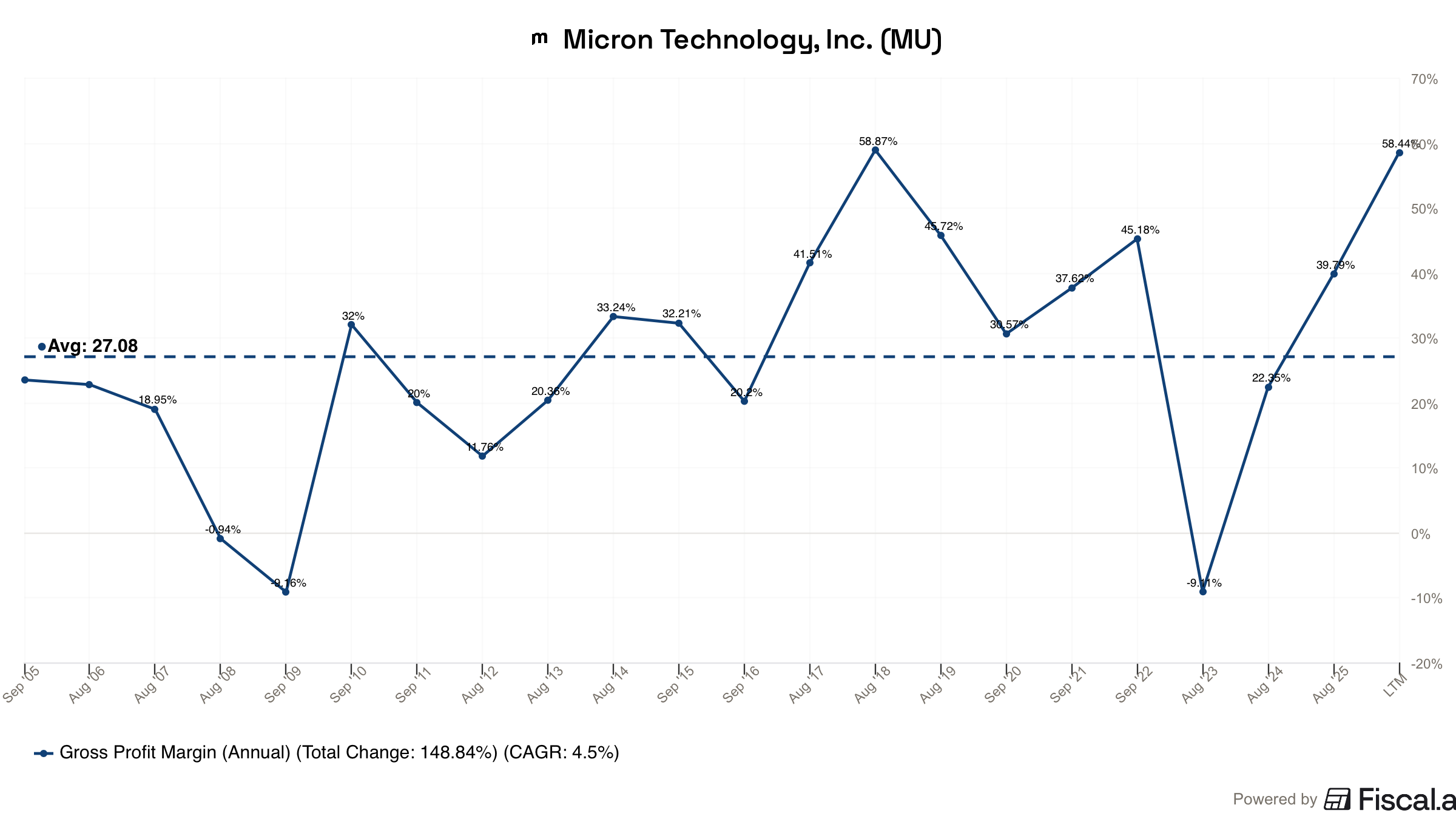

Due to the company’s fixed cost base, these higher prices have flowed straight to the bottom line, translating into the highest margins and net income that the industry has ever seen. To put it into perspective, Micron’s gross margins currently exceed Nvidia’s (and still rising), while 2026 earnings from the 3 OEM’s are estimated to be equivalent to 1% of US GDP.

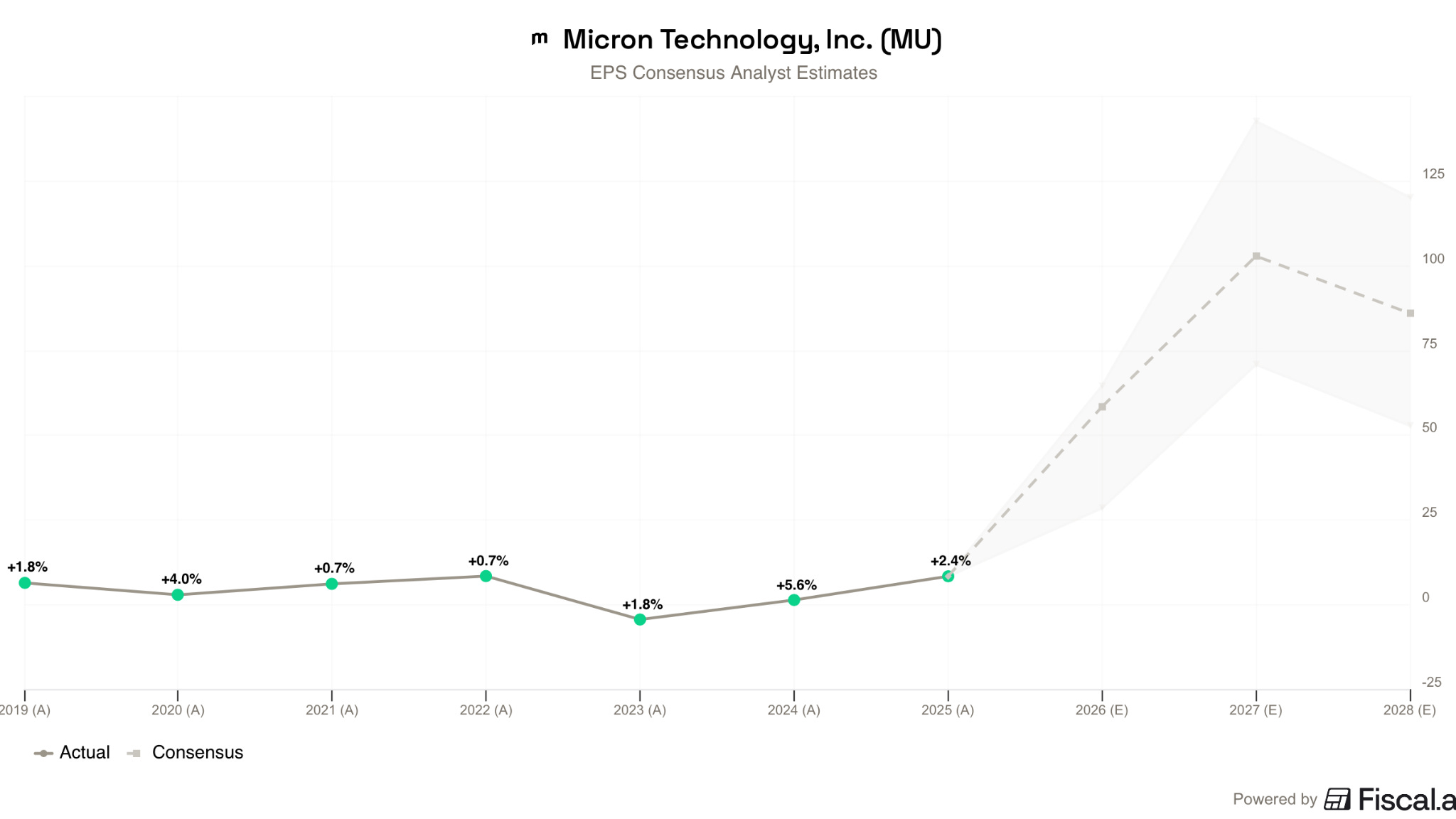

With new capacity not due to come online until early 2027 for SK Hynix, mid 2027 for Micron, and late 2027 for Samsung, the bottleneck is likely to persist for some time. Analysts are expecting Micron’s EPS to reach $50 in FY2026 and $100+ in FY2027, orders of magnitude higher than the $8 EPS at the peak of the previous cycle.

At the current share price (~$1,000+), Micron is trading at 9-10x 2027 estimated earnings.

The key question is, are these earnings sustainable over the next decade and beyond? If yes, then the current valuation may be justifiable; if not, Micron is likely significantly more expensive than first thought.

Price must be sustainable

From a starting price of ~$950, shares would need to reach $2,463 in 10 years to achieve a 10% rate of return from here. Breaking it down, Price and volume are the two key variables that will determine Micron’s success.

Looking at the technology waves that memory is riding, I think there is a high likelihood that more memory chips will be sold 5-10 years from now. However, with elevated prices driving significant operating leverage within the business, volume alone will not be enough to deliver satisfactory returns from here if prices should decline. This makes pricing the key factor to future success.

“When demand and supply are in stable equilibrium, if any accident should move the scale of production from its equilibrium position, there will be instantly brought into play forces tending to push it back to that position; just as a stone hanging by a string is displaced from its equilibrium position, the force of gravity will at once tend to bring it back to its equilibrium position. The movements of the scale of production about its position of equilibrium will be of a somewhat similar kind.”- Marshall’s principle of Economics.

So far, the forces acting on the memory industry have all worked in one direction to exacerbate supply, driving prices higher and higher. While the timeline is unknowable, I do not think that these prices, and therefore profits, are sustainable over cycles. As a result, I believe that Micron will be unlikely to achieve a 10% rate or return over the next 10 years in all but the most bullish of scenarios from here, shifting the asymmetry from the upside to the downside.

In the rest of this article, I will outline why I have come to this conclusion.

Bottleneck easing

Part of the original thesis was a conviction that competition had rationalised. Over recent cycles, the three DRAM players have been extremely disciplined, matching supply to demand, following years of brutal competition.

With prices at historic highs and customer appetite to build out an AI future at whatever cost running rampant, justifying the ROIC of new capacity investments is not a challenge. The risk is that supply discipline goes out the window.

Each player is stuck in the prisoner’s dilemma; if they do not increase capacity, they will lose market share and scale to competitors, while the necessary expansion multiplied by three could lead to excess capacity, which would impact prices.

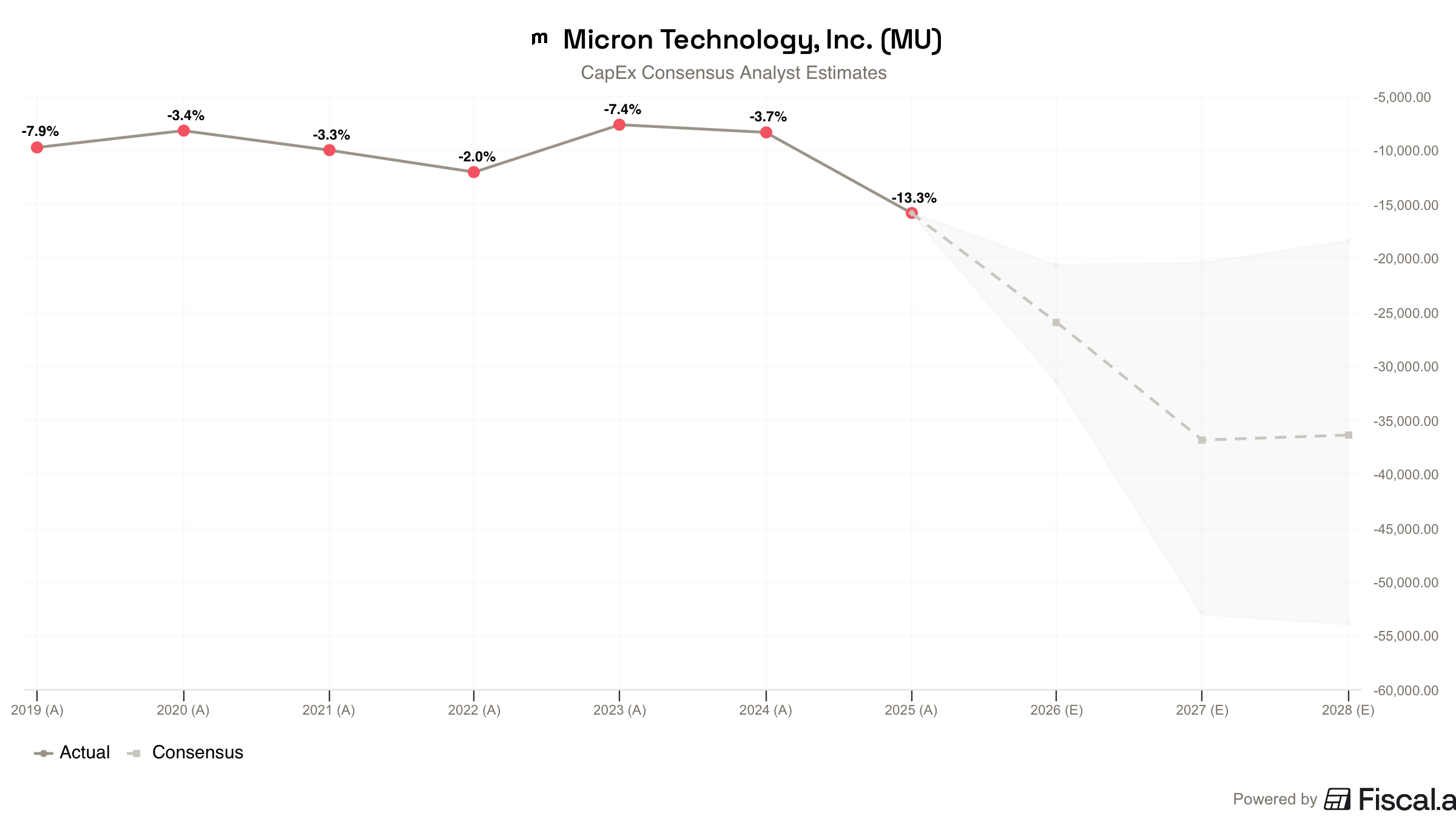

Each player is currently spending more than double their historical capex peak, and has committed to sustained capacity investments. Micron, for example, has announced plans to invest $200 billion over a decade+ time-frame, which is 4X the PP&E currently on the balance sheet, while SK Hynix has plans to invest $75 billion through 2028. Furthermore, with yields improving, existing fabs will be able to expand capacity.

This unprecedented level of investment, combined with yield improvements makes matching supply to demand an increasingly complex task. While it is impossible to predict when supply will fully satisfy demand, I believe that it is the likely outcome versus permenant undersupply.

Capacity at the lower end

The reallocation of capacity towards HBM that has starved the lower end of the market has forced OEMs, such as Dell and HP, to begin qualifying Chinese memory producers that are 3-4 years behind the leading edge to secure the necessary supply.

While equipment restrictions make bridging the technological gap to the leading edge a difficult prospect for these Chinese companies, they can add supply at the lower end of the market, which, over time, could ease the bottleneck in the spot price markets and increase competition.

With supply being eased at the lower end of the market, Micron, SK Hynix, and Samsung would have more capacity to service the HBM demand, potentially relieving the bottleneck sooner than expected.

Samsung

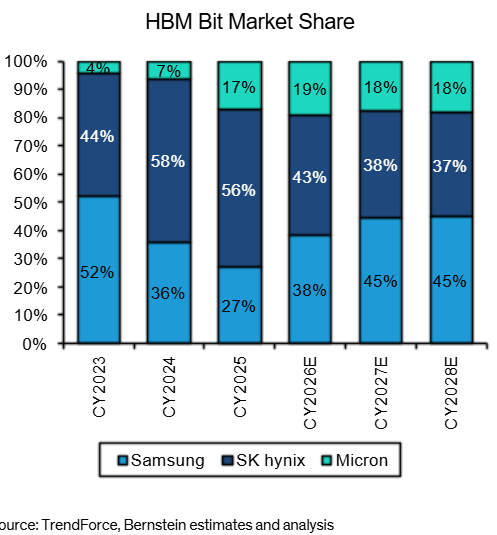

Samsung has long been the dominant company in the memory market. However, struggles to qualify its HBM3E chip with Nvidia left the company with the smallest market share of the 3 providers in this emerging segment of the market.

Not only have these struggles gifted HBM market share to SK Hynix and Micron, but it has also contributed to the supply shortage and provided leverage in pricing negotiations.

Samsung’s HBM4 & 4E chips are showing signs that the company is back on track. In early 2026, it passed Nvidia’s qualification tests, reportedly with the highest scores of the three.

This turnaround is likely bad news for everyone, particularly Micron; not only does it add supply to the market, but a credible third supplier who is likely eager to recapture lost market share fundamentally changes the negotiation dynamics in favour of buyers, such as Nvidia, pressuring prices.

Overall, I expect that capacity growth at both ends of the market and increased competition will likely have an equal and opposite reaction on prices (Newton’s third law), compressing margins, ROIC, and net income, unless it can be done with discipline, an unlikely prospect given the magnitude of the investments being made.

Cyclicality

Rule #1: Most things will prove to be cyclical; Rule #2: Some of the greatest opportunities for gain and loss come when other people forget rule number one. - Howard Marks

It is easy at the onset of a new wave of technology, which is seemingly only up and to the right, to forget that an industry is cyclical. Memory has historically been highly cyclical; in the good times, supply is tight, chips command premium prices, and capital is committed for expansion. By the time a new fab has reached volume production (3-5 years), the environment has changed, and prices collapse.

From these lofty levels, even the slightest hesitation of end demand, which could occur for any number of reasons, such as a slowdown in demand, macro environment, too much inventory, delay in a project, or even too high memory prices, could act like gravity on ASPs.

While many will argue that it is different this time, HBM is nowhere near as commoditised as other products. I would argue that it is a risk to bet on a market that has historically been extremely cyclical to have now transformed into a secular grower.

DRAM and NAND were both differentiated products during the early stages of those product lifecycles; over time, both became commoditised and cyclical due to competition. While the timeline is unpredictable, it is highly likely that HBM follows a similar path to DRAM, eventually evolving into a cyclical commodity that still generates solid returns across cycles due to the industry oligopoly structure. As a result, pricing the company without regard for this terminal result may be overvaluing the current growth and ASP trajectory.

The seeds of destruction are sown at the peak of prosperity

Historically, no one was trying to squeeze incremental performance out of memory chips; the incentives were simply not there to do so. However, due to the environment customers now face, this has changed. Likely, every major memory customer is now, to varying extents, working on ways to become more memory efficient.

The most prescient example is Google’s TurboQuant, a compression algorithm that can reduce the memory footprint of language models by up to 6x. So far, this is just a research project and has not been deployed into commercial use cases; however, the implications are clear.

Once efficiencies are found, they are rarely abandoned, which could not only ease the immediate bottleneck but also materially impact long-term volume demand as the collective effort to do more with less yields results. This self-correcting function is likely to produce a greater response the higher and more persistent these high prices last.

Valuation

“The most dangerous investment conditions generally stem from psychology that’s too positive. For this reason, fundamentals don’t have to deteriorate in order for losses to occur; a downgrading of investor opinion will suffice. High prices often collapse of their own weight.”- Howard Marks

At “just” 9x 2027 earnings, Micron may appear cheap; however, the real question is what happens in 2028 & beyond?

As I have laid out throughout this article, volume is likely to be higher, but increased supply from yield improvements, the big three and Chinese companies, cyclical dynamics, and memory utilisation gains all create headwinds to pricing beyond the immediate bottleneck.

Cyclical companies always look cheapest at the peak. I believe this to be no different here, with 2027 representing a cyclical peak earnings denominator rather than a new normal.

Micron’s gross margins historically run around 30%, adjusting EPS to reflect these dynamics, Micron becomes significantly more expensive.

Why not sell it all?

Looking through a probabilistic lens, I am assigning the highest probability that Micron is at peak cyclical earnings. However, this is not a certainty. At the other end of the range of outcomes, Micron could achieve above average profits for longer than I expect through; long term demand growth and disciplined supply growth that lead to persistent tight supply.

Furthermore, with companies looking to secure long-term supply agreements, up to 5 years in some cases, and increasing customisation, HBM could prove to be less commoditised than other products, driving growth at significantly better economics than previously seen.

At cost, Micron was a 4% position in my portfolio; at the time of sale, this had grown to 31%. I have now sold 80% of the position (25%+ of the portfolio). I have recuperated my initial investment, plus another 7 times.

This allows me to give this remaining 20% a longer leash, to see what happens, an insurance against my own ignorance. If my bearish thesis is correct, Micron will still be an extremely successful investment for me even if this final 10% underperforms.

Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment.

Very nice, well thought out article.