Evolution Update

Is the Long term thesis still intact?

Disclosure: I am long shares of Evolution AB ($EVVTY)

Note: this article should not be considered investment advice; please see the full disclaimer at the bottom.

Welcome to Leeder Capital!

I have previously covered Evolution AB, Airbnb, Crocs, Paycom, Xpel, Moncler, Charter Communications, Judges Scientific, and, most recently, Duolingo.

Evolution was my first deep dive on Substack back in early 2025.

In that 3-part series, I concluded that the company had a highly attractive business model with sustainable competitive advantages (predominantly scale economies, switching costs, and counterpositioning) that positioned it to benefit from the growth of the live casino industry.

My conviction that the business would be larger in 5-10 years, coupled with a low initial valuation, led me to conclude that Evolution presented an asymmetric opportunity. As a result, I made Evolution a 5% position (approximately) at cost in late 2024/ early 2025.

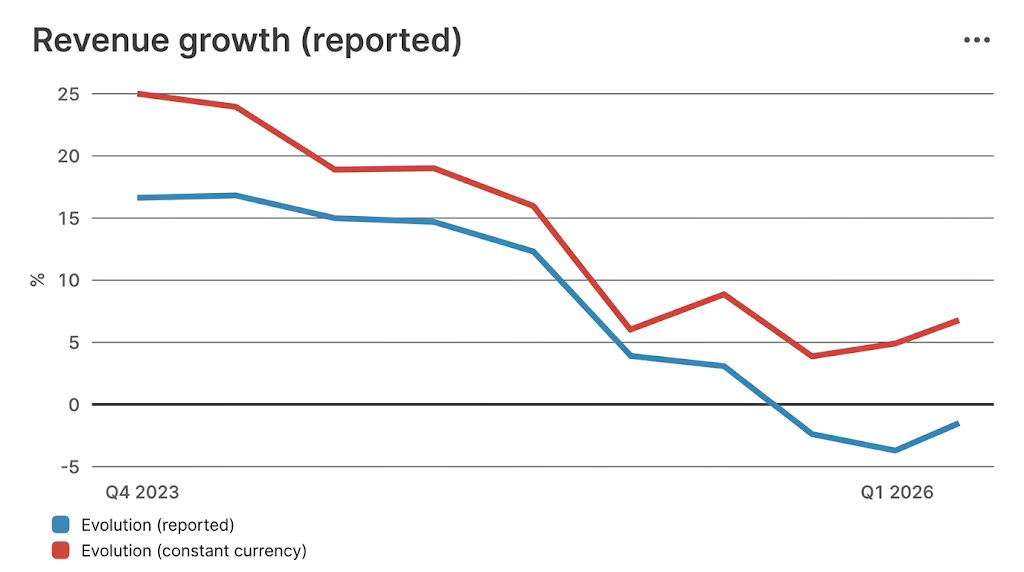

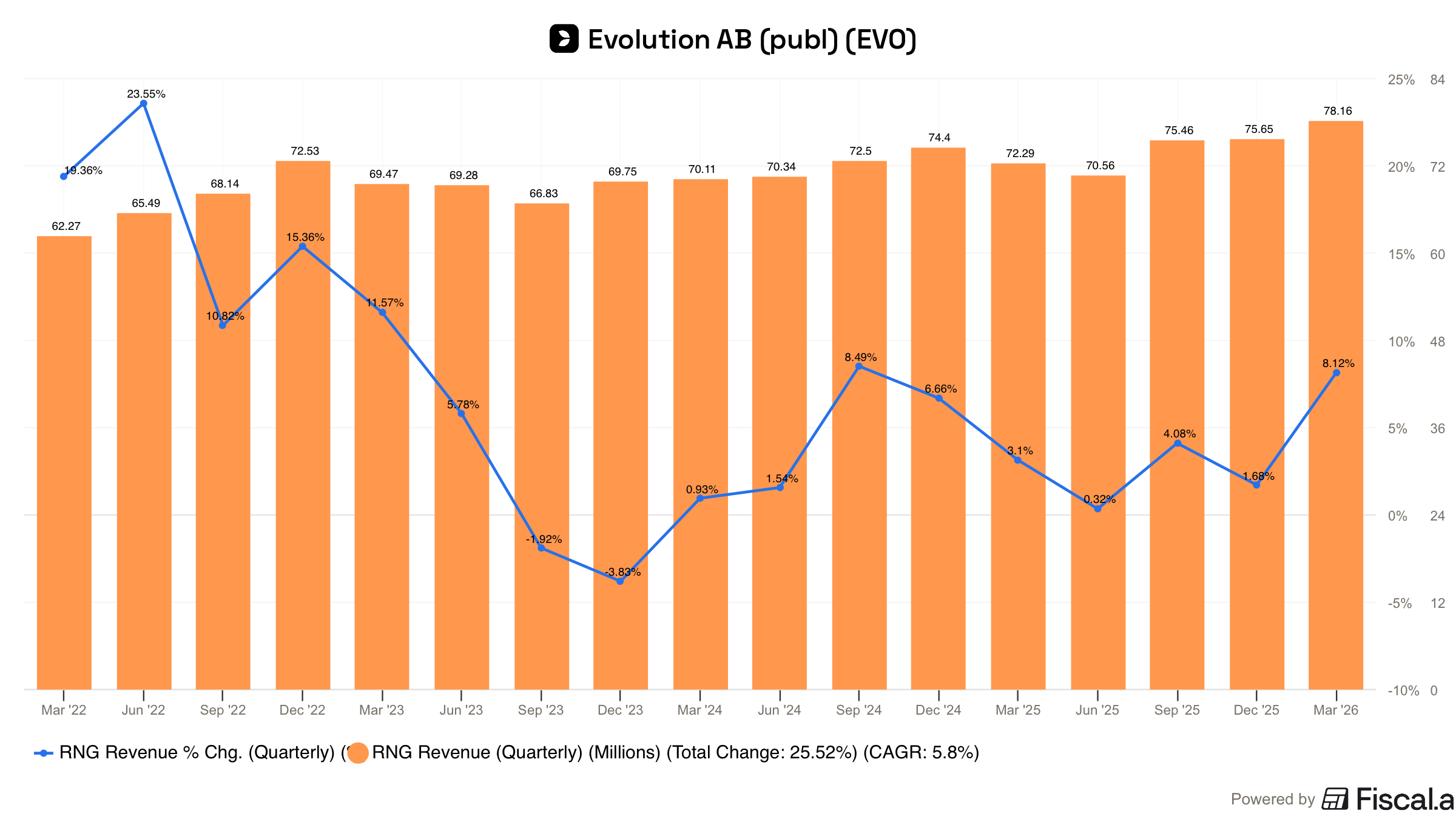

However, the fundamentals have not played out as expected.

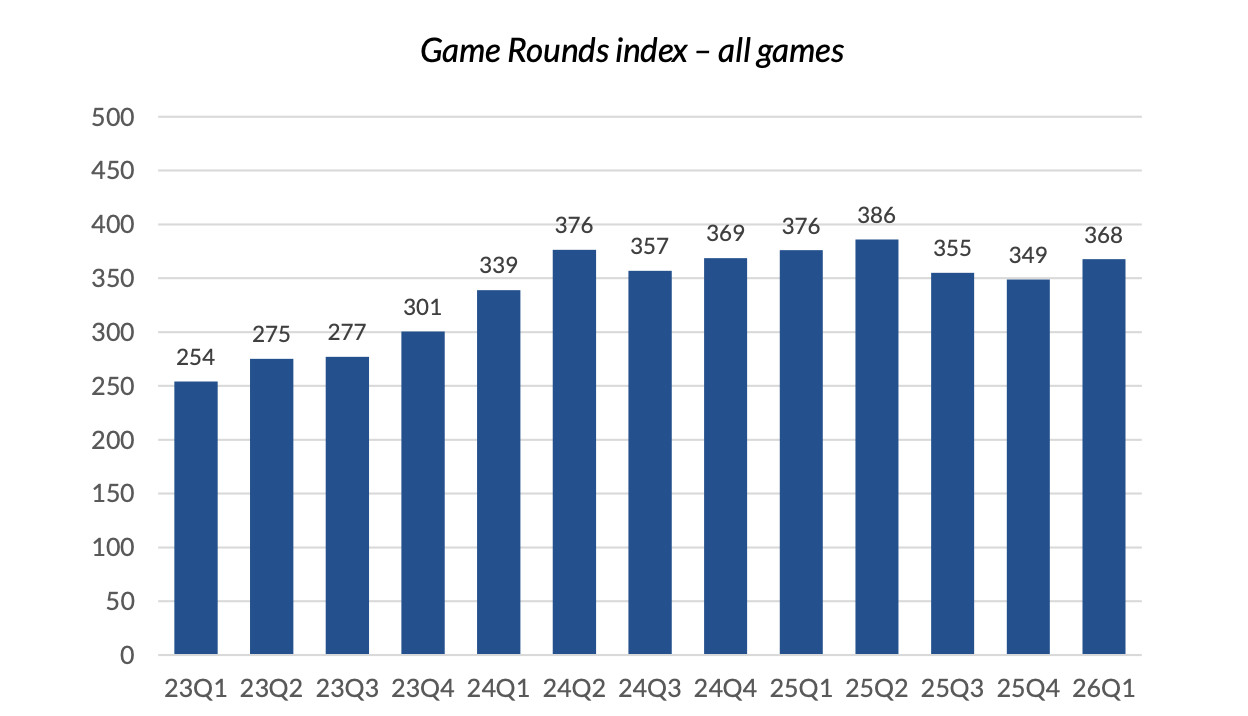

The games’ round index (an indicator of player activity) has stagnated, revenue has turned negative, and margins have contracted.

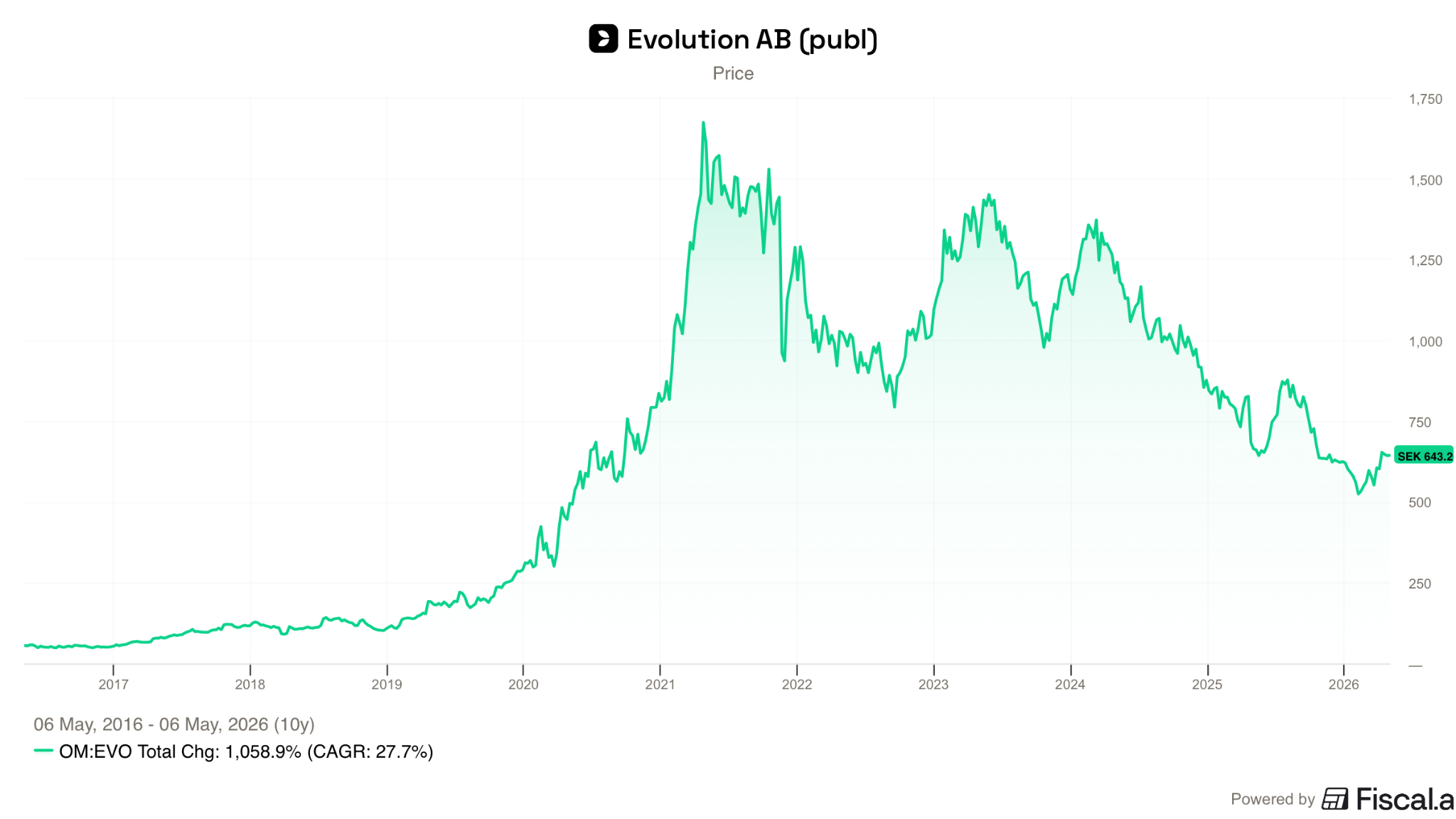

As a result of these weak results, shares have continued to struggle: over the past year, shares are down 23%, and in total, shares are 63% below their 2021 ATH. My position is down 13% (based on $69 $EVVTY)

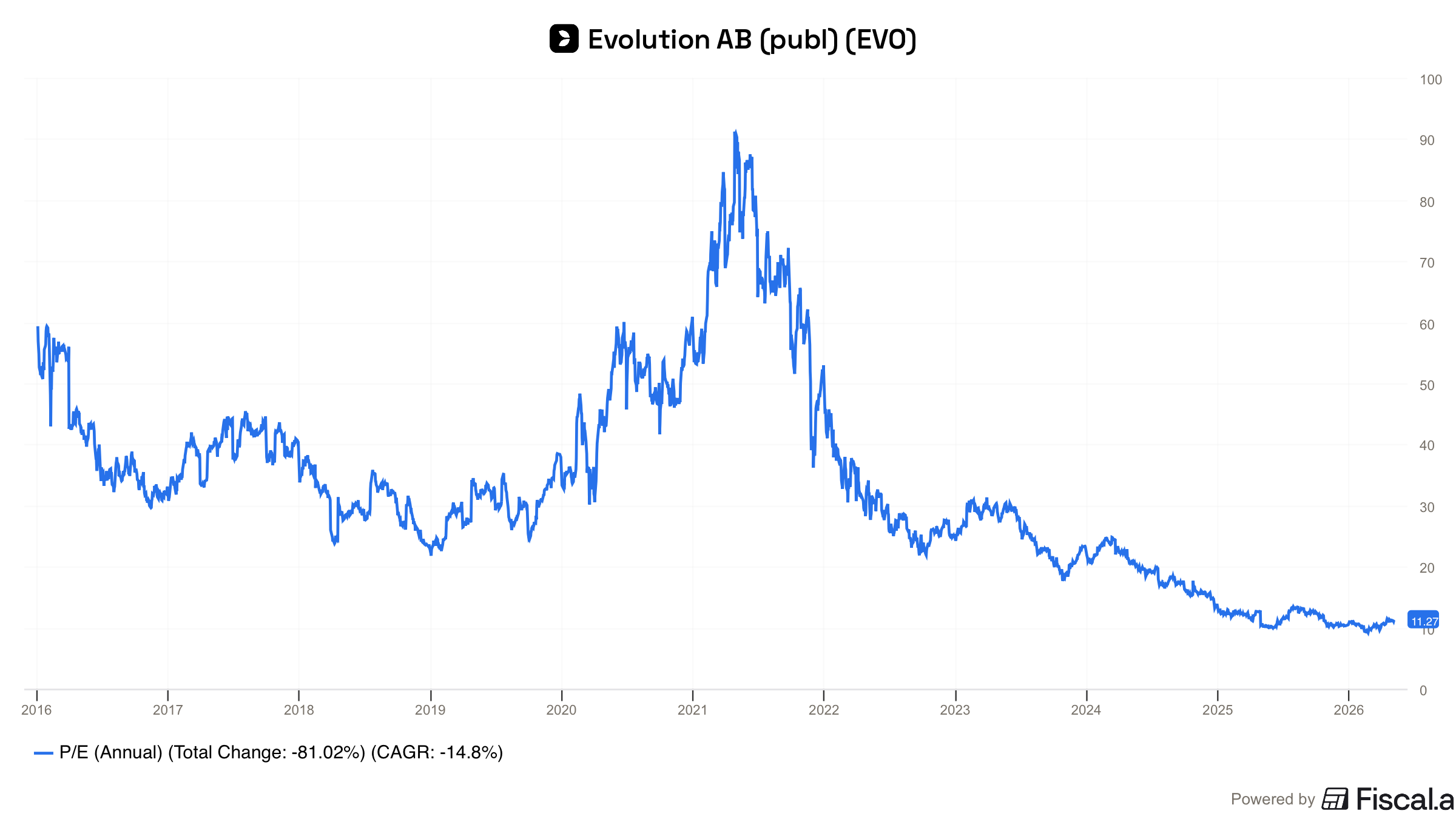

Today, the business trades at 11x earnings, implying a future growth rate of just 2%!

While the recent developments have been negative, I still believe my long-term thesis remains intact. Even when adjusting for my entry price to avoid sunk cost fallacy, I continue to believe it is an asymmetric investment opportunity.

In this article, I will discuss my thoughts on topics such as regulation, Cyber attacks, FX, the competitive landscape, and capital allocation.

Regulatory uncertainty

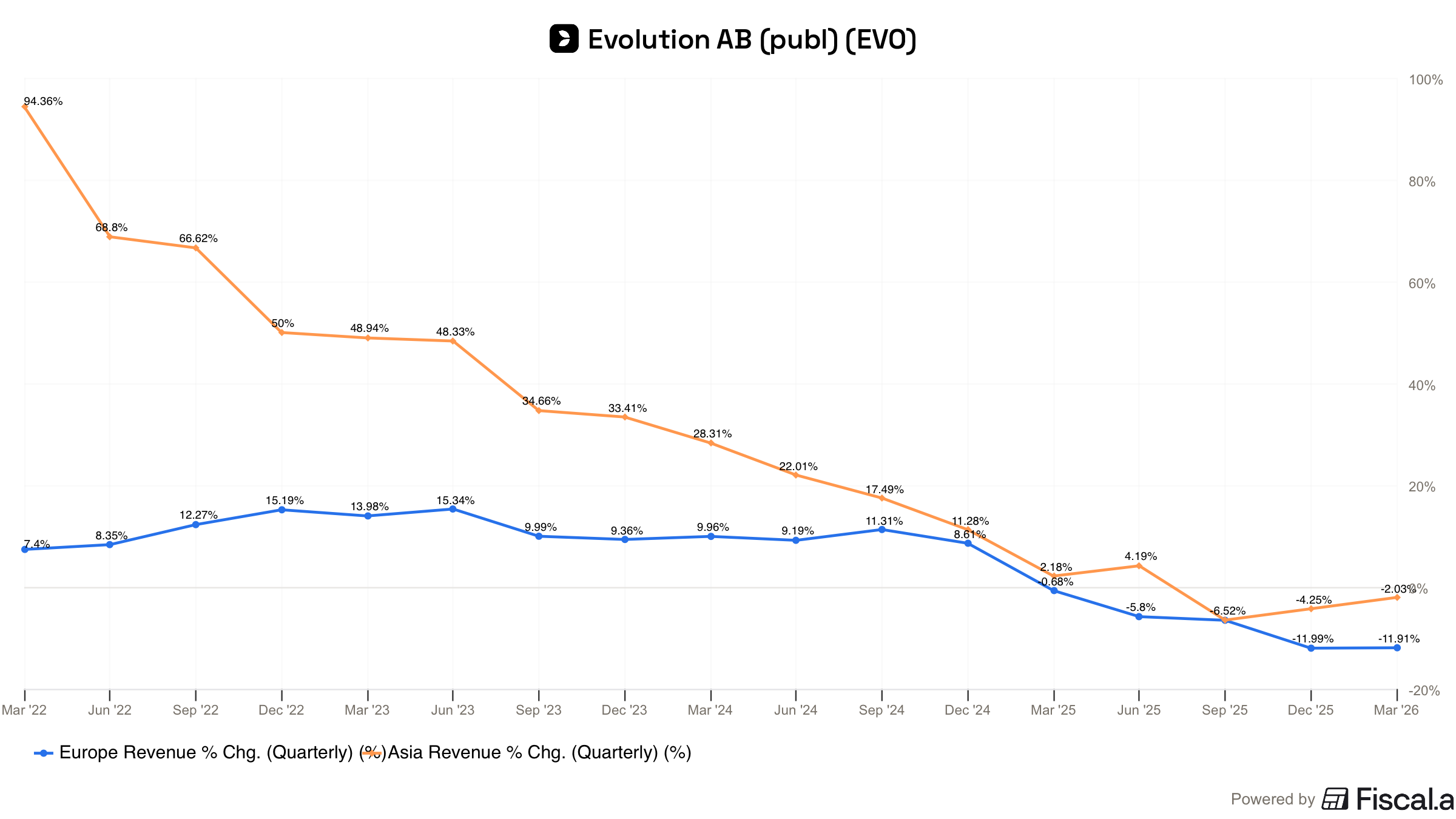

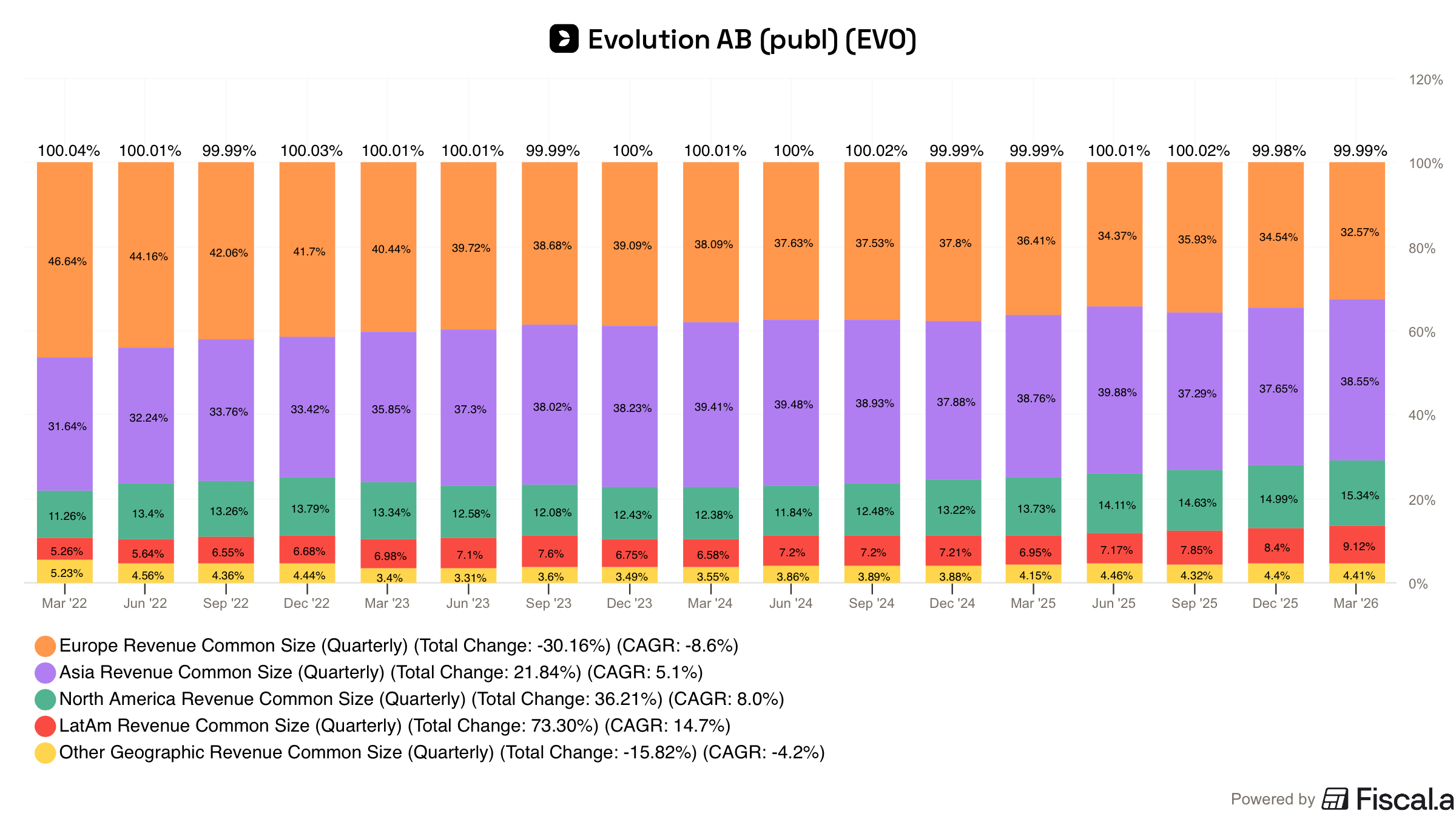

The primary contributor to the recent weak results is the regulatory uncertainty across Europe, Evolution’s largest market, and to some extent, Asia, which, along with the cyber attacks, has also struggled.

Beginning in Q1 2025, the company began to proactively ring-fence European markets, ensuring its games were only accessible through locally licensed operators. Management acknowledged that this would cause some short-term pain but that it was the right path going forward.

Compounding this, negative regulatory developments (tighter regulation + more restrictive interpretation of existing regulation) in markets such as the U.K., Sweden, Denmark, and the Netherlands have further accelerated the market’s decline.

These regulations intend to protect players, but to the consumer, deposit limits, spin speed constraints, product restrictions, loyalty/bonus restrictions, and higher taxes negatively impact the playing experience.

As a result, players switch to the all too easily accessible unregulated offshore operators that offer an unconstrained (superior) experience and higher odds (RTP) games. In some European markets, management has claimed that as much as 50% of gambling activity is now happening on these offshore sites, to the detriment of regulated operators served by Evolution. Prior to these events, Evolution was growing 9-10% in Europe, now, the segment is seeing double digit declines.

Similar to Europe, Asia has also been subject to shifting regulations, namely in India (banning all online money games) and the Philippines (implementing a regulatory structure that creates near-term weakness, although it should be beneficial over time).

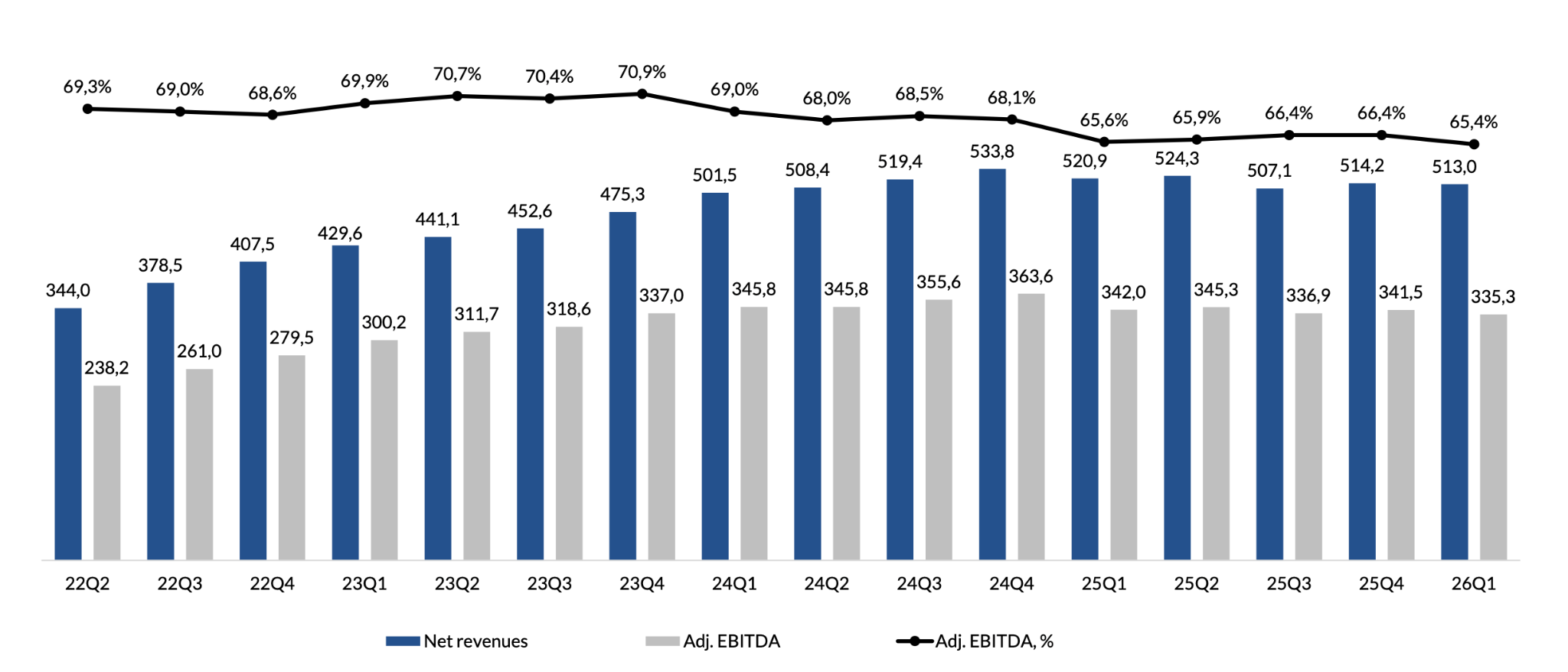

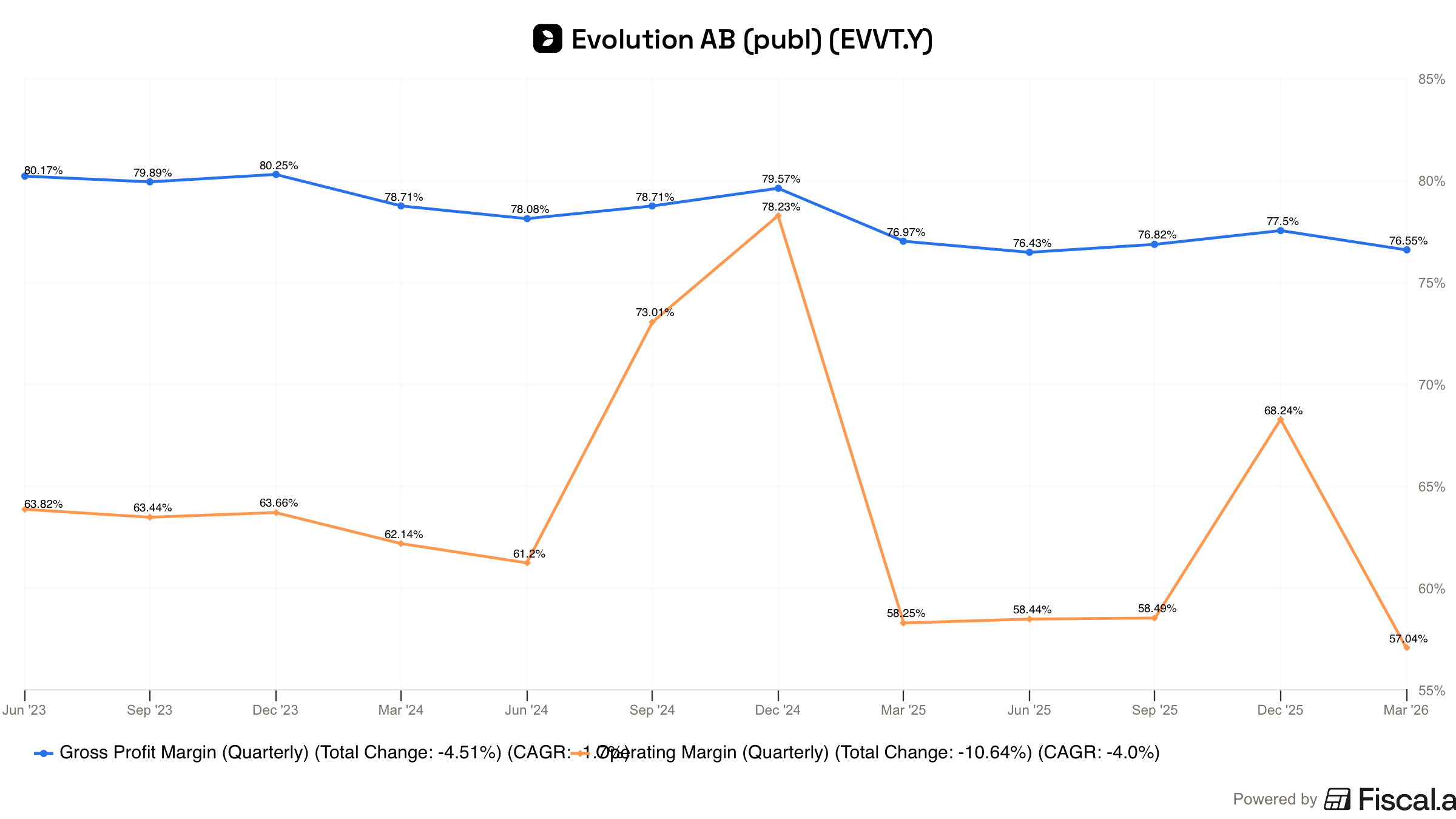

Evolution’s cost base is mostly fixed (significant operating leverage); as a result, this slowdown has also impacted the margin profile, which is experiencing the effect of deleverage.

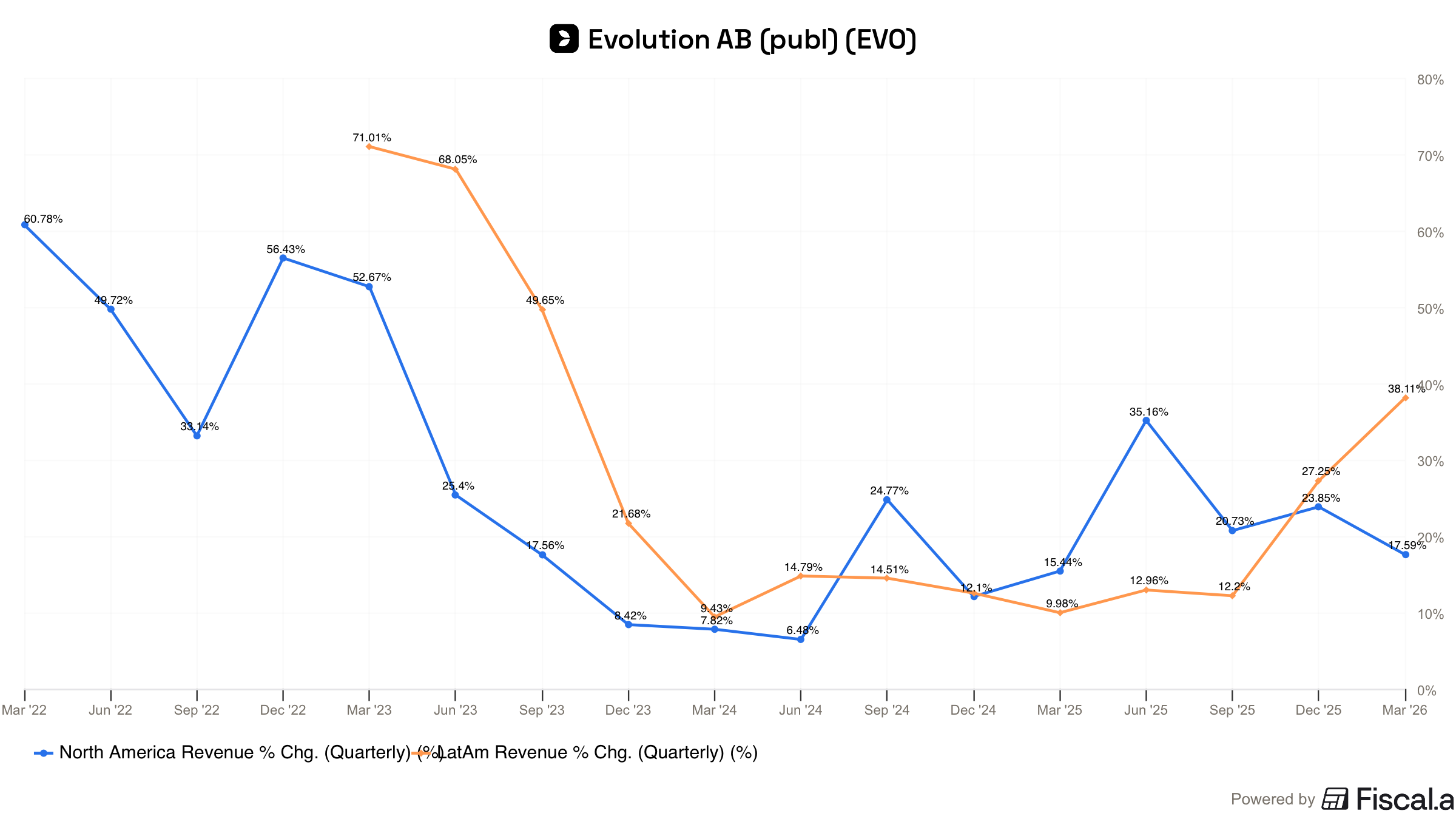

While existing jurisdictions have seen tighter regulation, the broader trend is for unregulated markets to introduce frameworks that govern and facilitate online casino. The US & South American segments have been benefiting from favourable regulations; Brazil, Alberta, and Maine have all introduced recent legislation that is (and should continue to) deliver real growth across these markets. However, due to their smaller contribution to the overall business, this growth has not been enough to offset Europe and Asia’s decline.

The downside of this growth, in many of these new regulated markets, is that Evolution is required to have a local studio, further impacting margins, ROIC, and capital intensity when compared to the historical operating model of a single studio for multiple markets. While this may sound negative, the economics of these new markets are still highly attractive and will likely become more so as each market scales.

For investors, regulation has always been framed as an opportunity, and overall, regulation has been a tailwind throughout the industry’s history, unlocking new users (legalisation) and providing the stability for operators to invest, facilitating long-term growth. But beneath the surface, at the market level, regulation has been constantly evolving as jurisdictions try to strike the right balance between creating local jobs, collecting tax revenue, and ensuring player safety.

The new regulations (particularly in Europe) are not having the desired effect; they fail to protect players who shift to unregulated (illegal) websites that offer superior playing experiences. jurisdictions lose out on tax revenue, and local jobs are put at risk as licensed operators are placed in limbo. This is bad for everyone involved.

This is not the first time that this has happened; the cobra effect can be seen at different stages across different gambling sectors: regulators implement restrictive policies, forcing players to the black market, impacting tax revenue, leading to a regulatory review that eventually reverses the decision. Sweden is a good example, regulators imposed strict regulations back in 2019, after years of players shifting to offshore sites (channelisation fell from 90%+ to as low as 59%), regulators have introduced reformed legislation (for January 2027) that intends to fix the channelisation problem.

Although the regulatory environment could continue to get worse, limiting the immediate upside, I think it is foolish to bet against the long-term trend. The incentives at play, long-term trend, and history of similar events lead me to assign a greater probability of this being a temporary headwind versus a structural change. However, a timeline for any kind of recovery is simply unknowable and may be far longer than most investors’ time horizons.

In the near term, the only way Evolution can bring players back is by introducing better, more engaging games. More on this in a moment.

Cyber attacks

Asia, Evolution’s second-largest market, as mentioned, has also faced significant headwinds. First disclosed in Q3 2024, the company has been targeted by sophisticated cybercrime operations that intercept, manipulate, and redistribute Evolution’s live games. To players, these are indistinguishable; players therefore bet on these unauthorised games, but Evolution receives no revenue.

Management initially thought this would take a couple of quarters to resolve; however, it has proven more difficult than expected. Countermeasures have shifted between periods of being too restrictive, impacting legitimate players, and not restrictive enough. Despite it taking longer than expected, progress is reportedly being made.

“We believe that it’s harder to steal our content today than it was a year ago.” - Martin Carlesund

I expect the company to continue making steady progress over time, similar to regulatory headwinds; this is unlikely to be in a straight line, but over time, it will likely make the company stronger.

Asia is showing some positive signs: The company has now reported two consecutive quarters of (QoQ) growth, potentially signalling that they are beginning to find the right balance.

FX headwind

Evolution reports revenue in EUR. This has created a significant headwind to reported revenue as the Euro has strengthened. This headwind is currently at its widest point; on a constant currency basis, revenue actually grew 6.8% in Q1 2026, highlighting that demand is actually stronger than reported and has continued to grow throughout this tough period.

Historically, reporting in EUR made sense because Europe was the major source of revenue; however, as other regions have grown, reliance on this segment has declined significantly. Over time, these fluctuations in currency will even themselves out, and adjusting for these currency fluctuations makes sense to understand the underlying demand trends.

On an underlying basis, revenue has now accelerated for 3 consecutive quarters (YoY), in a stark contrast to the reported figures.

It’s not all bad

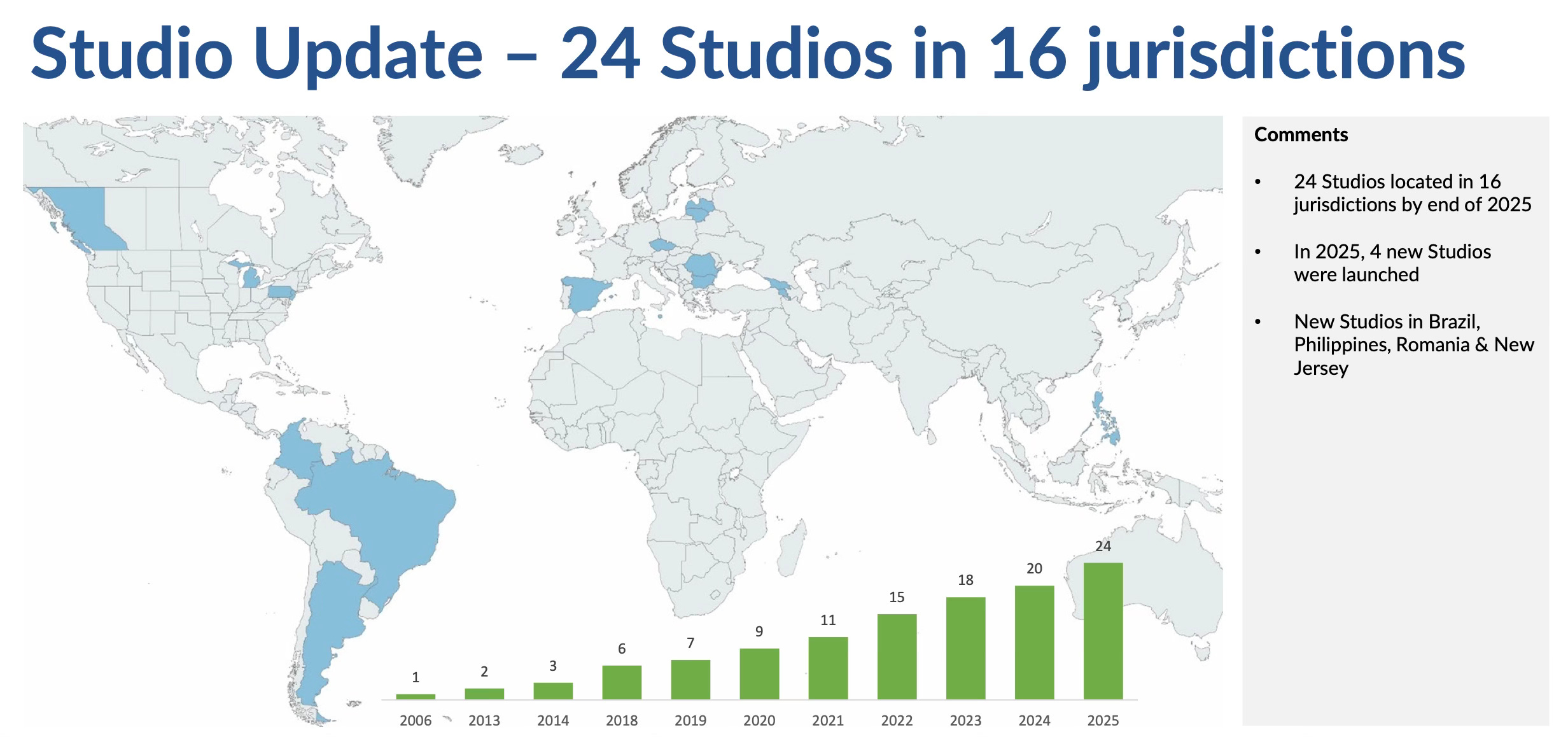

Despite industry growth slowing, Evolution continues to dominate the live segment with an estimated 60% market share. The company now operates 2,000 live tables, up from 1,700 a year ago, and over 4X more than that of the closest competitor, Playtech (450).

Furthermore, the company continues to attract operators to its platform; in 2025, the customer count grew from 800 to 870.

Two factors give me confidence that Evolution can sustain/expand this lead.

Increasing complexity: Operating a live business at scale across multiple markets is extremely complicated. Management has repeatedly stated that the barriers to entry are low, but the barriers to success are high. In an increasingly complex regulatory environment, operating at scale is only made more difficult.

As more markets demand a local presence, Evolution is best positioned with the resources and know-how to build and ramp studios, allowing the company to consistently be first to new markets. Being first allows Evolution to capture the majority of the market from day one, entrenching itself among operators before competitors can.

For smaller competitors, who lack the resources and relationships (operator and regulatory), entering new markets is an inherently riskier proposition, where the barriers to success keep rising, and the relative reward from any single studio is dropping. Evolution’s recent €27.6m acquisition of an undisclosed competitor’s studio in Argentina, and Light & Wonders withdrawal from the market altogether, is evidence of this challenging environment at play. Not only does this make it increasingly difficult for established players to gain scale, but it also makes it harder to enter the industry.

Innovation: Evolution continues to extend its gaming advantage with 2 new enhancements: speed game shows and an exclusive partnership with Hasbro.

Speed game shows take the existing game show idea but adapt it for an audience accustomed to TikTok and Instagram Reels. The first launch in this new category, Ice Fishing, has exceeded all expectations, at times reaching similar player numbers to Crazy Time and garnering significant social media attention.

Looking at Evolution’s closest competitors, neither Pragmatic Play nor Playtech has released anything resembling a speed game show as of yet; in fact, management claims that competitors, more and more, are just copying Evolution rather than innovating for themselves.

In 2025, Evolution also signed an exclusive licensing agreement with Hasbro, an agreement that had belonged to a competitor for the last 20 years (believed to be Playtech). In 2026, Evolution plans to release: Game Night, Monopoly Filthy Rich, Monopoly Deluxe, Monopoly Roulette, and several RNG games. The goal for Game Night and Monopoly Filthy Rich is clear: to surpass the high-water mark of 2024’s lightning storm.

If Evolution can successfully develop and launch future speed game shows and Monopoly releases through the second half of 2026, they will further differentiate themselves, increasing the switching costs for operators. The Hasbro partnership also adds an element of cornered resources to the company’s already strong value proposition that should be particularly beneficial in markets like the US, where there is high brand recognition.

While Evolution’s competitive position in isolation appears strong and growing stronger, the reality is that the company is competing against a broader array of competitors across betting formats. The emergence of prediction markets has likely taken dollars away from the live casino space. While both can coexist, Evolution must continue to push the boundaries for live casinos to continue gaining share.

RNG Turnaround

Since entering the RNG category in 2020 with the acquisition of NetEnt for €1.91 billion (in shares!), it is fair to say the performance has been a disappointment, the segment has grown a total of 26% between FY 2021 & 25 (including acquisitions). Management has not shied away from this, but they have also not been able to re-ignite growth, while continuing to acquire more brands.

To succeed in RNG, 4 key ingredients are required: strong game development capabilities, brand identity, distribution platform, and streaming relationships. It appears that Evolution has fallen short on the first and fourth hurdle (poor games and inconsistent streamer engagement).

In a recent interview with the new leader of Evolution RNG, Jonas Tegman, he made several comments that give us an insight into some of the issues that have plagued the RNG businesses:

“old ways and old processes”

“Titles and hierarchy, they meant a lot of meetings instead of actually building the product.”

“Live and slots are two different products. The competition is also different.”

These comments suggest that Evolution’s direct integration with the live business has been a mistake, stifling innovation and allowing a culture of bureaucracy to emerge.

Jonas Tegman seems to be the right person for this new role. He is the co-founder of No Limit City (NLC). NLC has been referenced repeatedly by Evolution’s management as the standout performer of the RNG segment; if anyone can turn it around, it’s him.

Since assuming the role in March 2025, Tegman has taken significant actions: shifted focus from process orientation to product orientation (eliminating the old way of doing things), gained independence from the live segment (uncoupling the two businesses), flattened the organisation structure, and re-engaged the streamer community.

It is clear that the RNG segment cannot work when integrated so closely with the live business; these actions provide the high odds of a successful turnaround, accelerating growth.

Tegman expects players may be able to see these changes translate into better games beginning in the second half of 2026; however, it will take time for operators and players to gain confidence in the turnaround.

“We’re playing the long game here.” - Jonas Tegman.

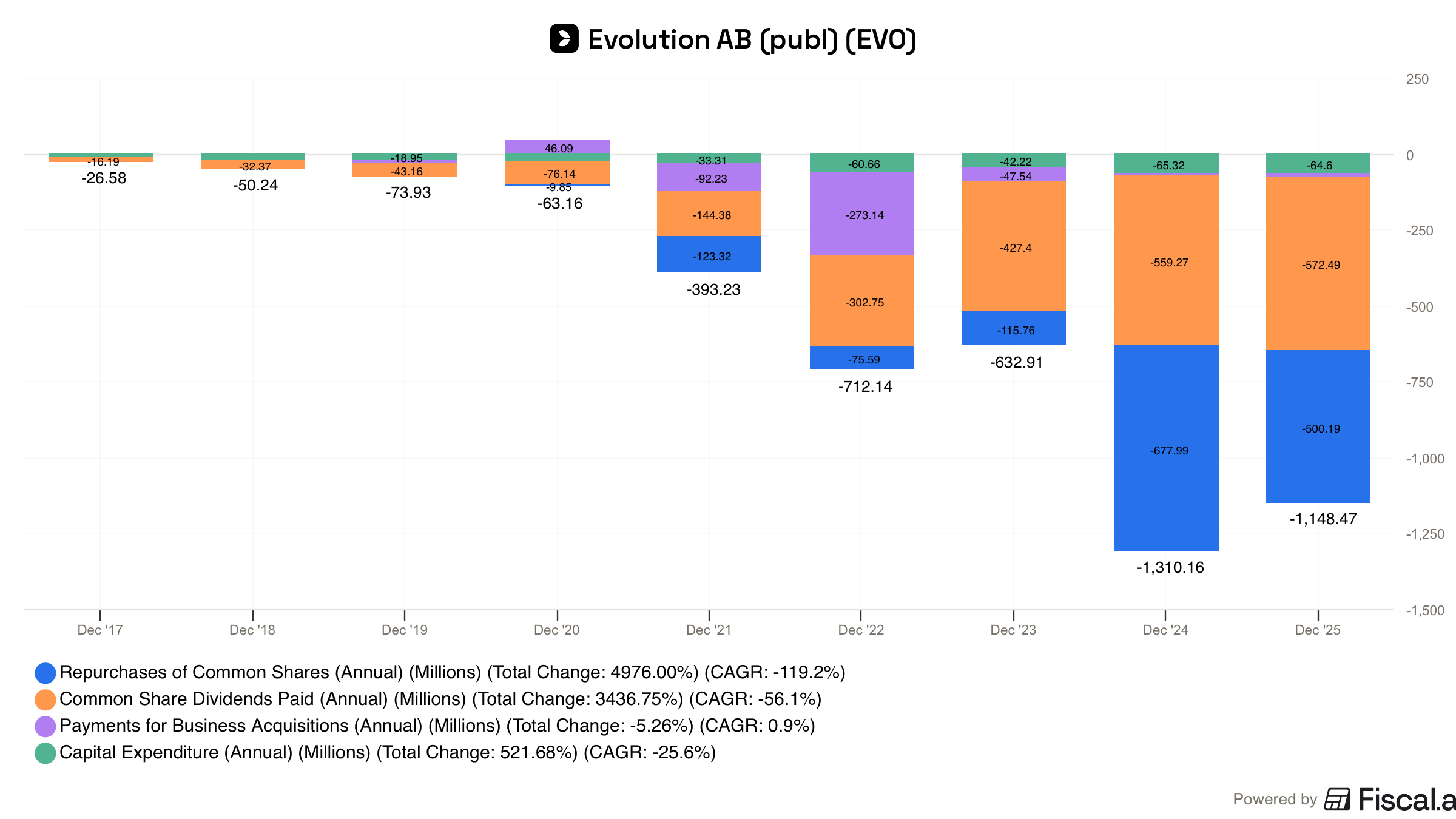

Improving Capital Allocation

Evolution’s Capital allocation has historically left something to be desired. On the one hand, the company has created significant value in its core live business; consistently delivering a best-in-class game portfolio, and scaling a global network of studios, more often than not being the first to any new market. However, the acquisition of lower-quality RNG businesses, compounded by the occasional use of shares, has likely destroyed shareholder value, at least so far.

The rigid dividend policy has also been suboptimal: granted, it is better to return the capital to shareholders versus making further RNG acquisitions; however, the mandate to return 50% of profits via this dividend does not take into account the share price, eliminating any kind of flexibility.

In recent years, capital allocation priorities have evolved, for the better.

Organic investment remains top of the list; the company continues to invest in launching new games and building out studios, signalling confidence in their future growth prospects. The company has also invested in several new areas: partnering with Gaming Arts to bring online games into land-based casinos, while also launching a new in-house RNG brand, Sneaky Slots.

Before the RNG acquisitions, Evolution had returns on invested capital of 70-80%. Returns have likely come down since then; however, they are likely to still be highly attractive (excluding RNG goodwill), and where it makes sense, all available cash should continue to be re-invested here.

Opportunistic acquisitions remain the next priority. However, the disappointing track record of the RNG acquisitions appears to have raised the bar for future deals; instead, as mentioned, management has favoured building a new RNG brand from scratch, likely a lower risk bet.

The company has still made a few acquisitions: Galaxy Gaming (still pending) and the previously mentioned Argentina studio purchase. The size (smaller) and rationale behind both of these are fundamentally different (US licenses and studio space) from previous acquisitions, which should lead to a better outcome, or at least less shareholder capital destroyed. I hope this discipline continues.

The final priority is returning cash to shareholders. Here, share buybacks have been increasingly favoured over the historical dividend, and in 2025, the dividend was suspended altogether. Instead, the board is authorised to buy up to 10% of shares outstanding.

Comparing share buyback to further acquisitions, it makes a great deal of sense to buy back a small portion of the wonderful business that Evolution already has, versus acquiring the entirety of an inferior business that has historically not worked out very well. Evolution’s management should take inspiration from FICO.

“Any business that we look at that we don’t love as much as our own, that includes pretty much the whole universe, would be dilutive in the long run. And so we’re not very acquisitive.” — William Lansing, CEO

At these valuations, I think share buybacks are the best use of cash outside of reinvesting in the business.

Acquiring fewer businesses and buying back more shares shifts the capital allocation framework from value-neutral/destructive to value accretive, which, over time, should be highly accretive to shareholders, which will be seen in the per share metrics.

Conclusion

The continued decline in Evolution’s share price not only reflects the current challenges but also a deterioration in confidence around its long term growth prospects, pricing in just 2% future growth.

I disagree with this sentiment, as I have laid out in this update, the resumption of long-term regulatory tailwinds, improvement in the RNG segment, and improved capital allocation could all contribute to per-share value increasing at a rate that exceeds market expectations.

While there certainly are risks, I believe the current share price provides an adequate margin of safety, even when I adjust it for my average cost. As a result, I have continued to add to my position in recent weeks.

Disclosure: I/we may or may not have a beneficial long position in any of the securities discussed in this post, either through stock ownership, options, or other derivatives. This article expresses our own opinions. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment.

Sources: Company Filings, Next.IO, Next.IO, Next.IO, Netherlands regulations, US regulatory history, iGB, Next.IO, UK tax increases, The cobra effect, Quatr

A strong business model can survive competition longer than markets expect if network effects, scale advantages, and customer behavior remain intact.

The key transmission signal is whether margins and retention start deteriorating structurally rather than sentiment alone.

What angle do you think Kevin Dart is playing at. He's building up quite a sizeable stake in evolution and other gambling companies.